|

RETIREMENT SECURITY MATTERS

A forum for retirement innovation information sharing

focused on states, supporters, and service providers.

Vol 61 | September 8, 2022

| | |

Greetings! Lisa, welcome to Retirement Security Matters – where we talk about retirement readiness innovation by the public sector, private sector, and policy organizations. | |

We’re enjoying early fall – that season where there’s a nip in the morning air but you’re sure you should be wearing shorts with your neighbors in the afternoon. That is, unless you’re back in the office! Wherever you are, we’ve got cool stuff for you. Settle in for the first-of-fall updates:

-

CalSavers leaps forward with Katie Selenski

-

We've crossed the $500 million mark! -- state metrics

-

Updates from California, Colorado & New Mexico, Illinois, Maine, Maryland, Oregon, Vermont, and Delaware

-

Who present-bias, me? Duke’s Perry Wright on precommitment.

-

Hot Sauce! Fresh research and some brain expanders

-

Pix of the week, from balancing on the SUP to ballparking together ...

| Comments or content suggestions? We welcome both. Have something about your program you’d like to share? We are all ears. | |

|

RSM wants your support! Be seen here.

Click here for more information.

| |

CalSavers: 340,000 New Savers, and Counting | | |

|

|

This week we have the pleasure together of chatting with Katie Selenski, Executive Director of CalSavers. Since 2017, Katie has been in charge of what has quickly become – and is likely to remain – the nation’s largest Auto IRA program.

While success is wonderful, the challenges are also very real. We spoke in mid-August, so don’t miss our Postscript and some important new news at the end.

| |

Katie Selenski, Executive Director of CalSavers | |

|

Katie, CalSavers just passed its third deadline – this one for employers with five or more employees, and no retirement plan. Give us an update.

Yes, it's so exciting. In a nutshell, we just crushed our expectations. We doubled the number of registered employers to 100,000 just in the last six weeks, and we are starting to see the new account surge beginning and savers’ money flowing in. This is what we’ve been waiting for.

The press around the program has been positive, very focused on awareness and making sure employers know this is real and what needs to be done.

This year we’ve been focused on driving more local news coverage so that employers know what they need to be doing to comply and avoid penalties. We also want workers to know what's coming as they're deciding whether or not to become savers.

It's taken a lot of effort to get to this point, Katie. What are you glad you have done?

There are so many things. I'm just so proud of our collective team - both our staff here in Sacramento and our partners, especially at Ascensus. I’ll share a few highlights.

Along with Ascensus, we launched a public live and interactive webinar series; enforcement with patience and grace has been very impactful - for each wave, we have a fairly generous time period where we’re sending increasingly firm follow-up messages; and our multilingual approach to this work – our website and most of our materials are available in ten languages (increasing it to 15 soon), and the call center, to the credit of the Ascensus, services calls in more than 40 languages.

Tell us about some of your bigger challenges, and what’s useful for peer states to know?

Yes. Well, the volumes. Anytime you have 92% of your universe of volume having a deadline on the same day, that's just going to pose challenges.

(Continued HERE Don’t miss the rest of Katie’s essential insights on deadlines, upcoming CalSaves focus areas, the right ways to engage in an auto enroll environment and much more)

As you know, we’re currently working on a bill that would expand our program substantially. The bill would lower our threshold for mandated employers from five employees or more, to one non-owner employee or more and allow us to fulfill our mission to ensure all Californians have a path to financial security in retirement

About how many affected workers do you think this would cover in California?

Our estimate based on last year’s data is about 300,000 employers, employing about 750,000 people.

Wow. Shifting directions: What are your thoughts on some of the federal proposals to expand coverage, including to states who may never establish an Auto IRA program?

I think that the most aggressive proposal we've seen was the Build Back Better retirement section including a national standard, potentially with state programs fitting into the national solution.

I personally am very supportive of that and think it would have made a big difference, even though we knew that that might not have the greatest chance of going all the way. We focus on what's in the best interest of our savers in California. And we can appreciate that folks in other states might like to have this sort of coverage too.

POST SCRIPT. On Friday, August 26, Governor Newsom did indeed sign the CalSavers Expansion Bill sponsored by State Treasurer Fiona Ma and authored by Senator Dave Cortese.

Katie, thank you for your perspective and insights. We couldn’t be more pleased with CalSavers’ success and impact.

