|

RBG Wealth Weekly

December 8, 2023

| | |

|

Ladies and gentlemen, the weekend! In this space each week, Greg and I share some of our favorite articles, notes, and graphics from the past week along with our commentary. Please feel free to provide feedback and forward along to others if you enjoy. We appreciate you taking the time to read.

If you are a client, we truly appreciate your business. If you are not a client, please click below to learn more about our firm and contact us.

| | |

|

“It’s that time of year when Wall Street’s top strategists tell clients where they see the stock market heading in the year ahead. Typically, the average forecast for the group predicts the S&P 500 climbing by about 10%, which is in line with historical averages.

This year, strategists are offering a pretty wide range of views. Some see weakness. Some see strength. The targets range from 4,200 to 5,500. This implies returns between -8.5% and +19.7% from Friday’s close. For what it’s worth, the forecasts aren’t as skewed to the downside as they were last year.

Before we move on, I’d caution against putting too much weight into one-year targets. It’s extremely difficult to predict short-term moves in the market with any accuracy. Few on Wall Street have ever been able to do this successfully. I do however think the research, analysis, and commentary behind these forecasts can be informative.

That said, here’s what’s driving Wall Street’s views for 2024:

The economists that these stock market forecasters work with are split on whether the U.S. economy will go into recession some time during the year, which has implications for revenue among other things. Those who are expecting continued expansion expect growth to be modest, and those looking for a recession expect any downturn to be brief and shallow. (Scroll down for: Wall Street’s 2024 U.S. economic outlook 🇺🇸)

Interestingly, most strategists still expect S&P 500 earnings to grow in 2024 despite lackluster GDP growth forecasts. This may have to do with the expectation that consumer spending shifts back toward goods from services and the fact that the S&P has greater exposure to the goods sector, whereas U.S. GDP has greater exposure to the services sector.”

|  | | |

|

Tis the season for market outlooks. Sam had a good disclosure in his article. Short-term (i.e., 1-year forecasts) are mostly wrong, but there is always some quality research, analysis, and commentaries within.

Over the next few weeks, we will highlight some recaps and outlooks that we find valuable and have interesting insights.

| | |

|

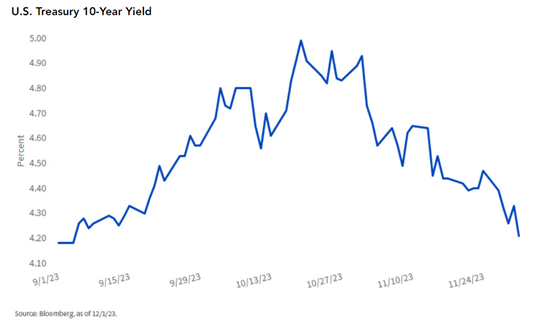

“Without a doubt, one of the more noteworthy developments in the financial markets of late has been the plunge in U.S. Treasury (UST) yields. Only a month or so ago, investors were looking at 5% yield levels, or close to it, along most of the UST maturity spectrum. In fact, some prognosticators were even mentioning that a 6% UST 10-Year yield shouldn’t be ruled out. So, the natural question to ask is: what happened in such a short period of time?

| | |

|

Let’s go to the videotape for some perspective. As the graph highlights, the UST 10-Year yield has now essentially reversed the entire increase it experienced in September and October. Just what did that entail, exactly? A move of roughly [0.80%], first to the upside, and now to the downside… Well, it doesn’t get more volatile than that in bond-land.

Typically, a reversal in yields of the magnitude we are discussing, especially in such a relatively short period, would require a sea-change in some key ingredient such as the economy, inflation and/or monetary policy. While the pace of economic growth does appear to be slowing from Q3’s robust reading of 5.2%. Based on the St. Louis Fed GDP Nowcast estimate, it looks like real GDP for Q4 could still be coming in just under 2%, or not too far removed from the first six months of 2023. With respect to inflation, progress continues on this front as well, but the most recent annualized reading on the Fed’s preferred inflation gauge, the core PCE Price Index, came in at 3.5%, or still visibly above the policy maker’s 2% target.

