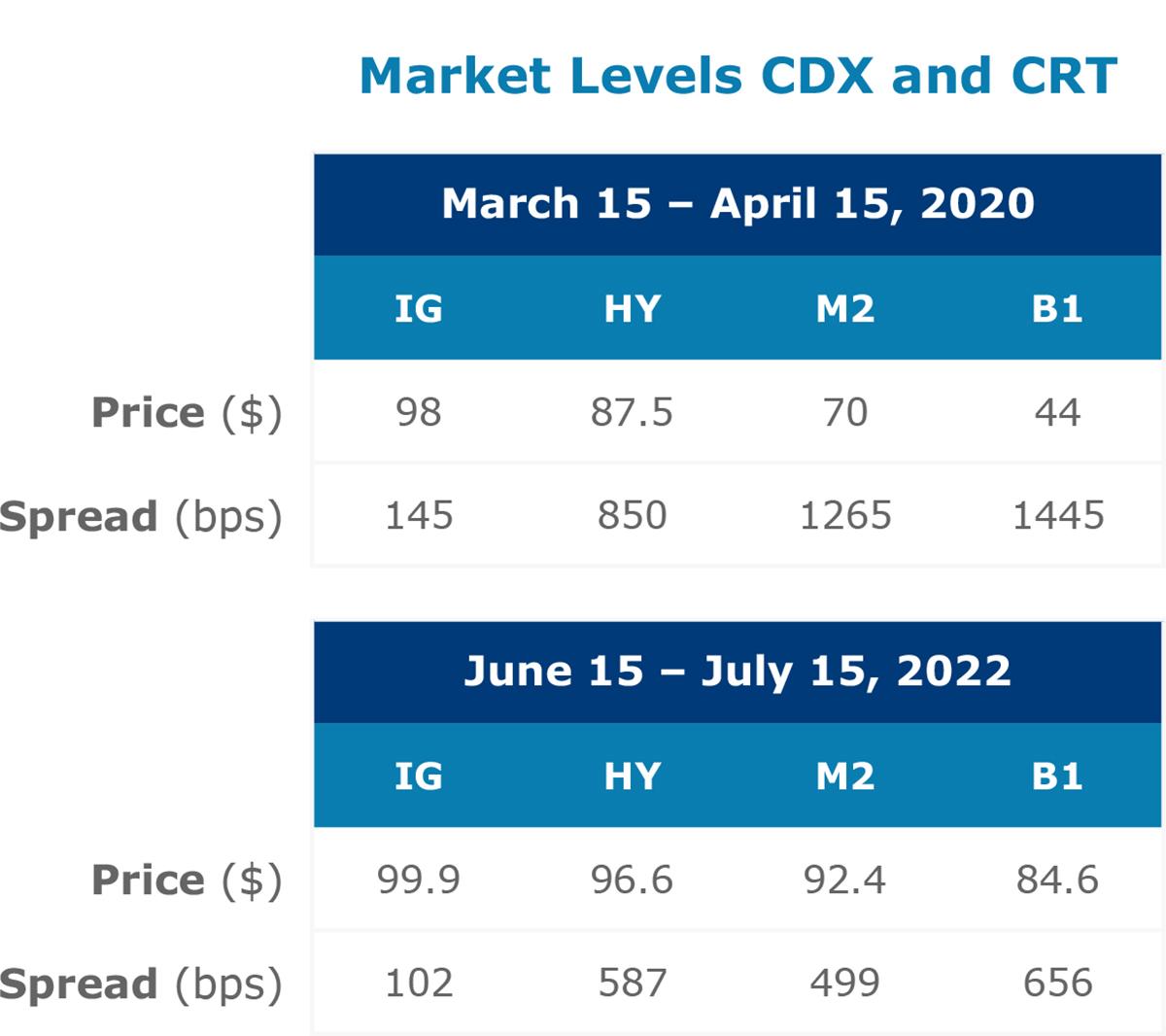

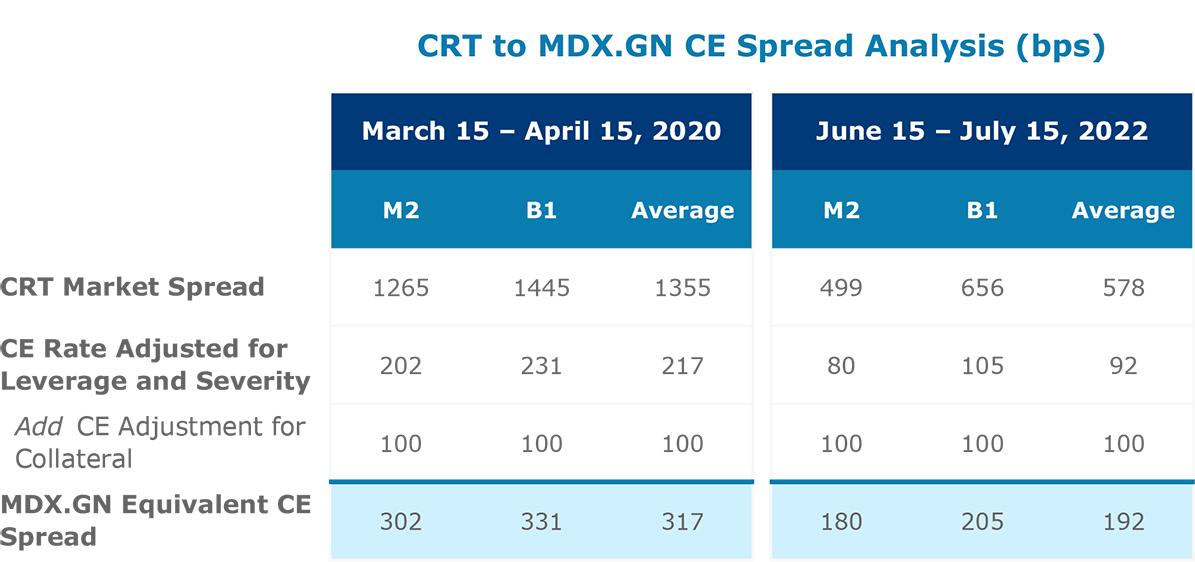

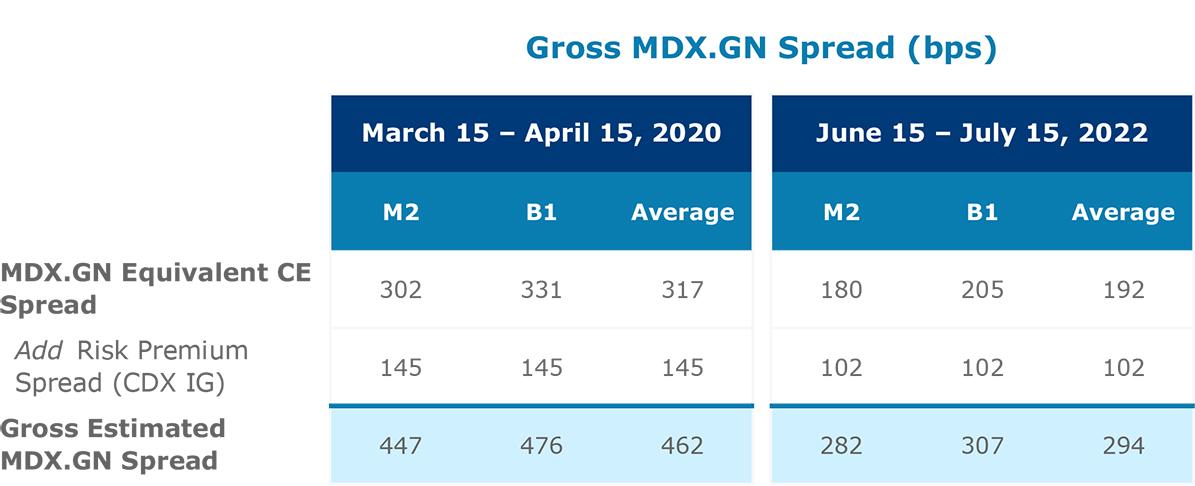

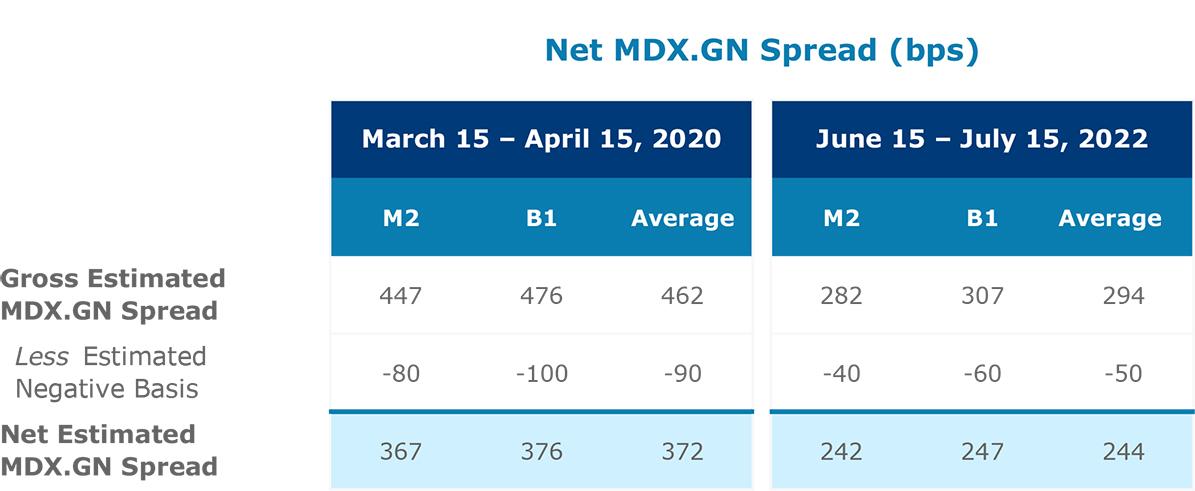

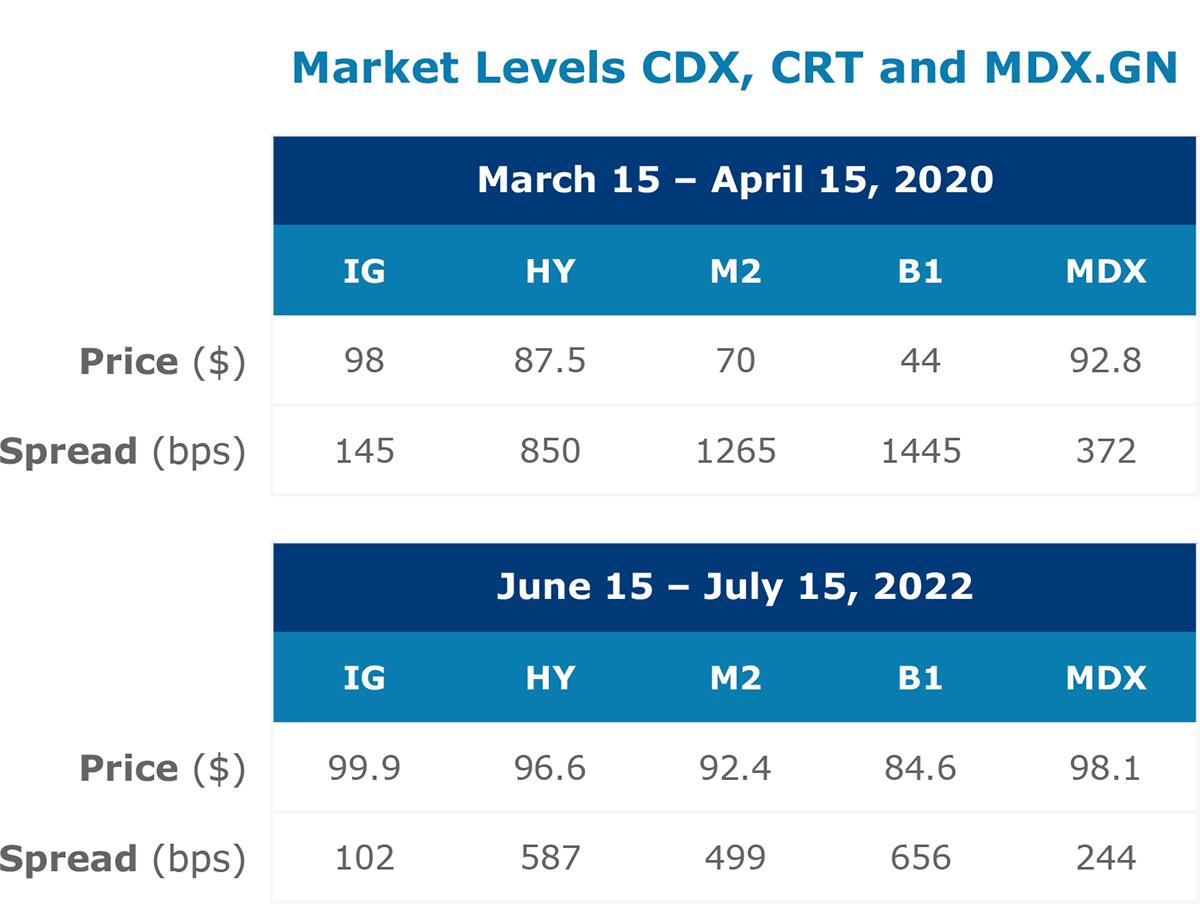

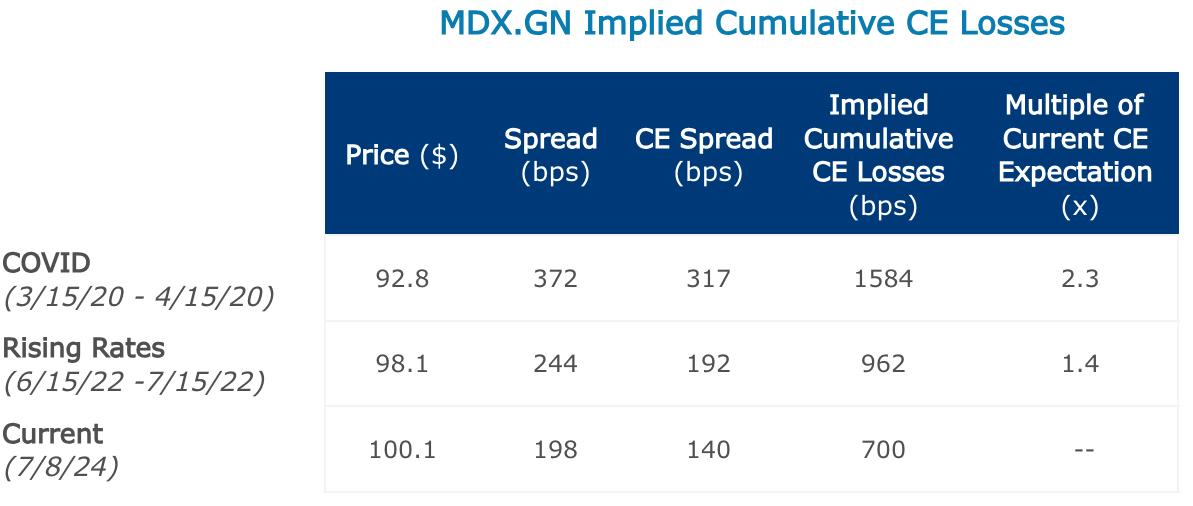

Market Conditions During Early COVID provide a recent test of pricing MDX swaps during an extreme macro stress period. Both CDX and CRT reached their high spreads/low dollar prices between March 15 and April 15, 2020. Meanwhile, the 30 days between June 15 and July 15, 2022, offered an environment for idiosyncratic mortgage stress, as interest rates began to increase rapidly.1 MDX swap pricing can be estimated for these periods using CDX IG and CRT spreads as benchmarks. To accomplish this process, loss-adjusted risk premiums are derived from CDX IG and combined with CRT spreads adjusted for differences in structure, collateral, and funding. All spreads are annual. |