|

MARKET COMMENTARY

Federal Reserve's Stance: The Fed remains in a "wait-and-see" posture regarding the decision to reduce short-term interest rates. Potential catalysts for making that decision include:

-

Economic Data: May's Personal Consumption Expenditures (PCE) report will be released on Friday, and is expected to show the slowest advance in consumption since Q4 2023, indicating economic weakness.

-

Upcoming Reports: The second revision of Q1’s GDP, Personal Consumption, and Quarterly Core PCE is due on Thursday, and May Personal Spending & Income is also due on Friday.

-

Market Movements: Investors are cautious to invest with weak data anticipated in the near future, and also considering the fact that this week is month/quarter-end, likely to lead to volatility in pricing this week.

Treasury Yields and Federal Reserve Actions

-

Treasury Yields: The benchmark 10-Yr Treasury yield ranged between 4.20% to 4.30%, above 4.10% for 73 consecutive trading days, only surpassed since 2007.

-

Interest Rate Outlook: A softer PCE print might provide further support for potential interest rate cuts. A 67.7% chance of a quarter-point rate cut in September is currently priced into the market.

-

Federal Reserve Speeches: Five voting and one non-voting Fed members will speak across eight engagements this week.

-

Treasury Auctions: This week includes $69 billion in 2-Yr Notes, $70 billion in 5-Yr Notes, and $44 billion in 7-Yr Notes.

Market Conditions and Investor Behavior

-

New Issuance Market: The mid-week holiday break induced sluggish trading in Agency CMBS with $500 million in Fannie Mae DUS/MBS trading, following a busy three-week stretch.

-

Investor Spreads:

-

Shorter Tenured Paper: 5-Yr paper spreads widened by 6-7 basis points due to saturation and growing broker/dealer inventories.

-

Longer Duration Paper: 7/6.5 and 10/9.5 structures saw only 2-4 bps widening.

-

Trading Activity: Ginnie Mae PL and CL new issue trading remains light. Credit spreads are steady with strong investor interest in PL’s and CL’s with first draws.

-

Market Bias is causing widening of investor spreads heading into quarter-end due to "window dressing" by investors and abnormally large inventories of treasuries on hand with dealers.