Katie Selenski is the inaugural Executive Director of CalSavers, the State of California’s pioneering retirement savings program for the millions of Californians who lack access to a retirement plan at work. Appointed by the State Treasurer in 2017 shortly after legislative passage, Ms. Selenski took CalSavers through design, build, launch, and growth. Please see her full bio here.

| |

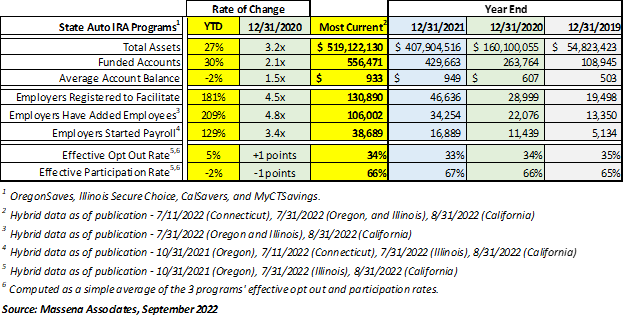

*Fresh!* State Auto IRA Program Metrics | |

|

*Forgive all these footnotes! Here’s what you need to know: August figures are starting to roll in, and we’ve reached a new milestone.

*ding ding ding* Consolidated program assets have just crossed the half-billion-dollar mark, supported by August 31 results from CalSavers. We're currently at $521 million.

Across these four programs you’ll find we are also at more than 556,000 funded accounts. That’s up 120,000 savers since the start of the year and 2x since the end of 2020.

Over 130,000 employers are registered to facilitate, although only slightly more than a quarter of that number have hit the GO button and started to forward participant savings to their retirement accounts. However, expect those numbers to go up in the next few months. Finally, effective opt out rates are up slightly with effective participation rate declining a bit, to December 2020 levels.

(PS: You may recall we had an office wager going on that $500 million mark. Staffer Melanie Lewis wins with the closest date. Well done Melanie! Dinner's on us.)

| |

State Facilitated Retirement Programs - Fresh Highlights | |

|

California (workforce 19 million) – The CalSavers Retirement Savings Board met August 22, 2022. Key items on the agenda included a summary report from Executive Director Katie Selenski on program participation and funding as of June 30, 2022; a report from program administrator Ascensus; an investment performance report by Meketa Investment Group; and presentation of both the Administrative Fund and Program Fund by audit partners.

At the meeting, the board approved a Notification of Proposed Emergency Regulation Action to readopt emergency regulations amendments that took effect March 18, 2022. The regulation amendments changed the date that newly mandated employers are required to register with the program, and simplified the employer registration process.

Also included on the agenda was a presentation by expert John Scott of the Pew Charitable Trusts’ Retirement Savings Project on private retirement plan market and impact of state retirement mandates, as the board seeks to further understand these topics to inform its operating strategy.

CalSavers is also in the news for its expanded employer coverage and employee access now extended to an estimated 750,000 additional workers (check out PLANSPONSOR’s recent article). In its latest report, CalSavers noted that by many measures strong growth remains consistent (for a great summary check out ASPPA’s recent post).

| |

|

Colorado (workforce 3.2 million) - The Colorado Secure Savings Program has officially launched a new program portal for employers and employees. It's a mini-site ahead of program rollout. Check it out!

The Treasurer's Office also announced BlackRock as intended global equity manager and State Street Global Advisors as manager of fixed income, money market and target-date fund investment options for the program. (subscription may be required to view the linked article).

| |

|

Illinois (workforce 6.2 million) - The Illinois Secure Choice Board met August 18, 2022. Key items on the agenda included introduction of new team members and highlights of the program’s quarterly report, including outreach, and marketing. Program administrator Ascensus reported recent service enhancements related to the program's expanded workforce coverage; 30-day contributions remained at peaks of ~$3.7M in Q2; assets and average account balances recovered significantly in Q3 due to improved market performance. The program has started its Wave 4 early notice campaign.

| |

|

Maine (workforce 677,000) – The Maine Retirement Savings Board met August 17, 2022. The agenda included an update from the Executive Director Search Subcommittee, and the Partnership Subcommittee. The latter discussed potential partnerships with other states and future collaboration with the Pew Charitable Trust on a feasibility study. A number of motions remain tabled while the program focuses on hiring its first Program Director.

| |

|

Maryland (workforce 3.1 million) – It's an exciting time at Maryland$aves as the program gets set for their statewide launch this month. The program is expanding its team with a new Finance Director position (position description here). The Board has also issued an RFP for External Auditing Services.

| |

|

Oregon (workforce 2.1 million) - The OregonSaves Board met August 30, 2022. Among other updates, Deputy Director David Bell commented on Wave 6; deadline shortly for these employers.

