|

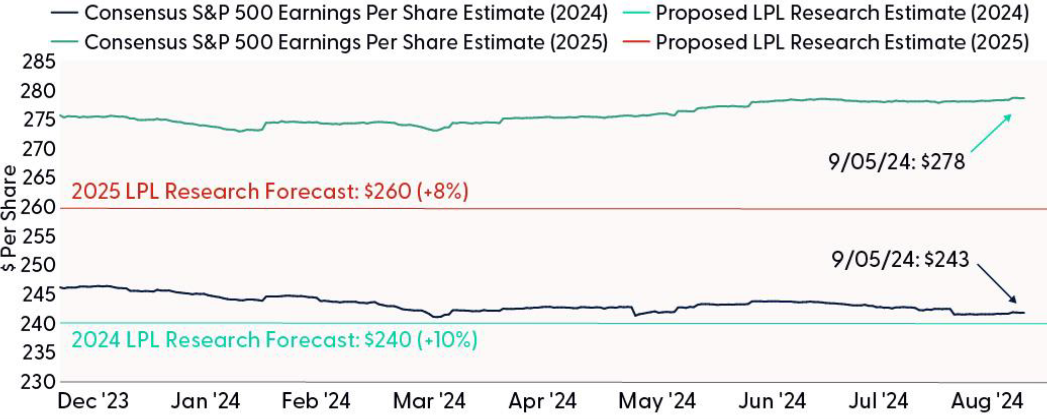

Source: LPL Research, FactSet 09/05/24

Past performance is no guarantee of future results. Estimates may not develop as predicted.

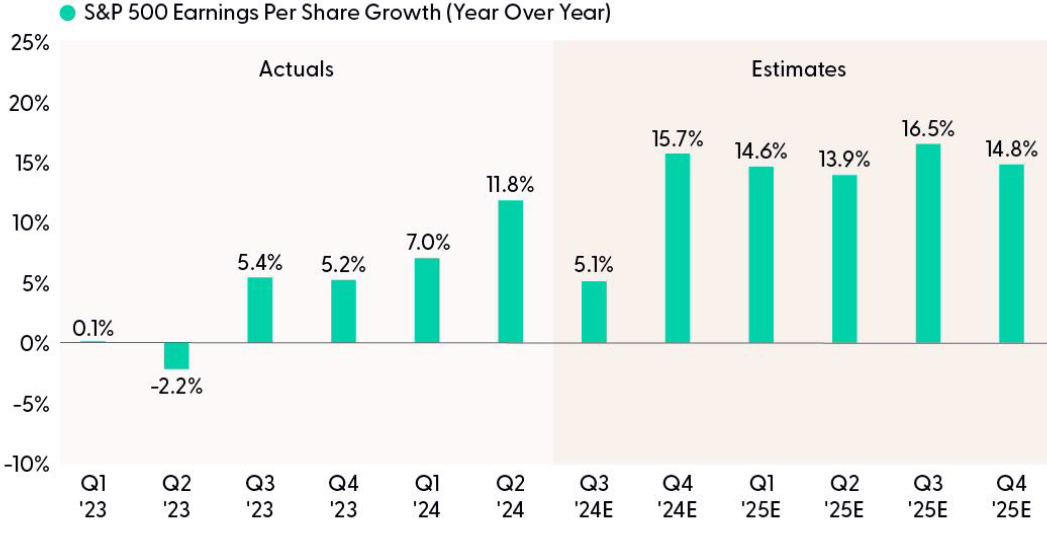

In that earnings preview, we cited resilience of estimates during the second quarter, steady economic growth, and healthy Asian export activity as reasons to expect good results overall. Those factors certainly contributed to solid revenue growth for the S&P 500 of 5.2%.

At the same time, a strong U.S. dollar, weak manufacturing surveys, and sub-par economic surprise indexes (most U.S. data fell short of economists’ forecasts from mid-April through mid-July) suggested capped upside potential. Those factors did contribute to less upside to estimates, with an average upside earnings surprise below 4% after average surprises over 7% in three of the prior four quarters.

