IBANYS Weekly E-Newsletter | |

|

Hope everyone had a nice long weekend.

BANK OF ROCHESTER: Over the past few weeks, we have taken a very proactive approach to opposing the bill on creating a public/ municipal bank called Bank of Rochester. In lockstep with the local community banks, Rochester Chamber of Commerce and NYBA, we strongly opposed the bill and provided alternative solutions that meet the issues. Creating a public bank for local projects is no small task for the city and/or state. Many existing programs will be better served to handle the projects for the city of Rochester, i.e., Pursuit, Capital Access Program, creation of MDI's, CDFI's, etc. We will stay on top of this for the last few weeks of session and provide updates.

The FDIC Quarterly report is included in Washington section below. Please review for the latest data on community banks performance.

IBANYS ANNUAL CONVENTION: Celebrating 50 years supporting community banks!!

Come join us at The Turning Stone Resort and Casino from July 15-17 to celebrate a milestone for our Association and all the great community bank leaders of the past half century!

There are still a few exhibit booths left, the opportunity to sponsor and donate an item for the PAC Auction.

Bring your executive team, senior leadership and board of directors to celebrate. The link to register for the convention is below. Also, please call The Turning Stone Resort and Casino to book your hotel rooms. The cut off date is coming quickly.

Look forward to seeing everyone help us celebrate IBANYS 50 YEAR ANNIVERSARY!

John

| |

|

Sponsors to date

- BHG Financial

- COCC

- Federal Home Loan Bank of NY

- Gensis PPG

- Hartman Executive Advisors

- Heilbronner Consulting

- ICBA

- InfoAgora

- NBS Group

- NEACH

- Plante Moran

- Piper Sandler

- Roosevelt & Cross

- Shield Compliance

- Sunweath

- The Long Group

- The Bonadio Group

- Wolf & Company

| Click the link above to obtain the detailed convention meeting brochure which includes the meeting agenda, registration information, booth information (only 3 left) reserve your booth today!! Sponsorship opportunities, golf details and much more. We are looking forward to you joining us in July at the Turning Stone Resort & Casino to help IBANYS celebrate our 50th Anniversary!! | |

- Booth 1 – Pioneer 360

- Booth 2 – BHG Financial

- Booth 3 – DataSure 24

- Booth 4 – NES Group

- Booth 5 – Shield Compliance

- Booth 6 – La Macchia Group

- Booth 7 - ICBA

- Booth 8 – Lee & Mason

- Booth 9 – Strategic Resource Management (SRM)

- Booth 10- - Hartman Executive Advisors

- Booth 14 – Specialized Data Solutions

- Booth 15 – Genesis PPG

- Booth 16 – Acture Solutions

- Booth 17 – Dox Electronics, Inc.

- Booth 18 – Neach

- Booth 19 – Office of the Comptroller of the Currency

- Booth 20 – Ncontracts

- Booth 21 – Magee Company

- Booth 22 – PW Campbell

- Booth 23 – JMFA (Atvantage)

- Booth 24 - RelPro

- Booth 25 – Federal Home Loan Bank of NY

- Booth 26 – IntraFi

- Booth 27 – StrategyCorps

- Booth 28 – Wolf & Company

- Booth 29 – InfoAgora

- Booth 30 – The Long Group

| |

Meet the Convention Speakers | |

| |

Charles E. Potts

EVP & Chief Innovation Officer

Independent Community Bankers of America® (ICBA).

In this role Potts drives ICBA’s innovation initiatives, and financial technology strategies, working with ICBA leadership to develop impactful, value-added solutions that help community banks seize new market opportunities to meet customers’ evolving financial services’ needs.

Potts’ extensive experience in banking and financial service firms provided the background Potts needed to start, co-found or lead various fintech start-ups including digital banking, mobile engagement, financial management and payments providers. Many had successful exits via IPO’s or acquisition via strategic acquirers.

A frequent speaker at national trade shows and conferences, Potts previously served as executive managing director at First Performance Global, where he led international business and corporate development activities for its card-control and fraud alert platform. Before that he served as CEO for NetClarity, a start-up in the University of Florida’s Business Incubation Hub. Prior to ICBA, he worked at the Advanced Technology Development Center (ATDC), leading the fintech practice where he mentored startups as part of the Georgia Tech-based incubator.

