|

July 25, 2024

When was the modern city of New York born? Some might say that it was in the 1820s, when the Erie Canal was completed, connecting the port city to the Great Lakes and transforming it into the commercial center of the nation. Others might say that it was in the 1900s, when the subway system opened, forever altering the way that New Yorkers would move throughout the city. Still others would point to its cultural milestones—from the emergence of Broadway to the opening of Lincoln Center. In many ways, the story of New York is the story of these accumulating accomplishments—of the layers of transportation, commerce, and culture that came together to create something greater than the sum of its parts: the diverse tapestry of the city that never sleeps.

Yet underneath it all is a foundation that made these gradual developments possible—a base upon which such a city could be built. For New York, we need to go back 240 years to reach this bedrock. At the time, the city was still recovering from the Revolutionary War, and stable ground was direly needed to help the city overcome the devastation of war, fire, and disease. It was this necessity that drew a small number of professionals to a coffee house in Lower Manhattan to discuss how they might help New York not only recover, but become an even greater city than before. These congregants, which included Alexander Hamilton, saw all that New York might become—but they understood that for this potential to be actualized, they needed the financial means to translate ideas into reality. They resolved to establish Bank of New York (now BNY), and in doing so, took the first steps towards realizing the city that we know today.

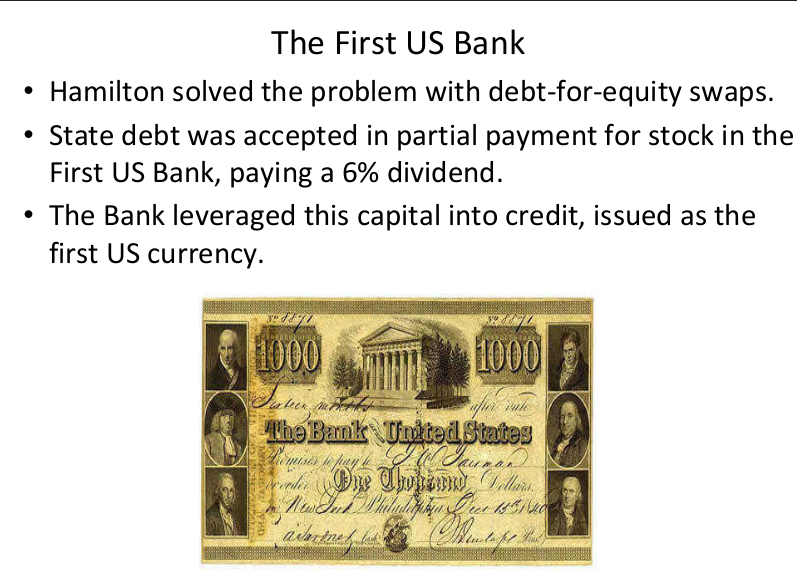

The constitution of BNY, penned by Hamilton himself, codified the sensibility that would allow the institution to serve as a pillar for centuries to come. Under its supervision, dividends would be reliably paid, overdrafts would be forbidden, and the books would remain balanced. Hamilton understood that when it came to restoring a city, you needed trustworthy foundations to build on, and so he wove resilience into the culture of BNY from the start. This insight would serve him well years later when he became the nation’s first Secretary of the Treasury and inherited an economy on the brink of collapse. BNY—which had by then helped New York get back on its feet—would again serve as the basis for development by loaning the young government $200,000 to keep the lights on while Hamilton stabilized the nation’s finances. (It’s a relationship that continues even to this day for BNY, as the primary provider of clearance and settlement for U.S. government securities).

|