Technology Got By With a Little Help From Its Friends

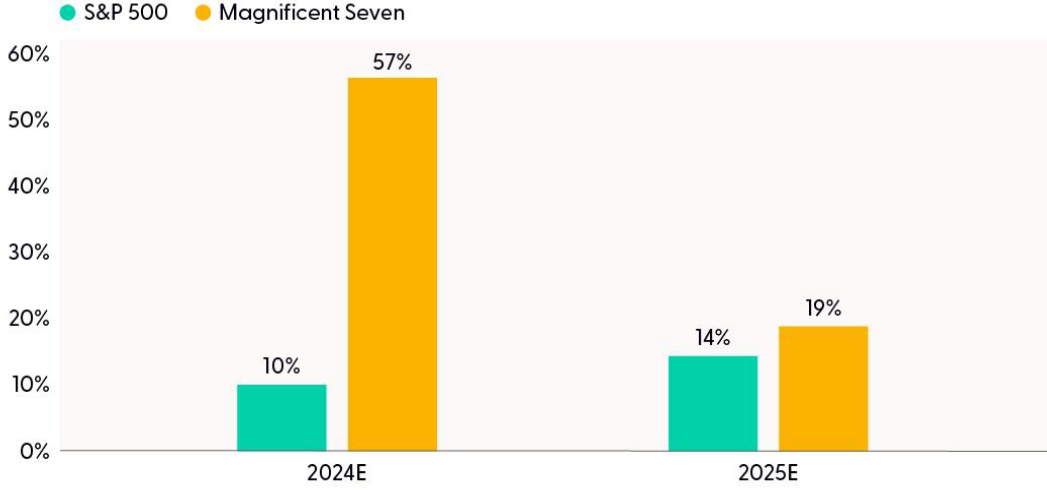

We had expected mega cap technology companies to be big drivers of earnings growth, and they were. More than six percentage points, or more than half of the S&P 500 EPS growth last quarter came from the top six technology companies — Alphabet (GOOG/L), Amazon (AMZN), Apple (AAPL), Meta (META), Microsoft (MSFT), and NVIDIA (NVDA).

The other 494 contributed slightly less than six points, still a solid improvement from recent quarters. Healthcare and financials made solid earnings contributions. In fact, a strong second quarter earnings season was one of the reasons for our upgrade of the healthcare sector last week to neutral from underweight. The sector grew earnings year over year for the first time since Q2 2022. Strength in consumer finance and insurance helped drive solid upside for the financial sector, where our asset allocation committee maintains its neutral stance.

Markets Weren’t Impressed

Perhaps the most disappointing thing about second quarter earnings season was the market reaction. From July 15 through the end of August, the S&P 500 was essentially flat, including an 8.5% drop that culminated in the volatility spike on August 5. The good news is the S&P 500 rallied back on results in August, at least before using NVDA results on August 28 as a reason to pull back again — though by only about 3% so far. Results weren’t enough to drive stocks higher, but it’s fair to say they were a key factor — along with falling inflation and supportive economic data after the weak July job report (released on August 2) — in helping stocks recover most of the 8.5% drawdown in less than three weeks.

Forward four quarter S&P 500 EPS estimates fell just 1% during the Q2 reporting season, about half the typical cut and a good result. The percentage of companies reducing guidance was slightly better than the norm. However, it wasn’t good enough to drive stocks higher as the soft-landing debate continued and seasonality, geopolitical threats, and policy uncertainty added to the headwinds.

Earnings Growth Gap Between the Magnificent Seven and the “493” is Narrowing

As noted above, the Magnificent Seven drove more than half the earnings growth last quarter. For just six companies (Tesla’s (TSLA) earnings fell, but we’ll still count it as one of the Seven) to drive that much earnings growth for an index of over 500 public companies is remarkable. The average earnings growth for those six in the quarter was over 60% (for all seven it was 46%) and it should be around that same rate for the full year 2024. That is tremendous growth, especially for such large companies.

The massive capital expenditures into artificial intelligence (AI) have made us hesitant to recommend an overweight to value stocks — although outperformance by value stocks over the past six weeks is encouraging.

One of the reasons our asset allocation committee is starting to get more interested in value stocks is the broadening out of earnings growth. The “493” certainly aren’t seeing anywhere close to the earnings growth the Magnificent Seven is currently seeing (TSLA aside). But in the coming quarters that gap will narrow quite a bit, which we would expect to be a catalyst for the value-leaning 493. The broadening out of earnings growth is positive for the health of this bull market, but the massive weight of the big technology names may make for a bumpy transition to potential value outperformance.

Earnings Growth Gap Between S&P 500 and Magnificent Seven To Narrow in 2025

|