Charles attended the Georgia Institute of Technology, did his graduate studies at Georgia State University in Atlanta and attended the Graduate School of Banking at LSU. Potts, an avid masters runner, cyclist and soccer fan, lives with his wife in Atlanta, GA. They have a daughter who recently graduated from the University of North Carolina at Chapel Hill where she was a nationally ranked pole vaulter on the Track and Field team.

| |

| |

Kim Snyder, CPA

CEO & Founder

KlarivVis

Kim founded KlariVis in February 2019 to solve the data conundrum in the financial institution industry. Kim is also the CEO and founder of KBS Results, a highly specialized consulting firm, assisting financial institution clients with engagements including: strategic planning, merger & acquisition planning and integration, operational excellence, financial management, succession planning and incentive plan development. Her experience as CFO / EVP of a $900MM publicly traded bank fueled her desire to create a leading-edge, easy to use, transformational data analytics solution to enable community banks and credit unions to directly compete with the large mega-banks.

Kim is a Virginia Bankers Association Bank Management School faculty member and serves as the CFO Facilitator for the Tennessee Bankers Association CFO Forum. Kim earned the banking graduate degree and leadership certificate from the ABA Stonier Graduate School of Banking and also served on the ABA Stonier Graduate School of Banking Board of Directors. Kim is a magna cum laude graduate of James Madison University.

| |

| |

Wade Barnes

Industry Lead, Financial Services

Hartman Executive Advisors

Wade is an indispensable asset to his clients who benefit from his extensive experience working in the banking industry and expertise in using technology to solve issues ranging from operational inefficiencies and regulatory challenges, to cyberthreats. As Hartman’s Financial Services Industry Lead, he works alongside executives to create and execute technology roadmaps and data strategies to drive growth and innovation. Wade is a highly effective, multi-disciplined leader who thrives on identifying opportunities and creating strategies for businesses to build market share and increase overall profitability.

Wade has spent most of his career in banking, starting as a teller and advancing through the ranks to the C-suite. Before Hartman, Wade was the Chief Marketing Officer at Howard Bank. In this role, he championed the importance of using technology to source new clients and expand relationships with existing clients by defining the customer journey and personalizing the banking experience. He also created and led a corporate discipline for product development, including a FinTech initiative, with a focus on processes for highly efficient internal operations and enhancements to the customer experience. Wade also held senior management roles in retail banking, marketing and e-commerce at 1st Mariner Bank, where he leveraged technology to automate business processes and used data analytics to drive strategy and execution.

Wade most enjoys spending time at home with his wife and daughter, especially when he has time to try out a new recipe for dinner. You might also find him on the golf course or making plans for his next European vacation. Wade also passionately serves on the board of directors for Meals on Wheels of Central Maryland and Maryland Council on Economic Education.

| |

| |

Hamza Qadir

Director of Strategic Innovations and Operations

1st National Bank of Scotia

Hamza Qadir is an entrepreneur at heart, long time innovation-enthusiast, and currently the Director of Strategic Innovation and Operations at 1st National Bank of Scotia. He joined 1st National Bank of Scotia in June of 2023, where his journey to help foster the bank's innovation mindset and overall culture began. Hamza is a firm believer that in order to be truly successful at innovation, it must be a dedicated part of the organization's strategic goals and tactical operations. Innovation is a valuable skillset that can be learned and powerfully leveraged when an organization is ready for change!

In his prior innovation roles, Hamza served as a digital transformation agent for some of the largest enterprises in the world including FIS, Blue Cross Blue Shield, and Walmart. From an entrepreneurial perspective, Hamza has not only served as a startup founder and small business owner himself, but has helped countless other entrepreneurs create, build, and scale their dreams. His ability to draw from a diverse range of experiences offers a new perspective to help tackle the problems facing the community banking industry. Having moved from Little Rock, Arkansas to the Capital Region in New York, he is a proud New York Banker and eager to play a role in helping to evolve the community banking landscape.