So, that leaves us with the monetary policy quotient and, no doubt, this is where the outlook has shifted dramatically. The money and bond markets have now moved up the timeframe for the first Fed rate cut and increased the cumulative amount of expected decreases for the Fed Funds trading range for 2024.”

The benchmark 10-year U.S. Treasury rate has made a roundtrip from 4.0-4.2% levels in August to 5% in mid-October and back to 4.2% currently. That’s a quick move for interest rates without a needle-moving economic event.

The conclusion reached is the fixed income market is pricing in Fed rate cuts in 2024, and quickly. To support rates back at this lower level as well as Fed cuts, over the next 3 months, we will likely need to see the core inflation rate with a 2% handle (3.5% currently) and the unemployment rate with a 4% handle (3.7% currently).

| | |

|

“As of Oct. 1, the Internal Revenue Service is charging 8% interest on estimated tax underpayments, up from 3% two years ago. The increase is one of the many effects of rising interest rates…

The IRS assessed more than $1.8 billion in penalties for underpaying estimated taxes on nearly 12.2 million individual returns in fiscal year 2022…

To avoid underpayment penalties, most filers must pay 90% of their taxes through withholding during the calendar year, or through estimated payments due quarterly. The payment for the fourth quarter of 2023 comes due Jan. 16, 2024. The IRS won’t charge an underpayment penalty if the balance due is less than $1,000 after taking into account withholding and credits. (Though it is called a penalty, it is essentially interest tied to the federal short-term rate.)

Staying on top of estimates is especially important for people with fluctuating or self-employment income. Taxpayers with bonuses and equity compensation, whereby automatic tax withholding is too low, could face underpayment penalties. Anyone with higher-than-usual interest from high-yield savings accounts and mutual-fund dividend or capital-gain distribution payouts could also be affected…

Individual taxpayers can generally insulate themselves from underpayment penalties by paying in (through withholding or estimated taxes) at least 90% of the current-year tax bill or 100% of the previous year’s tax bill. The 100% figure rises to 110% for filers with adjusted gross income of more than $150,000, or $75,000 for married taxpayers filing separately.”

This is another one of these higher interest rate chain reaction items that taxpayers may not have considered. The standard interest rate on underpayment of taxes is 3% plus the federal short-term rate, which resets quarterly.

For 2022, those rates were lower but rising (3% for Q1, 4% for Q2, 5% for Q3, and 6% for Q4).

For 2023, those rates are much higher (7% for Q1, Q2, Q3, and now 8% for Q4).

| | |

|

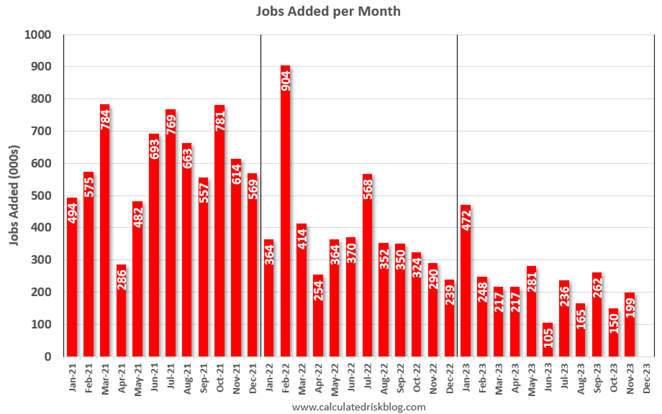

“Through November 2023, the employment report indicated positive job growth for 35 consecutive months, putting the current streak in 5th place of the longest job streaks in US history (since 1939).

[Today’s release of the November] jobs number was at consensus expectations; however, employment for the previous two months was revised down by 35,000, combined. The participation rate and the employment population ratio both increased, and the unemployment rate decreased to 3.7%.

Another solid employment report.”

| | |

Tweet (or maybe X) of the Week | |

Thanks for reading. Have a great weekend! | | | |

Guidance for today. Growth for tomorrow. |

|

|

Tim Ellis, CPA/PFS, CFP®

CIO and Wealth Advisor

RBG Wealth Advisors

| | |

RBG Wealth Advisors LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance. | | | | | |