|

RETIREMENT SECURITY MATTERS

A forum for retirement innovation information sharing

focused on states, supporters, and service providers.

Vol 79 | June 1, 2023

| | |

Greetings! Lisa, welcome to Retirement Security Matters – where we talk about retirement readiness innovation by states, supporters, and service providers. | |

Hurrah June - you bring something for everyone! We've just celebrated our Memorials, and now we are headed toward Juneteenth on our way through Pride month. Yes, we lik inclusivity. So, grab your iced coffee and let's catch you up on retirement savings coverage, innovation, and inclusion:

- Making retirement savings an inclusive instrument of wealth creation

- State metrics

- Updates from California, Colorado, Hawaii, Minnesota, and Nevada

- Pat GPT on how generative AI can be used to solve today’s challenging retirement, saving access, and inclusion puzzles

- Hot Sauce! …

- And celebrating family in our PIX of the Week!

| Comments or content suggestions? We welcome both. Have something about your program you’d like to share? We are all ears. | |

|

RSM wants your support! Be seen.

Click to grab this space for your brand.

| |

Collaborating for Equitable Retirement Savings (Outcomes) | |

(Art credit: DALL-E 2 with a little inspiration from us. This one is: an oil painting of people collaborating to build something in the style of Diego Rivera and wearing modern clothing.) | |

|

June 1 means the start of summer. A taking stock of where we’ve been so far in 2023, and where we are headed over the course of the year. We like to focus on retirement savings coverage, innovation, and inclusion here. 2023 is shaping up to be a really impactful year.

How so? Let us name a few of the ways:

-

The states are doing their part to extend coverage – 17 states now have programs authorized, and 14 of those are the impactful Auto IRA model. Although no state will capture all of its uncovered workforce, these states together represent 24 million uncovered workers, about 42% of the 57 million often cited. Progress will be slow. It may feel glacial. But it’s happening. Pew estimates that if all states were active, there’s about $1.3 billion in taxpayer dollars to be saved. We think we’re spending that raising the debt ceiling, so for the sake of our kids, let’s find a way to make some of it back.

-

SECURE 1.0 and 2.0 provisions are coming online. These start with extension of coverage to a wider swath of more permanent part time workers. That matters. The coverage provisions of the SECURE acts have been widely touted, but to be honest, actual extension of coverage through features like automatic enrollment for new plans is going to be experienced slowly, small new plan by small new plan.

-

Private sector innovation is helping to spark new plan adoption. We haven’t tried it, but we hear it’s getting crazy easy to set up a new plan. And more affordable, with more transparent cost and responsibility information. That matters.

-

The double impact of state Auto IRA deadlines and small plan innovation are spurring new plan formation, as shown in Pew’s longitudinal study of 5500 data in the US.

-

We also see a deeper focus on demographics through initiatives like the Collaborative for Equitable Retirement Savings, highlighted below. CFERS seeks to understand how workers who do have access to retirement plans are using them – and what sort of differences in outcomes we are seeing under different plan designs across a range of demographic cuts. This goes directly to inclusion and the ability of plans to effectively serve the wide range of workers covered in the US.

So let’s talk about CFERS. You’ll be hearing more about this over the next several years. Here’s a sneak peek at what’s coming.

Advancing Retirement Security and Equity: The Role of the Collaborative for Equitable Retirement Savings

The Collaborative for Equitable Retirement Savings (CFERS) is a joint initiative of DCIIA, the Aspen Institute Financial Security Program, and Morningstar Investment Management LLC that is working to transform the retirement savings landscape. Here we’ll explore two key facets of the Collaborative's work:

1. Understanding and Addressing Inequities in Retirement Savings

CFERS focuses on understanding and addressing the inequities in America's defined contribution retirement savings system. With $10.4 trillion in assets, the system is a significant wealth generator, but it's not working equally for everyone. It is, therefore, crucial to explore and understand how plan design and participant behavior lead to disparate outcomes for different demographic groups. By analyzing anonymized defined contribution transactional plan data, CFERS is shedding light on how participants from diverse demographic groups use, experience, and benefit from their retirement plans.

2. Promoting Industry-Wide Discussions and Initiatives for Equitable Retirement Savings

CFERS is fostering a broader discussion about retirement inclusion and the mitigation of wealth disparities. Through the publication of key findings and by organizing leadership discussions, CFERS promotes conversations about closing racial and gender wealth gaps starting with 401(k) plans.

Why is this Important Today?