Also included in the meeting discussion was an update on the Oregon Bureau of Labor & Industries’ compliance timeline. Official meetings will start this month, and official notices to all non-compliant employers will start in June 2023, becoming an annual process starting July 31, 2024.

| |

|

Vermont (workforce 318,000) – Event alert! State Treasurer Beth Pearce will host a retirement security awareness roundtable discussion on September 9, 2022, at the Vermont College of Fine Arts with panelists Kathleen Kennedy Townsend, special representative to the U.S. Secretary of Labor, Rep. Tiff Bluemle and AARP State Director Greg Marchildon. The roundtable discussion will address systemic issues in retirement security, recent federal legislation, gaps in retirement security for women and trends in Vermont. Members of the public are invited to attend. For more information, email Ashlynn.Doyon@vermont.gov.

Vermont's planned program, the Green Mountain Secure Retirement Plan, is a voluntary state-wide multiple-employer retirement plan (MEP) intended to be launched soon.

| |

|

A C T I V E

Delaware (workforce 490,000) – Delawareans are in the news, as Governor John Carney signed the Delaware EARNS Act just before Labor Day, making Delaware the 16th state in the U.S. to create a state retirement savings program for private sector employees. For a great summary check out the PLANSPONSOR’s recent post here.

| |

|

C O M I N G U P

Join where you’d like, and count on us to follow these meetings for you:

-

Maryland (workforce 3.1 million) – The next meeting of the Maryland$aves Board is scheduled for September 12, 2022.

-

Oregon (workforce 2.1 million) – The next meeting of the OregonSaves Board is scheduled for November 15, 2022.

-

California (workforce 19.0 million) –The next meeting of the CalSavers Board is scheduled for November 21, 2022.

| |

May I Offer You a Precommitment? | |

|

In previous issues, I shared how we at Common Cents Lab work with industry partners. In those installments, I discussed how understanding user intentions and deploying thoughtful defaults can help users bridge the intention-action gap.

Today, we can explore a powerful tool for offering plan participation: precommitment. And we’ll learn how professionals in the retirement space can use this tool to guide users toward healthier financial lives over time.

| |

|

What is precommitment? In behavioral science, precommitment involves an individual committing in advance to a specific action at a specific time, trading away one’s future flexibility for an action that the present-self isn’t quite ready to perform but knows is beneficial.

Precommitment’s ability to reserve the hard stuff for the future makes plan participation more accessible today. Auto-Increase retirement savings provides that new participant with an implicit recommendation that increasing contributions over time is the right thing to do.

Through a recent series of studies related to Auto-Increases, researchers gave us even more insight into how to better implement precommitment to serve users.

Why does precommitment work? Precommitment works for a couple of reasons. First, precommitment leverages our bias toward the present by promising to reserve hard or unattractive actions. Second, offering users precommitments implicitly increases the perceived importance and urgency of an action.

Here’s what I mean and some thoughts on how you can use this perception to better guide users today toward healthier financial lives over time by creating formal structures based on user precommitments.

| |

Final tips:

For many people, saving for retirement is a challenging negotiation between our bias toward the present and our intellectual knowledge that we should be contributing toward our future needs. Professionals in the retirement space can help users overcome this challenge.

Stay tuned for more! / Perry

Perry Wright is a Senior Behavioral Researcher at Duke University's Common Cents Lab, using behavioral science to create solutions that aim to increase the financial well-being for low- to moderate-income people living in the United States and abroad. The Common Cents Lab is funded by the MetLife Foundation and supported by BlackRock as part of BlackRock's Emergency Savings Initiative. For more information and to connect directly, you can reach Perry by email here.

| |

|

Throwback Thursday? This just in from EBRI, and it feels surprising, and very 1980s. Is it true that women who are not married have lower retirement confidence than their married peers? EBRI cites a range of contributing factors: “First, they are much more likely to have lower incomes and asset holdings. They are also less likely to have done a retirement needs calculation or use a professional financial advisor. Unmarried retirees are also facing challenges in retirement. They are more likely to have low levels of savings, their expenses are higher than they expected when first retiring, and they are more likely to have retired earlier than planned.”

