Market Update - June 2022 | |

Image: Expect big market waves up and down in the coming months. | |

- All markets rose in May, except for the Nasdaq and precious metals markets.

- Interest rates peaked in early May and an inflation reading of core inflation from April was encouraging.

- The U.S. economy is expected to grow about 2% this quarter, pushing recession forecasts to later this year.

- The Federal Reserve will raise rates to 1.75% by the end of July. With headline inflation of 8.5%, the Federal Reserve is dragging its feet to slow inflation.

| |

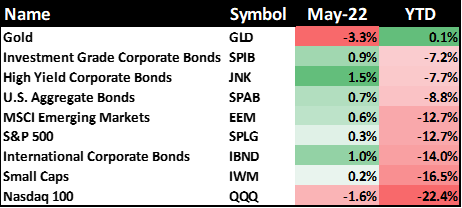

Table 1: Performance update | |

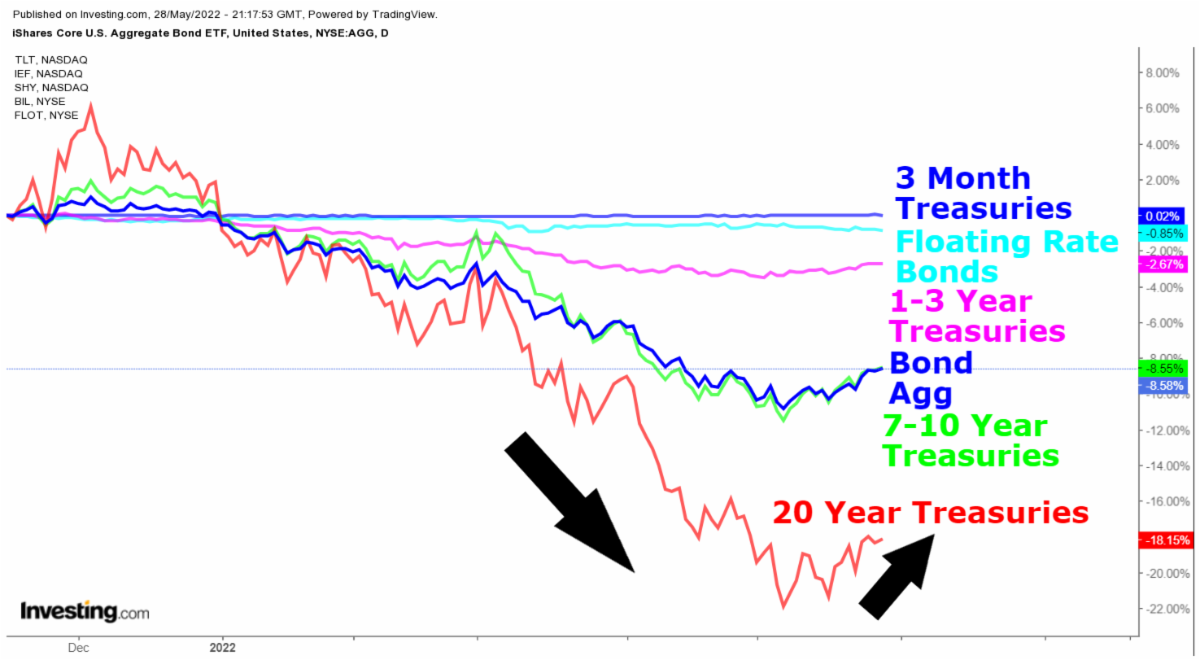

Bond and equity markets put in a temporary bottom in May. In general, the riskiest segments of the market such as the tech-heavy Nasdaq and Small Caps have performed worst of all year-to-date. Ironically, they have rebounded the most off of the bottom May 23rd (the May performance numbers don't tell the whole story.) Investment grade and municipal bonds bonds also performed well. Remember, for bonds "price-up" = "yield-down" and lower interest rates mean financial stress is declining. | |

The market bounce that began May 23rd was a relief to many investors. In particular, there were four key factors that set the stage for a bottom and subsequent rally: 1) extremely negative sentiment, 2) a peak in a key inflation data and interest rates, 3) a prediction of slow interest rate increases from the Federal Reserve, and 4) good forecasts for 2nd quarter GDP growth.

