|

RETIREMENT SECURITY MATTERS

A forum for retirement innovation information sharing

focused on states, supporters, and service providers.

Vol 68 | December 15, 2022

| | |

Greetings! Lisa, welcome to Retirement Security Matters – where we talk about retirement readiness innovation by the public sector, private sector, and policy organizations. | |

While you’re busy with the hustle and bustle with friends, family, and your community all preparing to celebrate the big holidays, don’t forget to pause and nourish yourself a bit along the way. Curl up for a moment in those footie socks with some wassail and catch yourself up:

-

Martha Deevy on optimizing 100-year lives and the importance of financial resiliency

- Key updates from California, Colorado, Delaware, Maryland, New York State, and Virginia

-

DCIIA, The Aspen Institute, and Morningstar – joint venture in expanding equitable retirement

- What’s one piece of hopeful news you heard this week? – check out Hot Sauce and Cool Stuff

- Pix of the week to boost your day

| Comments or content suggestions? We welcome both. Have something about your program you’d like to share? We are all ears. | |

|

RSM wants your support! Be seen here.

Click here for more information.

| |

The 100-year life is here and the importance of financial resiliency

| | |

|

|

This week we have the pleasure of chatting with Martha Deevy of the Stanford Center on Longevity.

Martha has more than 25 years in senior executive positions at Intuit, Charles Schwab and Apple. Since 2009, Senior Research Scholar and Director, Financial Security Program, Stanford Center on Longevity, focused on re-imagining how we plan for retirement and how we live in retirement.

Let’s jump in! (This is an excerpt. The full piece can be found HERE.)

| |

|

Martha Deevy,

Associate Director, Stanford Center on Longevity

| |

You're at this super interesting intersection between financial services, technology, and longevity. What's exciting to you as you think about those three things working together?

I feel like I've seen the world from two sides now. What I have been enlightened by since being at Stanford really is how much good academic research is out there that can be applied to solving some of these real world problems. And I often say that I could have saved a lot of market research money when I was running businesses, if I only would have knocked on a few academic doors. Trying to bridge those worlds is really what I do; what I think I bring to the party. I think the power in pulling together good evidence-based research with the people who can impact and make the change is really powerful.

Martha, tell us about the Stanford Center on Longevity.

The Stanford Center on Longevity is 14 years old and it was co-founded by a psychologist gerontologist Laura Carstensen and a stem cell biologist Tom Rando. The interesting story of how it was established came about from a casual conversation [read the full story HERE]

And getting to work on this really meant identifying what are those cultural changes that we need to be paying attention to in order to optimize what will be 100-year lives?

We love that. The 100-year life is here, as you pointed out. What does that mean, Martha, and how should we be thinking about it?

We think optimizing 100-year lives is not just something that happens at the end of life. The most influential domains that really impact how well we live our 100-year lives. It's early childhood, education, health, healthy behaviors, and in the US healthcare, it's work and the future of work, and it's financial security. And notice that I'm not saying retirement. I am actually talking about financial security across the lifetime. We also think it's about changing things in our built environment and, of course, climate. We think changes need to be made and can be made. And there's evidence that indicates changes made in each of these domains really does begin to optimize lifetime wellbeing. Ultimately, it's not just making it to 100, but it's doing it healthfully, feeling cognitively fit and physically fit and financially secure.

As you pointed out, one of the tenets of this good long life is the need to build financial security from the beginning or from early on. As Americans, how are we doing based on what you see?

Not well. Most people aren't feeling financially secure, particularly as they near what they perceive to be retirement age. Whether it's questions of student debt (interestingly, many older adults carry), as well as the inability to save money to purchase a house. So, I think the conversation really needs to begin to change from one that talks about what do we have to do to retire? to one where think about how do we enable, and how do we make wise financial decisions across the whole life cycle?

I like to change the conversation around from financial security to financial resiliency.

(Continued HERE! Don’t miss the rest of Martha’s insights on changing how we think about financing long lives and the resources the Center has available for you)

What are you seeing that you really like, that feels very positive to you in terms of what we're doing? What keeps you awake at night that we need to spend more energy on?

What I'm really optimistic about is that younger generations will catalyze a lot of the changes that we're talking about. I think younger people are already thinking about, or already accepting and knowing they're going to live longer lives. They have a lot of good models of people who are living long and well.

And what keeps me up at night is asking what are we doing to help facilitate those changes for them?