| |

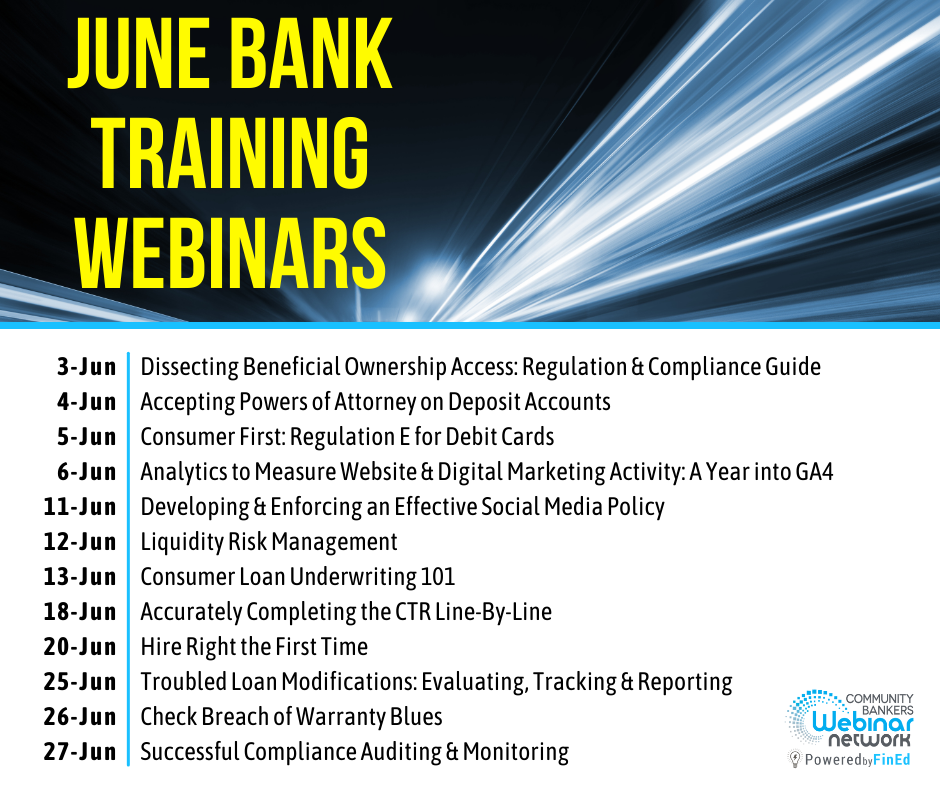

JUNE WEBINARS Power by FinEd | |

ASSOCIATE & PREFERRED PARTNERS | |

|

Aug 14-15, 2024 Virtual/Live Training

HR Management 2024

| |

Instructor, Kerry Sauley, is the Marjorie B. Ourso Excellence in Teaching Professor at Rucks Department of Management, Louisiana State University, Baton Rouge, LA. | |

This workshop is designed to provide intensive training for employees in Human Resources Management. | |

|

TOPICS INCLUDE

- Employee Recruitment, Selection, and Placement

- Situational and Behavioral Interviewing

- Driving Employee Engagement

- Creating an Accountability Culture

| |

|

AUDIENCE

- Human Resource Managers

- Branch Managers

- Department/Division Managers

- Management/Hiring/Coaching/

Counseling Responsibilities

| |

|

PRICE:

In Person: $695

VIRTUAL (VIA ZOOM): $595

| |

|

Registration is now open for Stifel’s Virtual Bond School, where our product specialists will review all of the investment products that comprise a robust portfolio. In addition to bond basics, they will explore how to incorporate these products into an investment strategy that meets an institution’s goals and objectives.

As part of Stifel Fixed Income’s value-added suite of services, the courses are at no cost and continued professional education (CPE) credits are available. For your reference, the agenda is listed below. If you have any questions or would like additional information, please contact your Stifel representative or email FixedIncomeEvents@stifel.com.

| |

| Thursday, June 13 |

| | 1:00 - 2:15 p.m. ET

2:15 - 2:30 p.m.

2:30 - 3:30 p.m.