First, if you read a lot of market news and watch a lot of financial television like we do, you may have noticed a distinct negative tone over the last few weeks. How could the market keep falling? Why aren't our optimistic forecasts coming true? Why are we losing money? The feeling of depression was quite palpable. This narrative is merely articulating the feelings of the market participants. There is a psychological aspect to investing I mentioned two months ago when I asked if you were mentally prepared for a bear market (Mental preparation for a bear market). Clearly, many of the talking heads on CNBC and Bloomberg were not prepared. However, it is precisely this negative attitude that creates investing opportunities for the attentive investors.

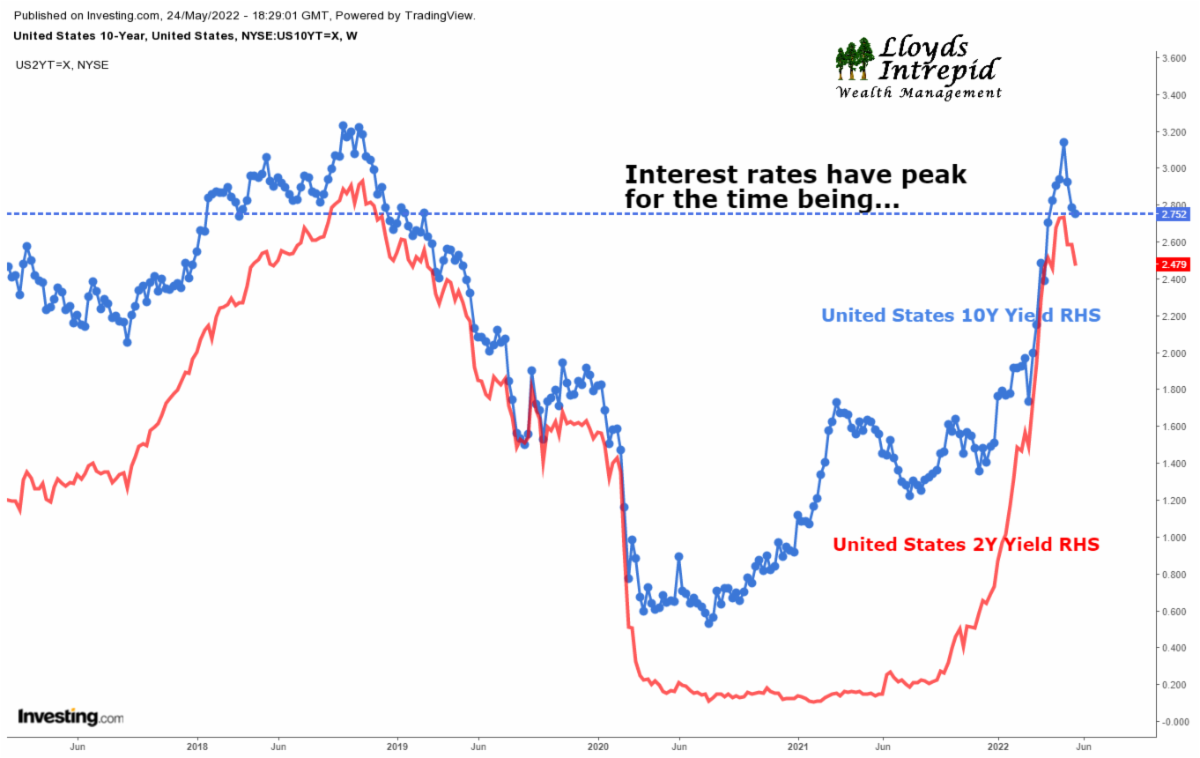

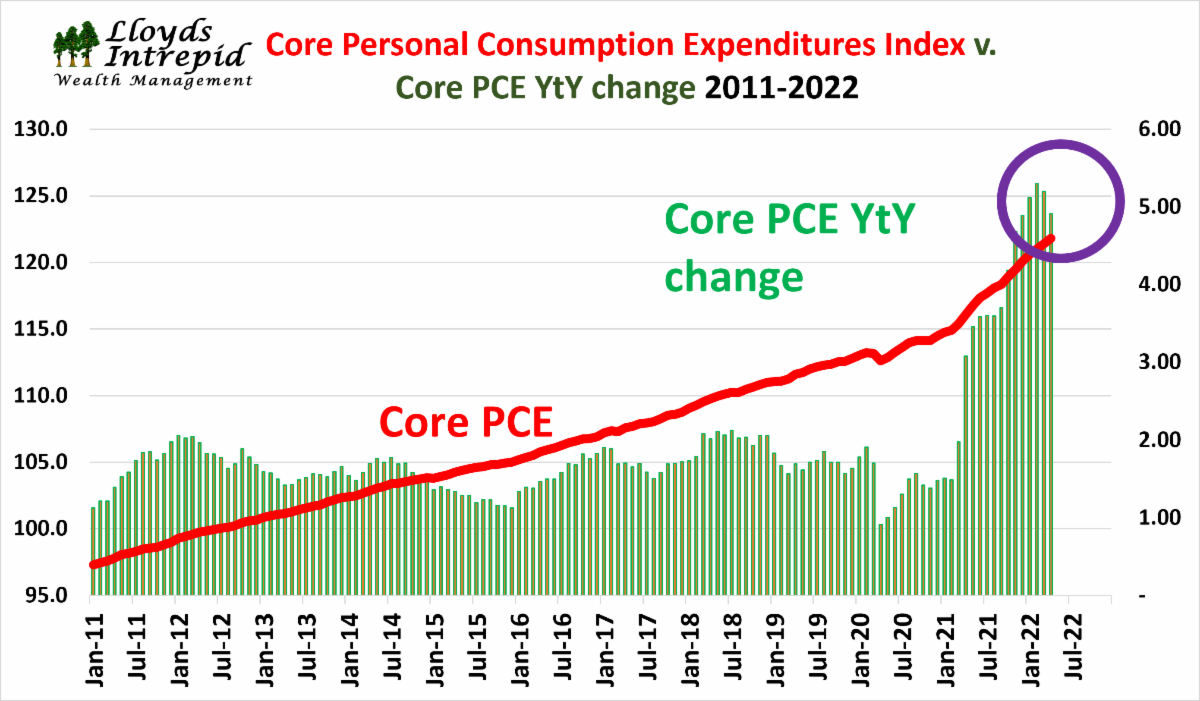

Second, it looks like interest rates have peaked for now. While we don't have to perfectly explain why, declining interest rates take some pressure off of the economy and imply that maybe inflation has peaked. Additionally, Core Personal Consumption Expenditures (Core PCE), a key inflation indicator followed by the Fed, may have also peaked. These are encouraging signs on inflation and interest rates, but it is too early to tell if this is "the" peak for this cycle. Total inflation remains much higher.

| Figure 1: Key interest rates: US 10-year yield and US 2-year yield | |

Figure 2: Core PCE inflation, a key Fed metric, has recently peaked | |

Third, the Federal Reserve remains committed to raising rates by only 50 bps in the June and July meetings despite the economy experiencing 8% inflation. They are still taking minimal steps to slow down the economy and its corresponding inflation. The market is taking this as a bullish signal for now.

Finally, there are indications that first quarter GDP of -1.5% was not the beginning of a recession. So far, the data on second quarter GDP growth is OK as we can see with the Atlanta Fed's GDPNow estimate of +2% growth.

Each one of these are reasons to temporarily lean against the bearish mood of the day.

| Figure 3: Atlanta Federal Reserve's GDPNow estimate for 2nd quarter GDP | |

While the news behind the recent market rally is fresh and encouraging, there are several severe problems afflicting the economy.