Martha Deevy joined the Stanford Center on Longevity in January, 2009 and serves as Associate Director and Senior Research Scholar. While at the Center, she has led the financial security research program which has focused efforts on retirement readiness, working longer and the detection and prevention of fraud. You can connect with Martha on LinkedIn and by email here.

| |

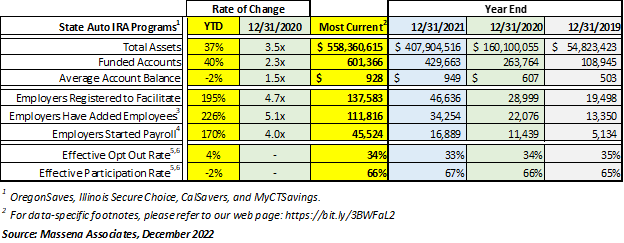

*Fresh!* State Auto IRA Program Metrics | |

|

What’s up! November figures are rolling in and we are seeing an upswing in new savers and retirement savings growth. Here’s what you need to know:

Saver assets have increased from our last report, up 51% year-to-date and 3.9x since December 2020. Average account balances are slightly increasines, now at $1,000.

The four programs shown here now aggregate to over 615,000 funded accounts. For comparison, funded accounts are up 43% this year so far, up 2.3x since December 2020 and up about 5.7x since December 2019.

Over 139,000 employers are now registered to facilitate a state Auto IRA. Of that number, more than 47,000 have begin forwarding payroll contributions for savers.

| |

State Facilitated Retirement Programs - Fresh Highlights | |

|

California (workforce 19.2 million) – The CalSavers Retirement Savings Board will meet briefly today, December 15, 2022, to discuss future engagement with program administrator Ascensus. Executive Director Katie Selenski will present the results of recent negotiations with Ascensus for the Board to consider approving amendments to its contract. You can get your copy of the agenda and proposed amendments here.

The Board has issued proposed rules a notification of proposed emergency regulation action to adopt emergency regulations amendments that were approved by the Board in November 2022. If approved, the regulations amendments would conform the program's regulations to match the recently passed Senate Bill 1126 that was signed into law in August 2022. An opportunity to submit public comments will be provided after the file is delivered to the Office of Administrative Law. We’ll keep you posted when public comment period begins. You may review the proposed regulatory language and Finding of Emergency on the Program website here.

| |

|

Colorado (workforce 3.2 million) – The Colorado SecureSavings Program Board met on December 6, 2022. The agenda included an ESG discussion, as well as an update from Executive Director Hunter Railey and team on implementation, data acquisition, partner programs, key outreach areas for 2023, and *drum roll please* rollout plan as the program launches in January 2023. The first deadline is March 15, 2023, for every employer with 50 or more employees; that will be followed two months later by the May 15, 2023, deadline for every employer with 15 to 49 employees; and the last wave will be on June 30, 2023, for employers with five or more employees. Check out the confirmed employer registration timelines here.

Provider Vestwell also gave an update on pilot launch, implementation of registration/onboarding sessions and results to date - overall positive feedback received from employers [Woohoo!].

Finally, Colorado SecureSavings welcomes new board member, Jennifer Luce, who brings banking industry experience to the Board. Jennifer currently serves as the Executive Vice President of FirstBank leading the South Market and serves on the board of multiple non-profit organizations.

| |

|

Delaware (workforce 499,000) – The Office of the State Treasurer officially published details seeking proposals from qualified firms interested in providing Program Consulting Services to the State of Delaware, as related to the Delaware Expanding Access to Retirement & Necessary Savings (EARNS) Program. Deadline for Bid Responses is January 17, 2023. You can get your copy of the RFP here.

| |

|

Maryland (workforce 3.2 million) – The Maryland Small Business Retirement Savings Board met on December 12, 2022. The agenda included an update from Executive Director Glenn Simmons on the first three months of the program with more than 1,140 employers registered, update from Marketing Director Chris Cullen on marketing activities and impact, as well as an update from the Audit and Finance Committee. Finally, Maryland $aves welcomes new Finance Director, Janaki Kannan.

| |

|

Virginia (workforce 4.3 million) – RetirePath Virginia is still recruiting employers for its Pilot Program. Businesses will be considered based on a variety of factors, including location, industry, size, payroll provider, and reach for an effective program trial prior to the statewide RetirePath Virginia launch. Here’s a good place to stay informed.

| |

|

C O M I N G U P

Join where you’d like, and count on us to follow these meetings for you:

-

California (workforce 19.2 million) –The next meeting of the CalSavers Board is scheduled for December 15, 2023..

-

Oregon (workforce 2.2 million) – The next meeting of the OregonSaves Board is scheduled for February 7, 2023.

| |

Expanding Equitable Retirement: A DCIIA-ASPEN-Morningstar Initiative | |

Retirement savings are the second-largest source of household wealth for Americans. Yet we know that this system is inequitable and is not creating security and wealth for everyone.

Let’s dive deeper. Disparity remains throughout race and gender across savings within the DC system, with nearly 60% of white households participate in retirement plans, compared to just 45% and 34% of Black and Hispanic families, respectively. The balance differential is substantial as well—the typical white household has nearly $50,000 in savings, which is 2.5 times that of Black and Hispanic families.

| |

|

We are pleased to share that DCIIA, The Aspen Institute, and Morningstar are partnering to develop fresh information that will enable action to close gaps within the retirement savings system. This project brings together stakeholders across the industry, including advisors, employers, recordkeepers, advocates and experts, working to better understand these differences and their underlying sources.