The work of the CFERS is vital in the current socioeconomic context for several reasons. Firstly, the racial wealth gap in America remains a persistent issue, and the retirement savings system is one area where this gap can be addressed effectively.

Secondly, the economic fallout from the COVID-19 pandemic has further underscored the importance of financial security and resilience, particularly for marginalized communities that have been disproportionately affected. After home equity, retirement savings represent the second largest source of household wealth for Americans. And if, for you, home equity is a further-out goal, a small amount growing in a retirement savings account today may be your quick entry into the American wealth-building system.

By striving for a more equitable retirement savings system, the CFERS is contributing to the broader goals of financial inclusion and social justice.

If you’re interested in learning more, or considering how you may become involved, here’s where to go next: news and action.

This piece was written by Lisa Massena with a little help from her friend, Pat GPT. Pat definitely makes stuff up and has to be watched closely.

| |

*Fresh!* State Auto IRA Program Metrics | |

|

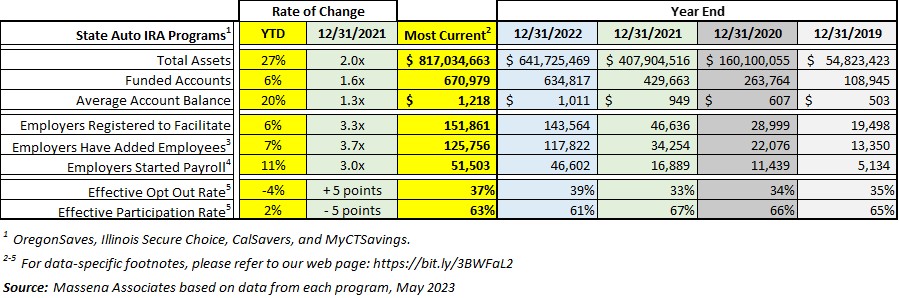

What’s up! We’ve got a full set of April data for the three long term Auto IRA states.

Assets. Saver assets are up 27% year-to-date and 2x since December 2021 to $817 million. Average account balances across the programs are over $1,200. Longer term balances are higher.

Funded accounts. The four programs shown here now aggregate to over 670,000 funded accounts. For comparison, funded accounts are up 1.6x since December 2021, up about 2.5x since December 2020 and up about 6.2x since December 2019 – and up in 2023.

Facilitating employers. Over 125,000 employers are now registered to facilitate a state Auto IRA. Of that number, more than 51,500 have begun forwarding payroll contributions for savers.

| |

State Facilitated Retirement Programs - Fresh Highlights | |

|

California (workforce 19.2 million) – The CalSavers Retirement Savings Board met on May 22, 2023. Key items on the agenda included an update on the ongoing search of the new executive director, a revised organizational chart, program participation, funding as of April 30, 2023, and update on employer compliance enforcement, amongst other topics; annual audited financial report for the fiscal year ending June 30, 2022; a report from program administrator Ascensus; and an investment performance report for the quarter ending March 31, 2023, by Meketa Investment Group.

At the meeting, the Board considered its Investment Policy Statement and approved emergency regulations amendments. If approved, the regulations amendments would amend the required data fields employers must provide to register with the CalSavers Retirement Savings Program.

| |

|

Colorado (workforce 3.2 million) – The Colorado SecureSavings Program has been featured in local news. “I think that everybody deserves a sustainable and dignified retirement. And right now we know there are a million people in the state of Colorado that aren't accumulating any savings, and they won't be sustainable on Social Security alone,” said Treasurer Dave Young in this interview.

| |

|

Hawaii (workforce 676,000) - The Hawaii Retirement Savings Program Board met on May 25, 2023, to progress its planning. Key items on the agenda included an overview of the Board’s requirements and responsibilities, hiring staff and consultants, preview of decision-making, amongst other topics. The agenda also included a review of best practices and lessons learned from other state retirement savings programs.

| |

|

A C T I V E

Don’t miss a great recap from Plansponsor on how legislators in Missouri and Minnesota passed bills to expand access to retirement savings for private sector employees, and Vermont legislators voted to change its approach.

Minnesota (workforce 3.1 million) It’s official! Minnesota became the latest state to officially launch a state-sponsored retirement plan for private-sector employees lacking coverage. Governor Tim Walz (D) signed HF782, the measure that creates the Minnesota Secure Choice retirement program, into law on May 19, 2023. For more see coverage by ASPPA.