3:30 - 3:45 p.m. | Corporates, RMBS, CMBS and ABS (1.5 credits)

Break

Portfolio Construction (1 credit)

Closing

| | |

|

Field of Study: Finance

As part of Stifel Fixed Income’s ongoing commitment to Continuing Professional Education (CPE), all attendees can earn CPE credit(s) for participating in these group internet-based sessions, which require no prerequisites or advanced preparation. Please note that each attendee must be registered individually, log in with their user-specific registration, and be logged on for a minimum period of time in each session to receive CPE credit.

Stifel Fixed Income is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.nasbaregistry.org

| |

This is for institutional use only. Stifel, Nicolaus & Company, Incorporated, is a broker-dealer registered with the United States Securities and Exchange Commission and a member of FINRA, NYSE and SIPC. This information has been prepared for general information purposes only and does not consider investment objectives, financial situation or particular needs of any specific institution. Institutional investors should seek financial advice as to the appropriateness of investing in any security or investment strategy mentioned or recommended. This information is not and should not be construed as a solicitation to buy or sell any security or securities. | |

|

In collaboration with ICBA’s education department, ICBA Education, certification programs, seminars, online training, and a host of resources are now available on our website, making it easier for you to find needed education. The new Affiliate Education Program will ensure that collectively, we put community banks in contact with the training tools necessary to grow bankers’ knowledge and skills.

Additionally, the program will also support IBANYS for every ICBA training course, seminar, event registration and resource purchased, ICBA will donate 10 percent of eligible purchases to IBANYS.

Let’s all win by increasing knowledge, improving efficiency, and investing in our employees while working together to uplift the industry we love—community banking!

Use This Code When Registering: NY-IBANYS

| | |

|

|

Play ball!

National pastime gives us some portfolio management guidance.

By Jim Reber, ICBA Securities

As we’re getting into the warmer months, it’s reassuring that baseball season is well underway. Your correspondent confesses a deep and abiding passion for the sport. While I’ve been only partially successful in getting my wife engaged in watching live baseball, she has gamely accompanied me to over two dozen major league stadiums. Nothing says “springtime” to me quite like the crack of a wooden bat on horsehide, and the roar of a crowd. Might I add a beer and a hot dog?

Read Article

| |

|

LEGISLATIVE NEWS

-

Latest Reports From Albany. Here are the new reports from the NYS Legislature on bill introductions and bill activity from last week, and on committee agendas for this week. These reports will also be posted on our website under the “Advocacy/Legislative Updates” tabs.

-

Bank of Rochester Bill. Over the past few weeks, IBANYS has taken a very proactive approach to opposing the bill on creating a public/municipal bank called Bank of Rochester. In lockstep with the local community banks, Rochester Chamber of Commerce and NYBA, we strongly opposed the bill and provided alternative solutions that meet the issues. Creating a public bank for local projects is no small task for the city and/or state. Many existing programs will be better served to handle the projects for the city of Rochester, i.e., Pursuit, Capital Access Program, creation of MDI's, CDFI's, etc. We will stay on top of this for the last weeks of session and provide updates.

-

Polling On Some Pending Legislation. As the New York state legislative session draws to a close, a new Siena College poll finds support for several items before the Senate and Assembly.

-

Assembly Speaker Heastie told colleagues they will likely remain in Albany until June 7 to finish up -- a day after the scheduled June 6 end of the session. As of now, session is not expected to last into the following week. Legislators are motivated to get home, as it’s an election year and early voting for primary races begins June 15. https://www.politico.com/newsletters/new-york-playbook/2024/05/29/the-city-hall-power-struggle-is-accelerating-00160333?nname=new-york-playbook&nid=0000014f-1646-d88f-a1cf-5f46b74f0000&nrid=00000152-f737-dcf0-a7d7-f73fb7700001&nlid=630317

REGULATORY UPDATE

-

The State Budget Analysis. More than a month after the state budget was enacted, the New York State Division of the Budget on Friday released the Fiscal Year 2025 Enacted Budget Financial Plan, providing the first full picture of the State’s fiscal condition. The Citizens Budget Commission (CBC) -- a nonpartisan, nonprofit civic think tank and watchdog whose mission is “to achieve constructive change in the finances, services, and policies of New York City and New York State government” – commented: 1) The total “All-Funds” spending for FY 2025 will be $239 billion, $2 billion higher than the State reported when the budget was enacted. 2) Due to strong tax receipts at the end of FY 2024, the State added $1.5 billion more to reserves, bringing the total to $21.1 billion. 3) Adjusted State Operating Funds Spending Increases 7.8 Percent, or $10.4 Billion, in Fiscal Year 2025. 4) Through fiscal year 2028, average annual SOF spending growth is projected at 4.1 percent. 5) Projected fiscal year 2028 SOF spending is now $2.4 billion greater than originally proposed.