We would like to think that in the current decade, women have more flexibility, autonomy, and ability to focus on financial outcomes early in their careers, and that they have ready access to good financial education information along the way. The 2022 Retirement Confidence Survey sheds light on where this isn’t true. Thank you, author Craig Copeland.

While we were in the kiddie pool. Curious about the approaches in Canada, Lithuania, New Zealand and the UK? The GAO is. Why? They’re keeping an eye on outcomes for the nation’s aging workforce (in aggregate, not you, of course!). You can check out their full report here, with details on who counts as a covered employer and employee, the use of automatic enrollment, standard contribution rates, standard investments, and investment menus. Tranchau (Kris) T. Nguyen authored this report. Thank you to our friend John Mitchem for sharing this August 29 piece.

Our favorite August comment came from Aspen’s Karen Andres, who said, “retirement savings is a ledger for everything else going on in your financial life.” If the ledger = zero, not good. Emergency savings often comes higher on the list than retirement savings. Can ES be easier to achieve, more automated, and closer to the paycheck? In partnership with BlackRock’s Emergency Savings Initiatives, Commonwealth and DCIIA have identified some of the top Emergency Savings Features That Work for Employees Earning Low to Moderate Incomes. We won’t spoil it, a first-hand read is best.

Also, don’t miss the new episode of the State of Retirement – Shaping the Future podcast with the Georgetown Center for Retirement Initiatives. Bonnie-Jeanne MacDonald, Director of Financial Security Research at the National Institute on Aging at Ryerson University and Barbara Sanders, Associate Professor Statistics and Actuarial Science, Simon Fraser University introduce us to the concept of Dynamic Pension Pools and how they can address the need for lifetime pension income in Canada.

In the Ears: We’ve just finished the 24 hours, 53 minutes and 27 seconds of Robert Greenberg’s 30 Greatest Orchestral Works on Audible. Was it worth it? Yes it was. As Greenberg moves from Bach, Haydn, Mozart and Beethoven to masters who shared our lifetimes – Igor Stravinsky, Aaron Copland, Dmitri Shostakovich -- we could feel our brain, and our appreciation of these great composers and the worlds in which they labored, expanding. Greenberg is funny and keeps the stories rolling.

If you think that kept us from consuming much else, you would be right. Except we did quickly scarf down Wild Swan – Patti Callahan’s Florence Nightingale novella. It’s a quick snack, well narrated, dramatic.

Palate cleanser – we’ll stick with the arts – any painting that starts out all pink is good by us. Thank you @not_sorry_art!

| |

... With that lead-in, it's time for some PIX! | |

What if taking up a new sport brought you to this place … | |

|

This is Ice House Reservoir, thanks to Katie Selenski, on a calm day not long ago. #welike

This looks like great fun too – keepin’ it cool on the Sacramento River. That’s “Hello,” not “Help,” we’re pretty sure.

| |

When you get off the river, if it’s your lucky day you might get to join the CalSavers team at the ballpark – featuring, naturally, the River Cats. | |

That is one great looking group. Enjoy the game, Gang. You’ve earned it! | |

|

That’s it for this edition. ❤️ Hug your people and change the world.

If you like this piece, please stick with us. We’ll be back in about two weeks. If you don’t like it, please unsubscribe below. Comments for us? Please let us know. Want your own subscription? Request one here. All information shared is from public sources or used with express permission.

| |

Massena Associates provides process, policy, and implementation consulting on retirement savings programs and products.

Our clientele includes public entities, policy organizations, and private sector providers. Our specialty – efficient, targeted results. We are an active speaker on retirement security topics, including state-facilitated programs, MEPs and more.

If you’d like to explore working together, we welcome the conversation. Connect with us here, and at 339-236-0684.

| |

|

Looking for a great retirement savings innovation resource? Led by Dr. Alicia Munnell, the Center for Retirement Research at Boston College develops and hosts terrific content and proprietary research related to states, financial security, social security, and more.

The Georgetown Center for Retirement Initiatives, Exec Angela Antonelli, provides excellent information on state-based and other retirement security innovation and policy.

Pew’s Retirement Savings Project studies the challenges and opportunities for increasing retirement savings and is another great resource - check out the work of John Scott and his terrific team.

If you want a great source of broad-based, consumer-focused retirement news, Jeffrey H. Snyder’s The Morning Pulse is your ticket. You can subscribe here.

| | | | | |