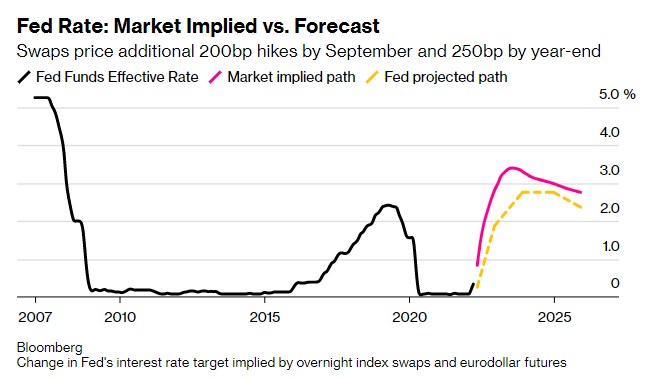

First, even though we have signs that inflation may have peaked, the Federal Reserve is mounting some response to it. Essentially, they have committed to raising rates to 2.5-3.0% before assessing whether they are affecting inflation. Of course, if we enter recession and inflation collapses, they won't have to raise rates dramatically, but that is not the market's base case at this time. Here is a reminder of what the bond market thinks interest rates will do over the next few years.

| |

Figure 4: Implied path of short-term interest rates | |

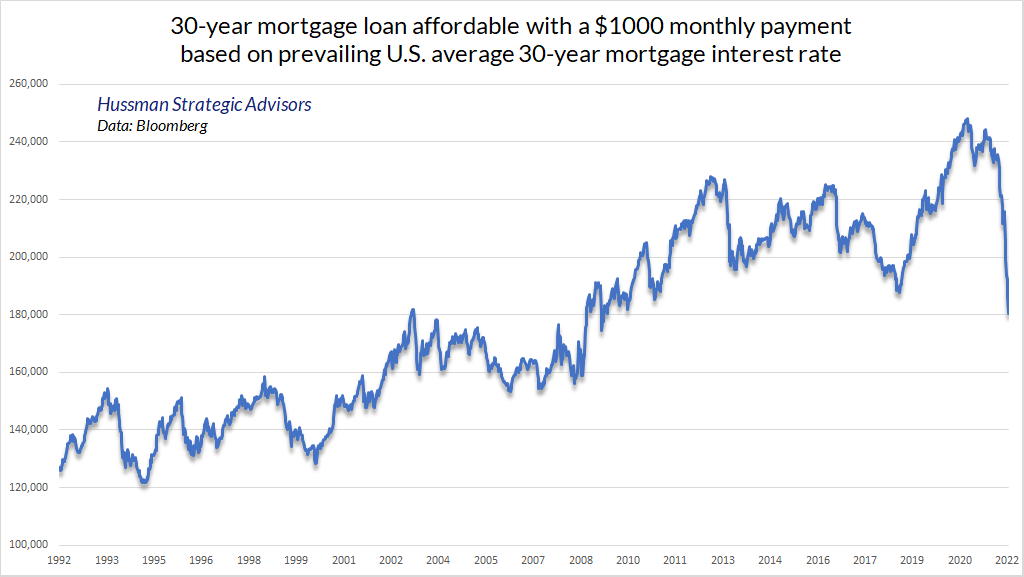

Additionally, higher interest rates have a detrimental effect on the pricing of stocks, bonds and real assets like houses. Here is an interesting analysis from John Hussman that compares how much house a $1,000/month payment can buy with a 30-year fixed rate mortgage. You can see how the recent move in interest rates has dramatically affected the housing market and we are only just now beginning to see the consequences. | |

Figure 5: Federal funds rates follow the US 2-year bond regularly | |

Second, corporate earnings are falling as inflation eats into margins. At first, inflation allowed companies to raise prices and increase profits, but now the cost of raw materials, inventory, labor and interest expense is chipping away at that expanded profit margin. We can see it both on a national level in Figure 6 and at the individual company level in Figure 7. While not clear signs of recession, they are very serious signs that the economy is slowing significantly. | |