-

Gaps Remain. From the CBC analysis: The enacted state budget drives a $16.1 billion structural budget gap. Gaps range from $2.3 billion in fiscal year 2026 to $7.3 billion in fiscal year 2028 -- smaller than they otherwise would be since the budget relies on temporary, non-recurring resources. The larger structural imbalance is “masked” by $2.9 billion from expiring tax increase, $2.5 billion in prior debt service prepayments, and $3.5 billion from rolled resources. The structural imbalance is approximately unchanged from the Executive Budget proposal because higher tax receipts of $2.5 billion are offset by the omission of savings proposed by the Executive and greater reliance on rolled resources in fiscal year 2028. The State’s Division of Budget acknowledges a range of economic uncertainties facing New York for the rest of the decade, including the post-pandemic aftershocks on population growth and the real estate sector.

-

Big Change Finalized At OCM. Chris Alexander, the head of the State’s Office of Cannabis Management (OCM), has resigned after weeks of public turmoil between the agency and Governor Hochul’s office. In a statement, Hochul noted: “As OCM transitions into its next phase, we look forward to continuing the world of building the strongest, most equitable industry in the nation.” Hochul appointed Alexander in September 2021. In January, she called the rollout of the legal market a “disaster” and ordered a 30-day review of the agency by the Office of General Services. This month, she released a report following the review that criticized the inexperienced leadership of the OCM and pointed to inefficiencies in the licensing process, as well sparse service for applicants awaiting determinations on their licenses.

POLITICAL PERSPECTIVES

-

Status Of NY House Races. The Cook Political Report’s (CPR) “House Race Ratings” assesses the competitiveness of all House elections in 2024 based upon the district's political makeup, candidates' strengths and weaknesses, the political environment in the state and nationally, and interviews with candidates and campaign professionals. Ratings are classified as: 1) Likely: Races not considered competitive at this point but have the potential to become engaged; 2) Lean: Races considered competitive, but one party has an advantage; 3) Toss Up: Races are most competitive; either party has a good chance of winning. Here are the newest ratings for New York State as of Friday, May 24. Likely Democratic: Rep. Suozzi (D-3rd CD, L.I.); Lean Democratic: Rep. Pat Ryan (D-18th, Hudson Valley) and Rep. Brandon Williams (R-Syracuse); Toss-Ups: Rep. Anthony D’Esposito (R-4th CD, L.I.), Rep. Mike Lawler (R-Hudson Valley) and Rep. Marc Molinaro (R-19th CD, Southern Tier); Likely Republican: Rep. Nick LaLota (R-1st CD, L.I.)

-

But First, The Key Primaries. As many as seven of New York’s 26 congressional seats are considered competitive in November, but before the general election, here are the primary races to watch.

-

Who Would Chair? Speculation abounds over who might chair key House committees in 2025 if Democrats regain control in November. Regarding the Financial Services Committee: Former Chair Maxine Waters (D-CA) will be 86 in August, but there’s every reason to believe she would again be the chair in 2025. If not, two New Yorkers are seen as potential chairs: Reps. Nydia Velazquez (D-Brooklyn) or Gregory Meeks (D-Queens). https://punchbowl.news/archive/52924-punchbowl-news-am/

| |

|

LEGISLATIVE REPORT

-

Farm Bill Moves To House Floor. The House Agriculture Committee passed the “Farm, Food and National Security Act of 2024” (H.R. 8467) on a 33-21 bipartisan vote. It now moves to the House floor for consideration. In a national news release, ICBA said the bill has numerous positive enhancements for American farm policy, though there are provisions in the bill that cause concerns for community banks. ICBA has been the only national banking trade group to weigh in against farm bill provisions to expand the FCS’s nonfarm lending authority and disparate regulatory treatment. IBANYS also emphasized these points during our meetings with the N.Y. congressional delegation. Community banks: Use ICBA’s “Be Heard” grassroots action center to call and write your Members of Congress on the industry’s farm bill priorities.

