|

|  |

|

|

Apartment Rents Hold While Bracing for New Supply

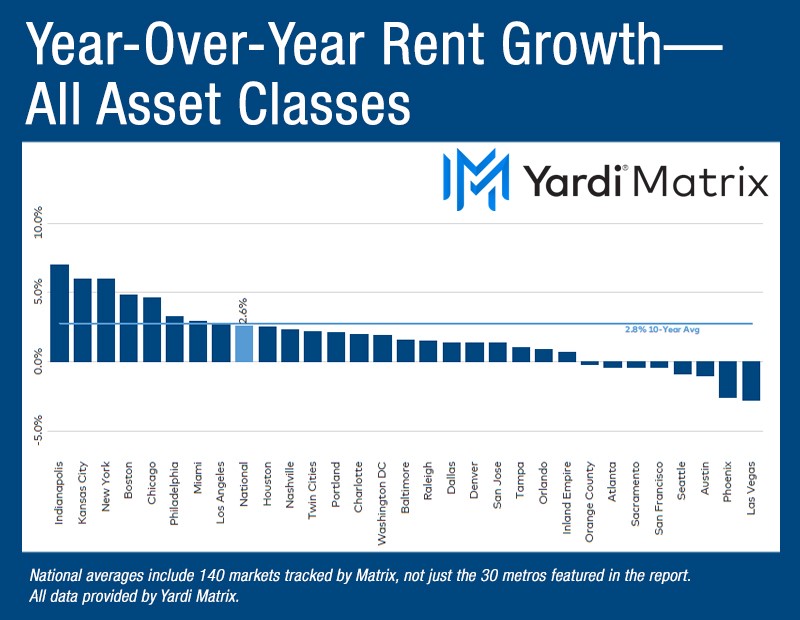

Yardi Matrix reported that between January and May of this year, apartment rents rose $18, or 1.0% to a national average of $1,716. Year-over-year rent growth was at 2.3% in May. May was the fifth straight month of rent increases following drops toward the end of 2022, according to RealPage.

The rent growth has been led this year by metros in the Midwest and Northeast. Indianapolis was in the top spot (7.0%), followed by Kansas City (6.0%), New York (6.0%), Boston (4.8%), and Chicago (4.6%). The markets which have experienced the most rent growth over the last decade are now showing declines.

Metros with negative year-over year-growth include Las Vegas (-2.8%), Phoenix (-2.6%), Austin (-1.0%) and Seattle (-0.9%). San Francisco, Atlanta, Sacramento, and Orange County also showed declines this year as new supply is putting downward pressure on rent growth. Other factors contributing to the slowing are declining household formations, scarcity of affordable units and waning demand as layoffs continue and consumer confidence erodes. Renewal rent growth remains robust but has decelerated for the past 10 months as these increases are getting closer to asking rents. Renewal rates rose 6.5% in May.

| |

|

Edward M. Aloe

President and CEO

626-229-9057

| |

|

|

In the latest Episode, “Understanding the Power of Pref Equity”, Ed sits down with John Pappalardo, Director of Business Development for CALCAP Strategic Opportunities. Learn how different components of the capital stack can be used to increase leverage and enhance investor returns.

The Real Estate Wealth Podcast with Ed Aloe

We look forward to growing this initiative with your support!

If you’re interested in joining us for an episode, or have feedback, please let us know by replying to this message. We’re eager to hear from you and deliver quality content to satisfy all levels of investors!

| |

|

U.S. inflation hits two-year low as rent prices decline

The CPI rose 3.0% year over year in June, which was lower than May's 4.0% reading

Indexes that increased in June include shelter, motor vehicle insurance, apparel, recreation, and personal care. The indexes for airline fares, communication, used cars and trucks, and household furnishings and operations were among those that decreased in June.

Shelter, which is the largest category, also posted a sizable increase, rising 7.8% year over year (down from 8.0% in May) and accounting for more than 70% of the total increase in the all items less food and energy index which was up 0.2% in June.

But the shelter inflation figure is highly imperfect. The BLS’s CPI metric lags asking rents because the CPI measures in-place rent, and because most renters see a change only once per year, the index lags significantly from asking rents on new leases. Peak rent inflation was between May 2022 and February 2023, but has declined in subsequent months and is expected to continue to do so.