To support policymakers and financial services providers in their ability to improve retirement savings outcomes, we need to know a great deal more about workers of all kinds. The first step is understanding where we are now.

Can you be part of this work? We know many companies who currently provide services in the retirement industry and many employers have made substantial commitments to racial equity. There are three distinct ways industry leaders can get involved:

|

-

Share anonymized plan data. As an industry leader, adding your plan data to the universe will provide insight into your workforce and show your organization’s commitment to this important initiative.

-

Invite your plan sponsors. Your influence and connection with employers can strengthen the overall work of this project and enhance plan sponsor relationships.

-

Become a leadership partner. Join the efforts as a foundational partner, to help advise, direct, and influence this important initiative.

| |

|

Want to be part of the solution? Join us to make retirement saving a more inclusive instrument of wealth creation. To learn more about this ongoing initiative, click here or contact rrc@dciia.org for more information.

This piece was contributed by DCIIA’s Pam Hess and Simone Lamont, members of the DCIIA Retirement Research Center. Karen Andres and Kara Watkins of the Aspen Financial Security Program, and Aron Szapiro and Jack Vanderhei of Morningstar are also closely connected to this work, among others.

| |

|

Pew asks: What employer supports would help workers transition into retirement? To better understand these complex decisions about financing retirement, The Pew Charitable Trusts’ retirement savings project surveyed 1,125 older workers and recent retirees. The survey results indicated that employer-sponsored financial wellness programs do little to inform strategies for handling 401(k) assets. To learn more, check out the full report here.

We have to share this cool piece from Commonwealth. Did ADP’s solution facilitate $1.5 billion in emergency savings, and is emergency savings the foundation for financial security? We editorialize – as a precursor to retirement savings and other long term liquid assets that support retirement security. Because … retirement security matters. PS here's a recording of the webinar highlighting these findings.

A couple of nuggets from Stanford’s 2022 Century Summit. "Emotional life improves with age" -- as does wisdom, experience, and resilience -- as long as we are well connected, socially. Check out the new (need to look for it) Career Break work category on LinkedIn. So relevant! And we heard Maria Shriver comment within the conversation about radically reframing aging: “So often people who are aging do not feel cherished, or seen.” We see you.

New summary of research on delaying Social Security – by PGIM’s David Blanchett. It is true that when focusing only on DC balances, less than 10% of participants are estimated to be able to delay claiming Social Security benefits to age 70 while maintaining a reasonable liquidity cushion? And if so, what does that mean for plan sponsors? Check it out.

TikTok Time! We fell over when this young man said, “and my money I save for my retirement”. If you need to see an eleven-year-old boy speed-crocheting a quilt, this is your indulgence for today.

| |

... PIX! Please, we've earned it! | |

We have been working remotely from Oregon this week. so here are a few (moon) shots from the old homestead. That’s the moon. Look closer! | |

And, is there anything better than telling your robot vacuum to clean under the stairs? *we don’t think so*. He did have to have a full evacuation after finding his way into the fireplace. All set now though. That little red line makes log-town OFF LIMITS. Final pic: a man and his dog. | |

|

That’s it for this edition. ❤️ Hug your people and change the world.

If you like this piece, please stick with us. We’ll be back in about two weeks. If you don’t like it, please unsubscribe below. Comments for us? Please let us know. Want your own subscription? Request one here. All information shared is from public sources or used with express permission.

| |

Massena Associates provides process, policy, and implementation consulting on retirement savings programs and products.

Our clientele includes public entities, policy organizations, and private sector providers. Our specialty – efficient, targeted results. We are an active speaker on retirement security topics, including state-facilitated programs, MEPs and more.

If you’d like to explore working together, we welcome the conversation. Connect with us here, and at 339-236-0684.

| |

|

Looking for a great retirement savings innovation resource? Led by Dr. Alicia Munnell, the Center for Retirement Research at Boston College develops and hosts terrific content and proprietary research related to states, financial security, social security, and more.

The Defined Contribution Institutional Investment Association (DCIIA) is dedicated to enhancing the retirement security of America’s workers. To do this, DCIIA fosters a dialogue among the leaders of the defined contribution community who are passionate about improving defined contribution outcomes. DCIIA's site provides a range of public and member-specific resources.

The Georgetown Center for Retirement Initiatives, Exec Angela Antonelli, provides excellent information on state-based and other retirement security innovation and policy.

Pew’s Retirement Savings Project studies the challenges and opportunities for increasing retirement savings and is another great resource - check out the work of John Scott and his terrific team.

If you want a great source of broad-based, consumer-focused retirement news, Jeffrey H. Snyder’s The Morning Pulse is your ticket. You can subscribe here.

| | | | |