Figure 6: GDP Growth vs. Corporate Profits through March 2022 | |

Figure 7: Big companies with spectacular earnings misses | |

Finally, if we look to the 1970s, we can see another period when a supply squeeze created very high inflation, the Fed raised rates in response, and the economy fell into a painful recession. The 1973 recession was affected by the OPEC oil embargo, but the underlying inflation had been building for years. What is most interesting on this chart is that the 10-year Treasury yields did not fall much during the recession but kept marching higher as the underlying inflation was not eliminated. This will be something to track closely in 2022 and 2023. If long term Treasury yields do not fall as the economy decelerates, expect inflation and rates to resume their rise after 2025. | |

Figure 8: S&P 500 and 10-year Treasury yields in the 1970s | |

Inflation is worse than you think it is | |

|

Everybody is worried about inflation. Earlier this month, we received the latest inflation numbers for April 2022. Many analysts hope this data indicates a peak in inflation as discussed above, but the drivers of inflation are more than just supply chain disruptions.

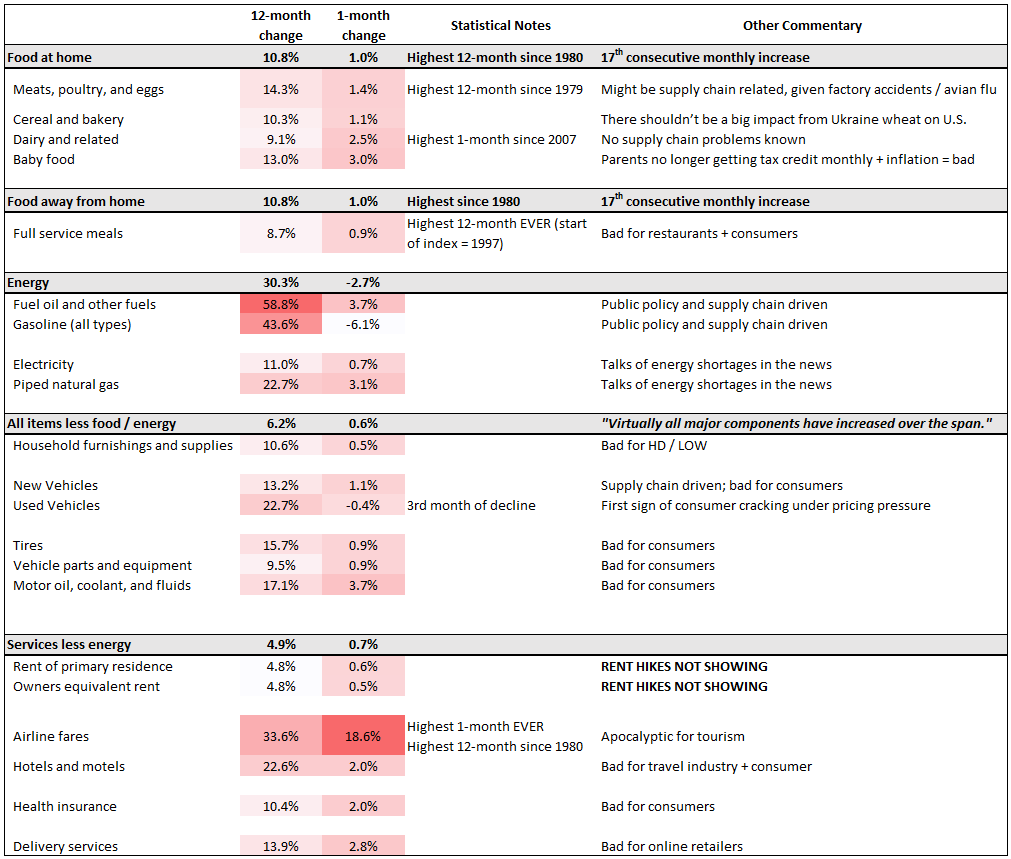

Gasoline prices rose dramatically over the past year, yet the headlines surrounding the Russian invasion of Ukraine have dominated the news hiding other significant inflation data reports. Food and home prices have risen substantially, reflecting 1) higher transportation costs, 2) higher fertilizer costs, 3) avian flu, and 4) higher wages. The price index for "Meat, poultry, and eggs" had the largest 1-year increase since 1979, while "Dairy and related" index had its highest 1 month increase since 2007. Food price hikes affect everyone and the average consumer will always allocate money towards food over other less critical choices.

