|

“Given the last decade of zero rate policy and subsequent severe capital losses over the past three years, passive index returns over the trailing five years are flat and negative when factoring in fees. In the same way trees don’t grow to the sky, bond investors faced the reality that interest rates don’t fall forever.

That said, the sell-off in fixed income has created opportunities for investors willing to reengage with the asset class. Indeed, our 2024 Long-Term Capital Market Assumptions (LTCMA), which provide 10-15 year return projections for major investable asset classes, expect the U.S. Agg. to deliver 5.1% annualized total return over this time horizon.

We have always believed core bonds play a key role in investor portfolios; however, investors should be reminded that this is not your grandfather’s bond market. Our research has identified key reasons to embrace an active approach within fixed income going forward to enhance returns and generate alpha over the next cycle:

- The U.S. Agg. is not as diversified as it once was given the index rewards the most indebted borrowers by weighting the index based on how much debt an issuer has outstanding. The explosive growth in U.S. Treasury and IG corporate debt has increased their share of the U.S. Agg. at the expense of agency mortgage-backed securities (MBS). Thus, the credit and duration characteristics are quite different and can impact returns.

- The benchmark captures just 52% of the U.S. public bond market meaning investors don’t have access to a large swath of investable securities like asset-backed securities and other agency debt.

- BBB-rated corporate credit represents 42% of the U.S. Agg’s corporate credit allocation due to lower-quality borrowing trends.

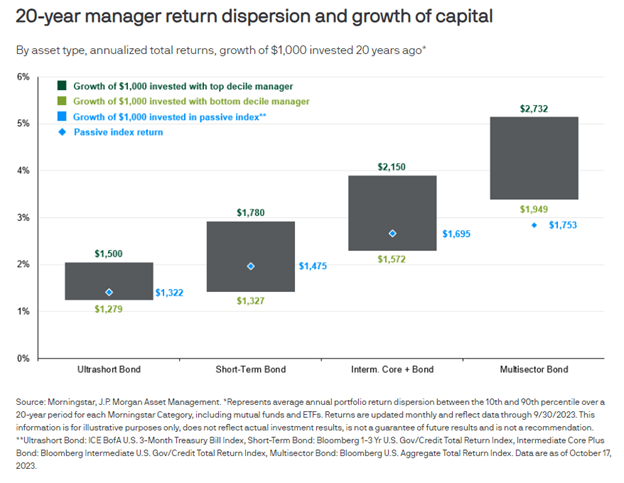

Per the chart, it’s striking to see that over the past 20 years, even the bottom decile active managers have outperformed the passive U.S. Agg. index as indicated by the Morningstar multisector bond category, with top active managers generating considerable alpha for clients. Given the shifting characteristics in the bond market and uncertainty around the path of rates from here, investors should engage in an active approach with proven managers in their fixed income allocations.”

|