Nevada (workforce 1.5 million) reintroduced a bill creating a state-supported retirement plan for workers who do not have access to one at their workplace on March 16, 2023. SB305 was read for the first time on May 30, 2023, and referenced to the Committee on Government Affairs. The bill would create the Nevada Employee Savings Trust, which would be directed by a board of trustees with the power to establish a retirement savings program and automatically enroll private employees. The program would be targeted to go live July 1, 2025.

See also the states we highlighted in RSM 78 & RSM 77 for a complete current view.

| |

|

C O M I N G U P

-

Oregon (workforce 2.2 million) – The next meeting of the OregonSaves Board is tentatively scheduled for August 15, 2023.

-

Illinois (workforce 6.4 million) – The next meeting of the Illinois Secure Choice Board is scheduled for today, August 17, 2023.

| |

AI Take on Retirement, Savings Access and Inclusion | |

|

Buckle up, buttercup. It’s the Summer of AI. We spend a lot of time talking with our friend Pat GPT. We asked Pat how generative AI can be used to solve today's challenging retirement, savings access and inclusion puzzles.

Pat had some pretty good ideas. Here’s what they said:

Generative AI, like the GPT models developed by OpenAI, has the potential to impact the field of retirement and savings access in several ways. Below, I've outlined a few possibilities:

1. Financial Education: AI can generate personalized educational materials to help individuals understand the importance of savings and retirement planning. This includes explaining complex financial concepts, providing actionable advice, and answering specific questions. AI can also adapt to the individual's knowledge level, learning style, and personal circumstances. And we wonder - can AI be used to improve the cultural relevance of communication for differing populations within a workforce? If it’s fast, cheap and easy, we just might do it.

2. Personalized Financial Planning: Generative AI could help develop personalized financial plans. By gathering data about an individual's financial situation, goals, and risk tolerance, AI can provide tailored advice to help them save for retirement. This could include suggesting specific investment strategies, calculating optimal savings rates, and forecasting future financial scenarios. Interesting. We might try this one. Can Pat do better than our brother-in-law Bob? (We love you, Bob)

3. Behavioral Nudging: AI can be used to nudge individuals towards better financial behaviors. For example, it could send reminders to save, congratulate users on meeting savings goals, or warn about the risks of overspending. Research shows that these types of nudges can significantly improve financial outcomes. Again - faster, cheaper, easier, more relevant? We like it.

4. Inclusion and Accessibility: AI can help bridge the gap in financial services for underserved populations. For instance, AI-powered apps can provide financial advice to individuals who lack access to traditional financial advisors. Furthermore, multilingual capabilities of AI can bring financial planning tools to non-English speaking communities, thereby increasing financial inclusion. Yes. Now we’re getting somewhere.

5. Policy Planning and Social Research: At a broader level, generative AI could be used to simulate various policy outcomes related to retirement and savings. For example, it could help assess the potential impacts of changes to social security, tax incentives for retirement savings, or minimum wage laws. This could inform better policy-making and social research. Interesting.

6. Fraud Detection and Security: AI can be used to detect patterns of fraudulent activity that could endanger someone's retirement savings. This includes identifying unusual transactions, predicting potential security threats, and alerting users or administrators to possible risks. Credit card companies are already excellent at this - let’s pull the capability over into the retirement savings infrastructure. We know it’s not cheap, though – is there a way of doing this without driving recordkeeping and administration costs through the roof?

7. Healthcare Planning: Given that healthcare is a significant concern for many retirees, AI can be used to predict future healthcare costs based on a person's health data and provide advice on saving for these expenses. Also interesting - anyone know what the current use cases are for health experience forecasting at the individual level?

Pat concludes: While these are promising potential applications, it's important to note that the use of AI in this field also raises important ethical and privacy considerations. The use of personal financial data must be handled with care to protect individual privacy and security. Additionally, it's crucial that AI tools are designed to provide accurate and unbiased advice. The deployment of AI in this field should be done responsibly, with these concerns in mind.

We thank our friend Pat GPT for its interesting insights into how generative AI can be used to solve some of today's challenging retirement, savings access and inclusion puzzles. We think Pat came up with some pretty good ideas. What do you think? To offer points and counterpoints, connect with us here.

| |

|

A quick curation of a few things you won’t want to miss this week.

One. A few great resources from our friends and Sunny Day Fund:

How do people save? - Join this webinar to learn from active practitioners and researchers on how behavioral science can foster savings habits.

What to ask in a workplace emergency savings program RFP? - Sunny Day Fund has distilled their experience into a framework you can adopt as you put together your RFP.