Beyond food, the chart below attempts to pull together the key unavoidable expenses every consumer in the country faces. For example, maintenance expense for cars is at least 9.5% higher, health insurance is up 10.4%, and used car prices are up 22.7% compared to last year. Extreme inflation for the basic necessities may cause consumers to restrict spending on other items like cell phones, vacations, cars, restaurants or entertainment. This is what typically happens during recessions when people lose their jobs, but in this case their earnings can't keep up with the price increases.

Chris wrote an extensive note on inflation if you want to read more. It is here.

| Table 1: Inflation rates on various basic necessities April 2022 | |

|

The bond and stock markets have put in a short-term bottom in May, in our view. It is not clear if this is "the" bottom, but the classic signs of a bear market bottom have not occurred: 1) recession, 2) Fed cutting rates, 3) stimulus spending, 4) peak in unemployment, and 5) panic selling in the markets.

We know that bear market rallies are common and can be large. For example, here is a chart of the 2000-2003 bear market. There are some similarities to our current market with the 2000 bear market: 1) extremely overvalued stocks in the technology sector, 2) a very tight labor market, 3) a Fed tightening cycle, and 4) an inversion of the yield curve. This is not meant to be a map for our current market's travels, but a way to think about how large rallies are part of a normal bear market.

| Figure 9: The S&P 500 bear market of 2000-2003 (yes, it was a long one) | |

Figure 10: The current S&P 500 market 2020-2022 | |

Figure 11: The bond markets have also put in a bottom for now | |

|

We have made some dramatic changes to our portfolios in May. We have rotated out of our 3-month Treasury and Floating Rate bond positions and bought exposure in longer duration Treasury, municipal and corporate bonds. At the same time, we have reduced out equity underweight and increased exposure to the S&P 500. Our view is that this is a bear market rally that will last 4-12 weeks.

In summary, geopolitical tensions remain high, the global economy is slowing sharply, valuations are high, interest rates may have peaked, and global financial system stress is easing somewhat. We expect the markets to rally in the coming weeks but do not believe this is the start of a new bull market. Expect big waves up and down in the markets over the next few months.

If you have any questions, please call me at 281-402-8284.

Sincerely,

Rob and Chris

| |

|

Robert J Lloyd, CFA®

President and Chief Investment Officer

Lloyds Intrepid Wealth Management

1330 Lake Robbins Dr., Suite 560

The Woodlands, TX 77380

281-402-8284

Robert.Lloyd@lloydsintrepid.com

www.lloydsintrepid.com

| |

Lloyds Intrepid LLC (“LIWM”) is an Investment Advisor registered with the State of Texas, where it is doing business as Lloyds Intrepid Wealth Management. All views, expressions, and opinions included in this communication are subject to change. This communication is not intended as an offer or solicitation to buy, hold or sell any financial instrument or investment advisory services. Any information provided has been obtained from sources considered reliable, but we do not guarantee the accuracy, or the completeness of, any description of securities, markets or developments mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this communication's conclusions. Please contact us at 281.886.3039 if there is any change in your financial situation, needs, goals or objectives, or if you wish to initiate any restrictions on the management of the account or modify existing restrictions. Additionally, we recommend you compare any account reports from LIWM with the account statements from your Custodian. Please notify us if you do not receive statements from your Custodian on at least a quarterly basis. Our current disclosure brochure, Form ADV Part 2, is available for your review upon request, and on our website, www.LloydsIntrepid.com. This disclosure brochure, or a summary of material changes made, is also provided to our clients on an annual basis.

| | | | |