|

RETIREMENT SECURITY MATTERS

A forum for retirement innovation information sharing

focused on states, supporters, and service providers.

Vol 90 | December 14, 2023

| | |

Greetings! Lisa, welcome to Retirement Security Matters – where we talk about retirement readiness innovation by states, supporters, and service providers. | |

We are making our way out of Hannukah, into those critical ten days before Christmas Eve, and blasting toward the New Year. If you’re working, you are probably working very hard and in need of a good break. Grab a cocoa-coffee and let’s catch up on the latest from the world of retirement security. We’re going to start with some innovation:

| Comments or content suggestions? We welcome both. Have something about your program you’d like to share? We are all ears. | |

Serving Small Businesses with Starter K: with Guideline’s Jeff Rosenberger and Jeremy ‘Cabs’ Caballero

| |

|

(Photo: Jeremy Caballero and Jeff Rosenberger,

Co-founder and CPO, and COO, Guideline)

| |

|

There’s always something new in the retirement space – which for us lives at the fascinating intersection of tax law, legislation, technology, service, and innovative thinking. We’re excited to be here today with both the Cofounder and Chief Product Officer and the Chief Operating Officer for Guideline – Jeremy ‘Call me Cabs’ Caballero and Jeff Rosenberger. We're talking about what’s new in fintech – and how they view the emerging Starter 401(k) space. This is an excerpt - don’t miss our full conversation here.

Jeff, tell us a little about what the Guideline team have been doing since we last spoke for RSM. (See our chat from 2020)

It won’t surprise you to learn we are still very focused on serving small and mid-sized businesses. They play an enormous role in the US economy, employing tens of millions of workers.

When we launched in 2016, there were a little over 500,000 401(k) plans. Today there are 720,000 or so. It’s still not nearly enough, but around 200,000 plans were created during that time period. We've created about 20% of them, or 40,000 new plans. We're really proud of that.

That must make you one of the fastest growing new plan providers in the country. What’s working?

I think there was an element of good timing at the point when we got started. We also bring more of a software mindset to this space, versus a more traditional asset management mindset. Internally, we look more like a SaaS (software as a service) business than an asset manager. That’s put us in a position to be very focused on the small and mid-sized business clients.

Cabs, your background is not retirement services – tell us how that influences your product design approach.

You’re right – my background is very much not in finance. My expertise is studying people and how they interact with computers. That’s a different perspective than you might get from the classical finance and investments person. For me, it amplified some of the user experience problems I saw.

Let’s talk about the new stuff. What have you been building this year, Cabs?

Yeah – so we’ve got a lot going on! Over the past year we built a mobile app available both on Apple and Android formats. We did this because we’ve known for a while that many of our client’s employees don’t have formal workstations with desktop computers. Many of them are out in the field, working in restaurants, in dentist’s offices, and other on-the-move occupations. We want to give them an equivalent signup and account management opportunity and experience. And we find those who onboard, view and manage their 401(k)s online tend to save more toward retirement. So you get a double whammy.

We’ve also watched how new types of 401(k) plan designs work for employers. QACA – qualified automatic contribution arrangements – are one example. They allow for the use of auto-escalation, and work well for employers as they start to graduate from the simplest plans toward a mid market plan. For these employers having QACA available has been integral for us. And now we are expanding the other direction to include a Starter 401(k).

How do you see Starter K and Auto IRA fitting together – are they compatible, or competitive, Jeff?

I believe heavily in building and developing awareness and getting the word out on retirement savings and access. Together we are, with the state programs and new federal norms like automatic enrollment through the SECURE Act, making good progress and creating a moment for awareness and better savings levels.

I would point out that if there are 720,000 401(k) plans and about 6 million employers in the US, then at the employer level only about 12% actually offer a 401(k) plan. We think we see a set of stepping stones from no workplace retirement savings to very robust retirement offerings.

That can be a state Auto IRA program if the employer is not in a position to cover administrative costs. It could be a Starter K if they are in a position to cover some administrative costs, but not in a position to do an employer match or deal with non-discrimination testing. It could also be a full 401(k) plan – beginning with a Safe Harbor plan with a 3% or 4% match.

This is an excerpt - join for the rest of our conversation and see our comparative chart here.

Cabs and Jeff – kudos to you for your user-focused approach, and thank you for sharing your insights and innovation.

You can connect with Cabs and Jeff and follow the work of Guideline here.

Jeremy ‘Cabs’ Caballero is the co-founding Chief Product Officer for Guideline. Cabs’ background as Lead Product Designer and Head of User Experience includes companies from diverse spaces, such as TaskRabbit, TargetSafety, and Targa Trophy. He describes himself simply: Helping small business owners and their employees save for today and tomorrow. 15 years building startups. Obsessed with design. Champion of simplicity. Dad.