Yes let's learn more on strategy, design and implementation. Here's a recording from a recent webinar “Workplace Emergency Savings Accounts Tips from a Total Rewards Leader" with Erica Hayton, who leads Total Rewards at Cystic Fibrosis Foundation (CFF).

Two. As a follow up to today’s piece - we couldn't agree more with Vanguard Group CEO Mortimer J. "Tim" Buckley that “AI will revolutionize asset management”. During the Investment Company Institute Leadership Summit Tim added "So this is this revolution: As we move along, we will change our jobs, we'll change what we do, and we'll move up to that higher-order thinking (adding) more and more value for our clients. So we embrace it." For more, see the coverage by Pensions & Investments (subscription may be needed to view this piece).

Three. And your weekly dose of Three Not-So-Bad Things on Aging and Longevity on Martha Stewart cover at Sports Illustrated and thoughts around “how society says people should act, and what good things happen when people push against stereotype.”

Four. As we said, this month Minnesota brings the count of state-facilitated retirement plans to 17. Check out this great piece from Planadviser featuring some of our esteemed friends and colleagues on how small business providers confirm that state engagement helps boost business despite state-provided auto-IRAs.

Five … Service sector employees lead DC plan contributions. According to a recent report by ISS Market Intelligence, workers from sectors focused on service accounted for $5.7 trillion in AUM in DC plans, doubling over the last decade. For more, read Planadviser's recent piece.

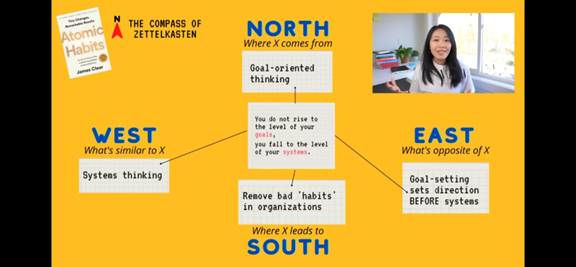

Cool way of thinking about things. We’re always trying to get more organized. So here’s a cool new way to think about how we take and organize our notes, from Vicky Zhao. Warning, that was a Youtube link. We hope you didn’t click that with the volume on while scrolling through RSM in a meeting at work. Just sayin.

We love this diagram for interrogating ideas in our notes.

| |

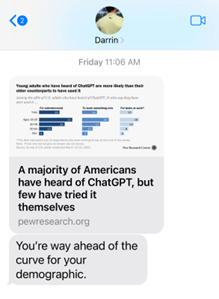

Andddd … this is what it looks like when your younger brother gives you a back-handed compliment: | |

“For your demographic” - ouch, Bro! That stings! But check out the data. Cuz we love data. | |

OK That’s Enough – give us the Pix of the Week! | |

Here’s one from the Massena mini-farm in Auburn, Washington. Celebrating family. In this shot, three siblings, two brothers-in-law, and a son-nephew. Doesn’t this angle make our legs look great? | |

And a little quiet time with the sheep. There’s a human out there in the mix, if you look closely. | |

|

That’s it for this edition. ❤️ Hug your people and change the world.

If you like this piece, please stick with us. We’ll be back in about two weeks. If you don’t like it, please unsubscribe below. Comments for us? Please let us know. Want your own subscription? Request one here. All information shared is from public sources or used with express permission.

| |

Massena Associates provides process, policy, and implementation consulting on retirement savings programs and products.

Our clientele includes public entities, policy organizations, and private sector providers. Our specialty – efficient, targeted results. We are an active speaker on retirement security topics, including state-facilitated programs, MEPs and more.

If you’d like to explore working together, we welcome the conversation. Connect with us here, and at 339-236-0684.

| |

|

Looking for a great retirement savings innovation resource? Led by Dr. Alicia Munnell, the Center for Retirement Research at Boston College develops and hosts terrific content and proprietary research related to states, financial security, social security, and more.

The Defined Contribution Institutional Investment Association (DCIIA) is dedicated to enhancing the retirement security of America’s workers. To do this, DCIIA fosters a dialogue among the leaders of the defined contribution community who are passionate about improving defined contribution outcomes. DCIIA's site provides a range of public and member-specific resources.

The Georgetown Center for Retirement Initiatives, Exec Angela Antonelli, provides excellent information on state-based and other retirement security innovation and policy.

Pew’s Retirement Savings Project studies the challenges and opportunities for increasing retirement savings and is another great resource - check out the work of John Scott and his terrific team.

If you want a great source of broad-based, consumer-focused retirement news, Jeffrey H. Snyder’s The Morning Pulse is your ticket. You can subscribe here.

| | | | |