| |

|

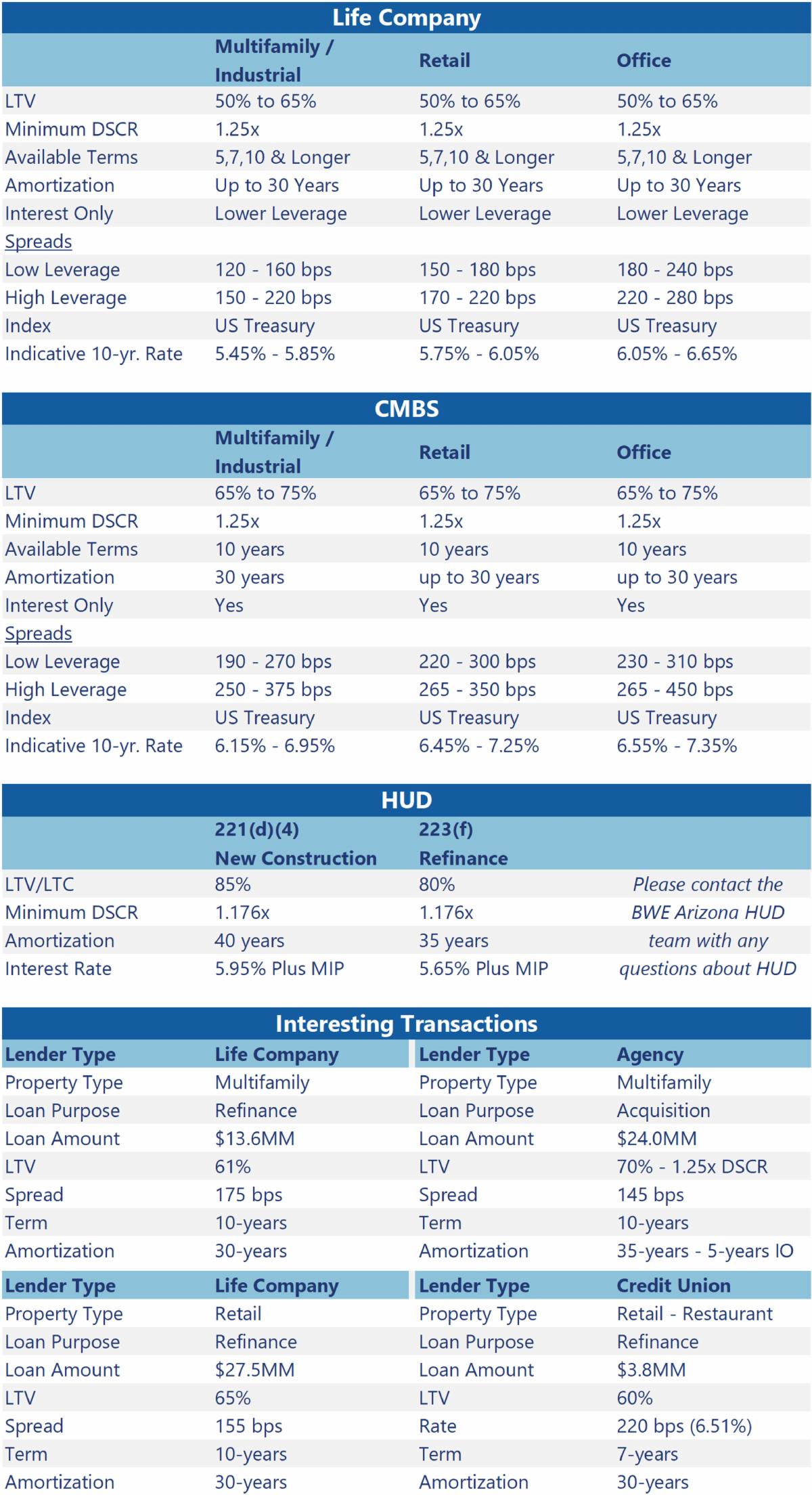

LIFE COMPANY

The onset of summer has not seen a slowdown in market activity. Life Company production by Bellwether is slightly ahead of the pace achieved a year ago. Allocations for the remainder of the year tend to fall into one of two camps – those with sufficient funding available and those that have already committed their 2024 allocation. Life Companies with available allocations have reaffirmed availability of short-term capital to meet demand by sponsors along with an abundance of long-term capital of 10-years or longer.

The benchmark 10-year US treasury index has settled over the past two weeks, settling within a range of 10 basis points averaging 4.25%. Over the same timeframe, we find lender spreads have ranged from mid-150 basis points to the low-200 basis points range depending on the quality, location and sponsorship. Outlier pricing for high-quality properties in primary markets with strong sponsors can garner spreads as low as 120 basis points. Single-A Corporate spreads to Treasuries have ticked up which may result in lender spreads moving slightly upward in coming weeks.

Highlights:

- Pricing has steadied over the past couple weeks due in part to US Treasuries experiencing less volatility.

- Current yielding spreads in the range of 1.55% – 2.20% for quality asset types like industrial and multifamily properties with good lending metrics.

- As of recent, our network of life companies continue to make short-term capital with flexible prepayment options available to meet market demand.