Jeff Rosenberger is the Chief Operating Officer at Guideline. Jeff has worked in fintech for almost two decades focused on asset management and lending, including as an early executive at Wealthfront where he helped build the market for direct-to-consumer robo advice. Jeff earned a PhD in Management Science & Engineering from Stanford, a BS in Statistics from UC Berkeley, and he holds the FINRA Series 65. Now that we know this we are going to start calling him Dr. Jeff.

| |

*Fresh!* State Auto IRA Program Metrics | |

|

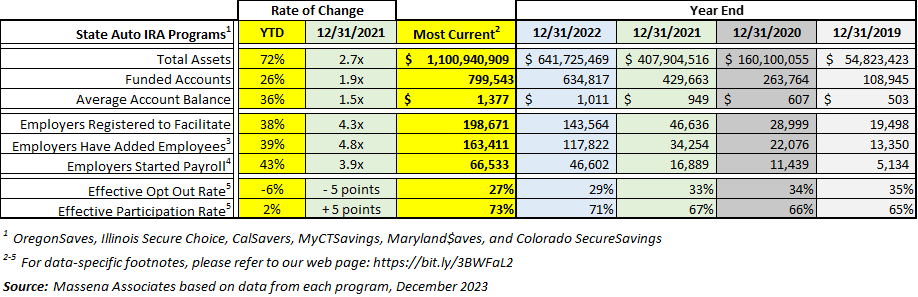

What’s up! 🥁 Drum roll please, ladies and gentlemen, the hardworking savers across the Auto IRA states have just achieved $1 billion in savings together. Our hearts are full. ♥️ Why? Because this part of proof of concept is complete: if you build it, they will use it. No idea is perfect, but you stuck your neck out, States. You built it and they are using it.

#Welldone. Much will be written about this and we're looking forward to seeing it.

Assets. The aggregated reporting Auto IRA states are reflecting $1.1 billion in assets as of November 30, 2023. Year to date assets are up 72%. By year end it is likely that assets will be 3x their level at the end of 2021, two years ago. Assets are now large enough that market impact has become a factor, and market growth is adding value to savers' accounts this month.

Funded accounts. We are now within a chef's kiss of 800,000 funded accounts. The next milestone to keep your eye on will be one million funded accounts, expected in 2024 - and it's your guess and mine how quickly this can be achieved. Account growth year to date is running at 26%, and over two years, running at close to 2x. Average account balances are just under $1,400 - more than twice their levels three years ago at the end of 2020.

Facilitating employers. Nearly 200,000 employers are registered to facilitate a state Auto IRA program. ♥️ As we have seen, about a third, or 66,000 have begun forwarding worker savings to program accounts and two-thirds are working their way through the facilitation pipeline in that direction. Imagine the power of these programs and savings when something approaching full rollout and more complete compliance is achieved. Programs with compliance efforts are seeing significant benefits from that activity.

| |

State Facilitated Retirement Programs - Fresh Highlights | |

|

Delaware (workforce 499,000) – This week Delaware Earns announces that it is joining the Partnership for a Dignified Retirement - hosted by Colorado Secure Savings. Delaware joins Maine and Colorado in this partnership. Maine has been able to get up and operating quickly, and we expect to see a similar opportunity for Delaware.

| |

|

Maine (workforce 677,000) – In fact the MERIT program is now live with funded accounts for the first savers from its pilot program. Although first employer deadlines aren’t until April of 2024, employers are able to register statewide starting in January and you can expect to see the program begin to grow. Maine's rollout is structured in two waves tailored to business size, with enrollment deadlines at April 30 (15+ EEs) and June 30 (5+ EEs).

| |

|

Virginia (workforce 4.3 million) – RetirePath Virginia continues its rollout – with a first deadline in September 2023 and a final deadline in February 2024 for covered employers with 25+ employees. Check out the latest, here.

| |

|

Freshen your cuppa joe and settle in for a few minutes of look-ahead. We think these are the top retirement savings innovation trends you’ll care about in 2024. Which ones will you be driving - we want to know!

- State Auto IRA Expansion:

State Auto IRA programs, designed to provide retirement savings options to workers without access to employer-sponsored plans, are expected to expand to more states in 2024. These programs automatically enroll eligible employees in an IRA, making it easier for workers to save for retirement. Stay tuned, the new legislative season is just around the corner.

The retirement industry will continue to invest in advanced digital tools and platforms to make retirement planning more accessible and user-friendly. This includes mobile apps, online calculators, and AI-driven financial advice platforms. We like this. A lot.

- ESG (Environmental, Social, and Governance) Investing:

The internet says ESG-focused retirement investment options will gain popularity in 2024. Investors are increasingly interested in aligning their retirement savings with their values, and asset managers will offer more ESG-compliant funds. This bucks recent headwinds, so we’ll see.

More private sector service providers will explore partnerships with fintech companies to offer innovative retirement savings solutions. These collaborations may include robo-advisors, micro-investment apps, and blockchain-based retirement products. These are longer term trends, as well.