-

CBDC Bill Update. ICBA commended House members who voted to pass ICBA-advocated legislation restricting the ability of the federal government to introduce a U.S. central bank digital currency. The CBDC Anti-Surveillance State Act (H.R. 5403), introduced by House Majority Whip Tom Emmer (R-Minn.), passed by a bipartisan vote of 216-192. The bill, which ICBA was the first banking trade to support, was a key lobbying issue during the recent ICBA Capital Summit. The bill: 1) Prohibits the Federal Reserve Banks from offering products or services directly to individuals, maintaining individual accounts, or issuing a CBDC to individuals or through an intermediary, and 2) Prohibits the Federal Reserve and the Federal Open Market Committee from using a CBDC to implement monetary policy.

-

National Data Privacy Standards? The House Energy and Commerce Committee’s Subcommittee on Innovation, Data, and Commerce advanced draft legislation to establish a national data privacy standard. The bill passed out of the subcommittee by voice vote. The “American Privacy Rights Act” discussion draft would preempt state data security laws, but does not include clear language exempting financial institutions subject to Gramm-Leach-Bliley Act data security standards. In a letter ahead of the markup, ICBA and other groups urged the subcommittee to amend the bill to exempt all financial institutions subject to GLBA regulations. The groups said failing to include a clear exemption would lead to duplicative and conflicting requirements for financial institutions already subject to GLBA oversight. The discussion draft will next be considered by the full committee.

-

Tell Congress: Respond On Credit Unions. Following the 10th acquisition of a community bank by a tax-exempt credit union this year, ICBA issued a national news release renewing calls for Congress to respond: “With tax-exempt credit unions now accounting for 10 bank acquisitions already in 2024 — roughly a quarter of this year’s acquisition total — Congress must act on this dangerous trend, which expands the federal tax exemption for more than $2 trillion in credit union assets and displaces trusted providers of credit in local communities.” Community banks: Use ICBA’s Be Heard grassroots action center to call on their members of Congress to hold a hearing on credit union policy. Additional resources are available on the ICBA website.

;

REGULATORY UPDATE

-

FDIC Quarterly Banking Profile. Reports from 4,568 commercial banks and savings institutions insured by the FDIC report aggregate net income of $64.2 billion in first quarter 2024, an increase of $28.4 billion (79.5%) from the prior quarter. https://www.fdic.gov/analysis/quarterly-banking-profile/?source=govdelivery&utm_medium=email&utm_source=govdelivery. A large decline in noninterest expense because of several substantial, non-recurring items recognized by large banks in the prior quarter, as well as higher noninterest income and lower provision expenses this quarter, contributed to the quarterly increase. These and other financial results for first quarter 2024 are included in the FDIC’s latest Quarterly Banking Profile released today. Community Bank Net Income Increased Quarter Over Quarter: Quarterly net income for the 4,128 community banks insured by the FDIC was $6.3 billion in the first quarter, an increase of $363.2 million (6.1%) from fourth quarter 2023. Lower realized losses on the sale of securities and lower noninterest and provision expenses more than offset lower noninterest and net interest income. The community bank pretax ROA increased six basis points from one quarter ago to 1.13 percent. FDIC Chairman Gruenberg stated: ““The banking industry continued to show resilience in the first quarter. Net income rebounded, asset quality metrics remained generally favorable, and the industry’s liquidity was stable. However, the banking industry still faces significant downside risks from the continued effects of inflation, volatility in market interest rates, and geopolitical uncertainty. In addition, deterioration in certain loan portfolios, particularly office properties and credit cards, continues to warrant monitoring.” Quarterly Banking Profile Home Page (includes previous reports and press conference webcast videos) ; Charts and Data; Chairman Gruenberg’s Press Statement

.