| |

|

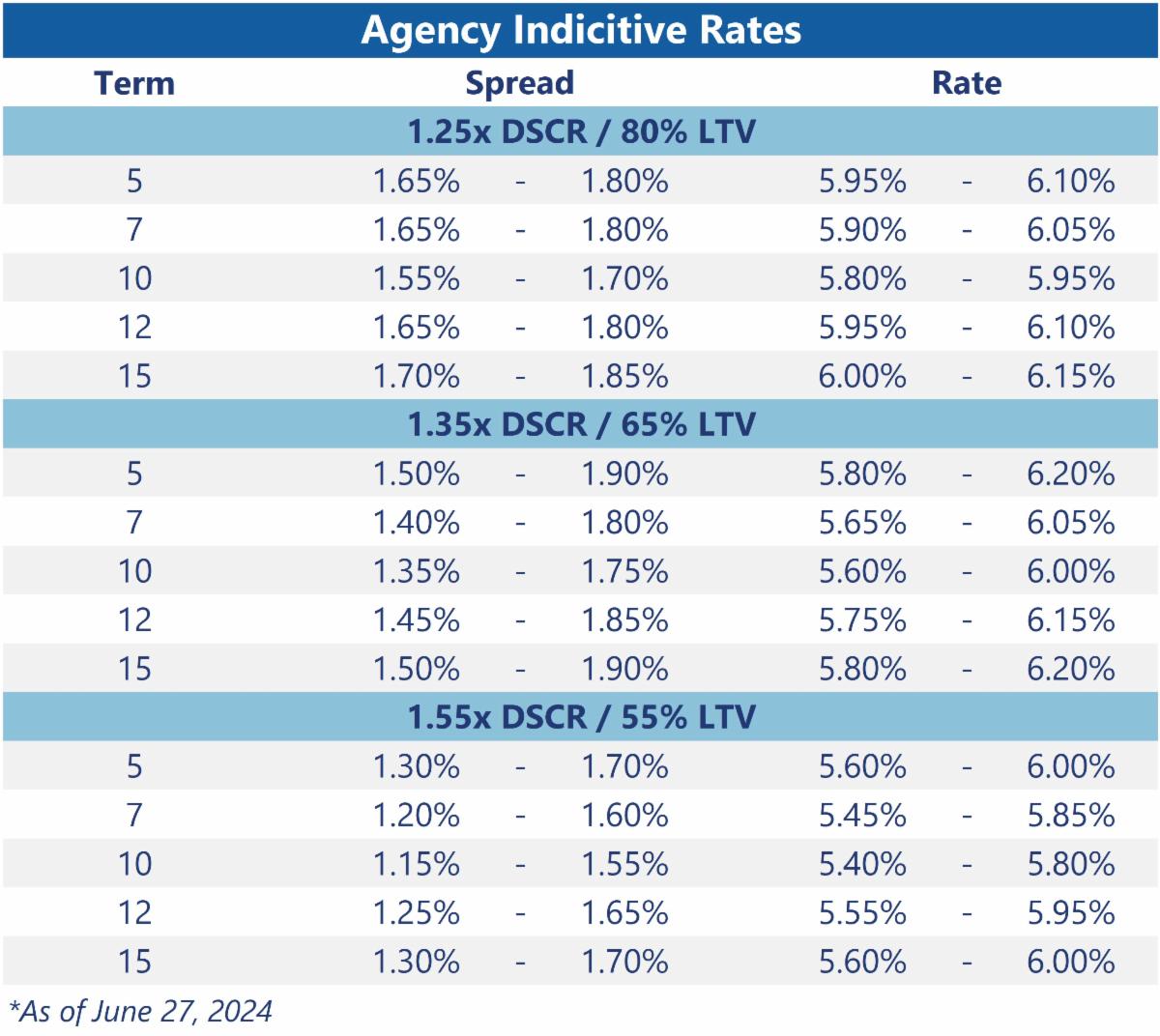

AGENCIES

The drop in Treasury yields over the past few weeks has amplified Agency CMBS new origination volumes above their year-to-date weekly averages. The June DUS origination volume weekly average hovers at around $890 million so far while the year-to-date weekly average sits at $570 million. This sudden “pop” in new supply has weighed on end investors’ buying appetite and caused investor spreads to widen +2-5 bps across the board last week. Specifically, Agency transactions with a 5-year loan term continued to dominate rate lock activity last week, which led Agency CMBS traders to pull back on price clearing levels and exposed fatigue in shorter duration paper.

In correlation, part of the spread widening may also be attributed to the mid-week holiday last week, effects of quarter-end positioning, and dealer inventories expanding. The “choppy” environment has caused investors to be even more sensitive towards illiquid deals which bear flexible prepayment structures, supplemental loans, small loan sizes, etc. In contrast, and a condition that has been prevalent for months, investors remain keenly focused on Agency deals that contain lower-leverage, full-term interest-only, interest rate “buy-downs,” and are larger than $20 million. Freddie Mac priced $103 million in their PC Deals in line with expectations.

Highlights:

- Fannie Mae & Freddie Mac Origination Volumes through May & YTD

- Fannie Mae

- May 2024 = $2.7 billion

- YTD 2024 = $15.4 billion (down 20% YoY)

- Freddie Mac

- May 2024 = $3.1 billion

- YTD 2024 = $17.0 billion (up 20% YoY)

- BWE's Agency volume is up 20% YTD Overall with both agencies

- Student Housing Update

- Starting parameters are 65%/1.35x. For sponsors with very strong student experience in the right markets and locations. Freddie will entertain 70%/1.30x

- Agencies are focused on sponsor’s student housing experience and experience in the market we’re the deal is located.