Retirement income solutions will be a major focus in 2024. Providers will continue to develop products that help retirees convert their savings into a steady stream of income, addressing the challenge of outliving their savings. We’ve seen boatloads of both practical and forward-thinking work in this space in 2023. Expect more progress and adoption in 2024.

- Financial Wellness Programs:

Employers and states will increasingly prioritize financial wellness programs that offer education, tools, and resources to help individuals make informed decisions about their retirement savings.

- Target Date Funds (TDFs) Evolution:

Target Date Funds will continue to evolve, offering more customization and personalization options. TDFs will incorporate AI and data analytics to better align with individual retirement goals.

State and federal governments may introduce or firm up new regulations and incentives to encourage retirement savings, such as tax credits for low-income savers and increased contribution limits. We’re bullish on this. Saver’s Match sort-out, anyone?

- Auto-Escalation Features:

More retirement plans will incorporate auto-escalation features that automatically increase employees' contribution rates over time, ensuring they save more as their incomes grow. This is the quiet cousin to auto-enrollment, gaining recognition for its importance in supporting higher and more sufficient levels of saving over time.

The use of blockchain technology for enhancing the security and transparency of retirement accounts and transactions will gain traction. This can help protect retirement savings from fraud and cyber threats. We suspect this can’t happen fast enough.

Recap - more good things ahead - the retirement savings landscape in 2024 will see a continued emphasis on accessibility, digitalization, sustainability, and financial education. State Auto IRA programs will play a significant role in expanding retirement coverage to more workers, while innovative technologies and investment strategies will help individuals plan for a secure retirement future. And who knows - perhaps a federal standard for retirement savings access in the workplace will get some serious attention too. Stay tuned, friends.

| |

|

We admit it, we’re knee deep in the holidays over here and this is going to be a short curation!

One. From Boston College’s Center for Retirement Research, an analysis of the 2022 Survey of Consumer Finances (SCF) showing how 401(k) and IRA saving fared from 2019-2022. There’s good news - a meaningful increase in the median combined 401(k)/IRA balances for working households nearing retirement. And, since this period covers the heart of the pandemic and economic disruption, there is news that’s less good for younger savers.

Two. Our friends at EBRI give another take on the SCF. You’ve got to have an account to read their analysis, but you’ll find an interesting review of SCF methodology changes over time with positive notes on the survey data beginning in 2019.

OK, jingle bells and let’s get onto some fun stuff.

In our ears. We are enjoying the deliciousness of Robin Wall Kimmerer’s Braiding Sweetgrass. Part elegy to her childhood and family life, part wisdom and lore, part history, it’s hard to imagine this book read by anyone other than the author. She’s got a calming approach, even when touching sensitive subjects, perfect for frenetic times.

That’s it, and now …

| |

We've Got You: Pix of the Week! | |

Here’s our friend Jeff Rosenberger as Sisyphus – pushing the retirement savings expansion boulder – you’ve got this Jeff! #keepupthegreatwork | |

And, who doesn’t love a dog named Glacier in the winter time? Glacier is a beautiful English Cream Retriever – and awfully relaxing to look at. ♥️ Thank you for sharing, Jeff! | |

|

We hope you are all enjoying a lovely December month - taking time to soak in the joy of the season and to appreciate your friends and family in every moment. Our current motto: How you spend your time is how you spend your life. More eggnog, less stocking stuffers, we say.

That’s it for this edition. ❤️ Hug your people and change the world.

If you like this piece, please stick with us. We’ll be back in about two weeks. If you don’t like it, please unsubscribe below. Comments for us? Please let us know. Want your own subscription? Request one here. All information shared is from public sources or used with express permission.

| |

Massena Associates provides process, policy, and implementation consulting on retirement savings programs and products.

Our clientele includes public entities, policy organizations, and private sector providers. Our specialty – efficient, targeted results. We are an active speaker on retirement security topics, including state-facilitated programs, MEPs and more.

If you’d like to explore working together, we welcome the conversation. Connect with us here, and at 339-236-0684.

| |

|

Looking for a great retirement savings innovation resource? Led by Dr. Alicia Munnell, the Center for Retirement Research at Boston College develops and hosts terrific content and proprietary research related to states, financial security, social security, and more.

The Defined Contribution Institutional Investment Association (DCIIA) is dedicated to enhancing the retirement security of America’s workers. To do this, DCIIA fosters a dialogue among the leaders of the defined contribution community who are passionate about improving defined contribution outcomes. DCIIA's site provides a range of public and member-specific resources.

The Georgetown Center for Retirement Initiatives, Exec Angela Antonelli, provides excellent information on state-based and other retirement security innovation and policy.

Pew’s Retirement Savings Project studies the challenges and opportunities for increasing retirement savings and is another great resource - check out the work of John Scott and his terrific team.

If you want a great source of broad-based, consumer-focused retirement news, Jeffrey H. Snyder’s The Morning Pulse is your ticket. You can subscribe here.

| | | | |