An index tracking the rent of primary residences slowed to a 0.46% change in June, the weakest increase since March 2022.

“Despite the positive inflation report, the Fed likely will resume its rate hikes when it meets later this month, remaining committed to raising interest rates until the magical 2% inflation target is met,” said Lisa Sturtevant, chief economist at Bright MLS.

View Article Here

| | | |

|

Commercial real estate is high among banker's ongoing debt concerns

Signs point to increasing credit risk in commercial real estate loan portfolios, as recent skittishness around lending has compounded existing concerns. The CRE sector was already under pressure due to pandemic-induced trends such as the shift to remote and hybrid work that resulted in more unused commercial space, and Federal Reserve rate increases totaling 4.75% over the past year. Rate increases have made refinancing commercial property loans onerous, requiring a significant increase in debt or a capital contribution to support new loan-to-value ratios.

These trends mark a reversal from the positive environment for commercial real estate seen for most of the past decade. That environment was characterized by low interest rates and favorable market trends that fostered growth in CRE lending, especially at regional and community banks.

View Article Here

| | | |

|

Refinancing Could Be Disaster for Many Loans, Not Just Office

Debt service coverage ratios are looking tricky, according to Trepp.

The screws are tightening on CRE loans. For example, multifamily debt originations dropped sharply while CMBS delinquency rates seem to be nearing the beginning of the great slide. And as CRE property values slide, the ability to easily negotiate a refi on a building gets tougher.

Over the past decade, CRE loan origination volumes had trended upwards, according to Trepp. As that is no longer the case, the question becomes “what proportion of the maturing loan market, both in aggregate and in specific markets, could face refinancing challenges in environments where the prevailing interest rate is higher than the loan coupon.”

To get closer to an answer, Trepp performed an analysis on maturing loans that by 2024 could land with a debt service coverage ratio (DSCR) based on net cash flow (NCF) of less than 1.25 times (a common risk management threshold), assuming loan coupon escalations.

View Article Here

| | | |

|

Angelo R. Mozilo

1938-2023

| |

|

About CALCAP

California Capital Real Estate Advisors, Inc., and its affiliate entities (CALCAP Asset Management, CALCAP Properties, CALCAP Lending, CALCAP Senior Healthcare, and CALCAP Strategic Opportunities, collectively known as “CALCAP”), is a California-based investment company founded in 2008 and headquartered in Pasadena, California. The Company sponsors alternative real estate investment opportunities focused on demographically driven housing. CALCAP has been able to consistently provide both individual and institutional investors with outstanding returns over the last 14 years. The Company uses a highly selective and disciplined investment approach, focused on delivering superior risk-adjusted returns. CALCAP currently has over $650mm in Assets Under Management. To learn more visit www.calcap.com.

Social Mission

CALCAP CARES is a 501(c)(3) private foundation organized to encourage employees to find a way to give back to the neighborhoods where we invest. CALCAP has created "GiveTime4Autism" as its initial program which gives employees the opportunity to donate unused vacation and sick days for a very worthy cause.

| |

|

LOS ANGELES

The Sanborn House

65 N. Catalina Avenue

Pasadena, CA 91106

SAN DIEGO

12626 High Bluff Drive, Suite 360

San Diego, CA 92130

PHOENIX

740 N. 52nd Street

Phoenix, AZ 85008

SANTA BARBARA

1309 State Street, Suite A

Santa Barbara, CA 93101

| |

|

Edward M. Aloe, Founder & CEO

(626) 229-9057

ed.aloe@calcap.com

Patrick A. Wakeman, Principal

(858) 764-4890

pat.wakeman@calcap.com

Drew Buccino, Principal and COO

(602) 419-3381

drew.buccino@calcap.com

Greg Blix,Dir. of Investor Relations

(805) 896-8500

greg.blix@calcap.com

Tim Landwehr

Executive VP, CALCAP Lending, LLC

747-268-0675

tim.landwehr@calcap.com

| |

Mark A. Mozilo, Principal

(626) 229-9056

| | | | |