- Min student body 15k. Freddie will potentially look at min 10k student body

- Focused on positive enrollment trends and property’s location to campus. Located within 2 miles.

- Will look at using the 2024/2025 rents.

- High Interest in 5-year Structures with Flex Prepay

- We’ve seen an overwhelming increase in 5 year fixed rate requests with flexible prepay.

- The most common structure is 5 years fixed with the last 2 years open at PAR.

- Supplemental Financing Opportunities

- The agency team is seeing an increase in supplemental opportunities that lower the tier of the deal's original loan (ie. Tier 3 to Tier 2)

- These requests include an additional adder to the pricing, but the blended rate between the original note rate and the new supplemental still results in a competitive overall rate.

- Original Loan - 3.5%

- Supplemental - 7.0%

- New Blended Rate - 5.0%

- This structure is becoming more prevalent with acquisitions.

- Pricing Observations

- The most common structure right now is a 1.25x DSCR and 65% LTV. This is generally pricing in the 150-170 bps range

- Higher LTV - We are seeing some deals with higher LTVs pricing around 180 bps

- Lower LTV - Many low leveraged deals are pricing well below 150 bps

- Fannie Mae Tier 4 deals with 75% at 80% of AMI are pricing 110-120 bps over before buydowns

| |

|

HUD

HUD remains a top option for refinancing market-rate projects transitioning from construction loans. Key advantages include a low debt service coverage ratio of 1.176x, competitive fixed interest rates, and 35-year fully amortizing, non-recourse loans that are fully assumable. Under certain conditions, cash-out refinancing is also possible. A recent refinancing of a stabilized new construction project provided enough proceeds to retire the entire construction loan without additional equity, thanks to the low DSC and competitive rates.

HUD financing for both new construction and multifamily project refinancing offers some of the highest leverage in the market today. We are consistently seeing new construction loans in the 75-85% LTC range and refinancing loans in the 70-80% LTV range.

Highlights:

- New construction loans are typically sized between 70%-85% LTC, with refinancing loans in the 70%-80% range.

- HUD offers insured loan products in both large metropolitan and smaller secondary and tertiary markets, meeting the demand for housing.

-

Our highly experienced FHA/HUD team recently closed a $39.4M HUD 221(d)4 New Construction loan for Market Rate Multifamily Property in Pueblo Springs, CO. For more information, please review the recent press release: BWE $39.4MM 221(d)4 New Construction Loan

Please contact BWE Arizona HUD team if you have any questions about the above updates and how they might apply to your project.

| |

CMBS

The surge in CMBS issuance this year is reflective of a wave of maturing loans facing the industry. Spreads haven't changed significantly, with 10-year loans priced in the low-to-mid 200s over Treasuries and 5-year loans in the mid-to-high 200s. For multifamily properties specifically, CMBS lenders are continuing to offer full-term interest-only financing. This structure allows lenders to push proceeds by underwriting down to a 1.20x debt service coverage ratio on an IO basis, making financing more attractive for multifamily property owners.

|

| |

|

|

STEFANIE VANBEEKUM

VICE PRESIDENT

Email: Stefanie.VanBeekum@bwe.com

Direct: 602.423.2142

20555 N. Pima Rd, Suite O-140

Scottsdale, AZ 85255

| |

Opinions, estimates, forecasts and other information contained in this document are those of Bellwether Enterprise Real Estate Capital, LLC (“Bellwether”) and should not be construed as indicating Bellwether’s business prospects or expected results. Although Bellwether attempts to provide reliable, useful information, it does not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is provided on an “as is” basis, with no warranties of any kind whatsoever and is subject to change at any time without notice. Information in this document may not be used without permission from Bellwether. This document is not intended to be an offer to buy or sell or a solicitation of an offer to buy or sell securities, if any, referred to herein.

| |

Bellwether Enterprise Real Estate Capital, LLC (BWE) conducts business through Bellwether Enterprise Mortgage Investments, LLC – Mortgage Banker license #BK-1007784 – the Department of Financial Institutions State of AZ. (Fannie Mae transactions), as well as Bellwether Enterprise Real Estate Capital, LLC – Mortgage Banker License #BK-1007825 – the Department of Financial Instituti9ons State of AZ (all other transactions). | | | | |