-

Concerns Over Freddie Second Mortgages Proposal. ICBA submitted a letter to the FHFA outlining concerns with a Freddie Mac proposal to purchase certain closed-end second mortgages. ICBA said: 1) The loans are readily available in the private sector from community banks; 2) The proposal does not provide sufficient details regarding pricing, property valuation, and risk management and is not consistent with Freddie Mac’s core housing mission; 3) This product is inappropriate given that Freddie Mac remains undercapitalized and in conservatorship.

-

Feds Amending Call Report/FFIEC Forms. The federal banking agencies announced they are moving forward with proposals to amend certain references in call report and FFIEC 002 forms. Last fall, the agencies proposed revisions to all three versions of the call report (FFIEC 031, FFIEC 041, and FFIEC 051) and the FFIEC 002 report. After considering the comments received on these notices, the agencies are moving forward with: 1) Certain proposed revisions related to replacing references to “troubled debt restructurings” with “modifications to borrowers experiencing financial difficulty.” 2) Certain technical clarifications to reporting web addresses of depository institution trade names; 3) Standards for electronic signatures to comply with the call report signature and attestation requirement. Comments have been reopened on these issues and are due by June 21.

-

Latest From FDIC On Economy, Markets & Risk. The FDIC published its 2024 Risk Review, which summarizes conditions in the U.S. economy, financial markets, and the banking industry. The FDIC’s Risk Review is an annual publication and based on year-end banking data from the prior year. The 2024 Risk Review provides an overview of banking risks in 2023 in five broad categories: Market risks that include funding and liquidity risks; Credit risks in various portfolios including commercial real estate and consumer lending; Operational risks; Crypto-asset risks; and Climate-related financial risks.

-

Fed Governor Michelle Bowman said it is important to continue to reduce the size of the Fed’s balance sheet while the economy is still strong to allow the Fed to more effectively and credibly use its balance sheet to respond to future economic and financial shocks. Bowman said using the Fed's balance sheet as a monetary policy tool has demonstrated it can be an effective way to ease financial conditions and support the economy in periods in which the conventional monetary policy interest rate tool has reached the zero lower bound. Bowman noted policymakers must use the balance sheet judiciously, citing the need to balance the risks of doing too little or too much in pursuing their monetary policy mandates.

-

Will DFS's Harris Be Biden’s Next FDIC Chairman? There is growing speculation on who will succeed FDIC Chairman Gruenberg: https://www.cnn.com/2024/05/21/politics/biden-administration-financial-regulators-fdic/index.html. The Chairman’s term is five years, so a Biden nominee could continue in office well beyond the November election. Among those mentioned: 1) Christy Goldsmith Romero, a Democratic member of the Commodity Futures Trading Commission (CFTC); 2) Treasury Undersecretary for Domestic Finance and former top Federal Reserve official Nellie Liang; 3) New York State Department of Financial Services (DFS) Superintendent Adrienne Harris, who was in contention for the job in 2022; 4) Sandra Thompson, Director of the FHFA, who spent 23+ years at the FDIC; 5) Graham Steele, Assistant Secretary for Financial Institutions at Treasury (and former adviser to Senate Banking Committee Ranking Democrat Sherrod Brown, D-OH.) A White House official described the process as “fast-moving but still early.” https://www.reuters.com/business/finance/fdic-needs-fresh-start-with-new-chair-who-is-not-part-leadership-white-house-2024-05-21/.

-

ICBA, the Center for Payments, and Nacha are conducting the 2024 Payments Fraud Survey to help financial institutions enhance their defenses against payments fraud. Community bankers are encouraged to provide their insights by this Friday, May 31, to help evaluate the current methodologies employed by financial institutions in identifying and responding to instances of payments fraud. Participating banks will receive a personalized Company Performance Report of the survey findings and similarly situated institutions. Each financial institution should submit only one survey response.

DEMOGRAPHIC INSIGHT

-

The “American Banker” reports the financial services industry has largely recovered from the negative shocks of the 2008 financial crisis, although the most recent release of the “Edelman Trust Barometer” found banks need to address a significant level of skepticism among consumers. “Insights for the Financial Services Sector” -- a supplemental report connected to the “2024 Edelman Trust Barometer” -- found banking scored a 65, up three points since last year and 12 points from a decade ago. The index grades public and private institutions on a 100-point scale, with 60 the threshold for trusted status. https://www.americanbanker.com/news/trust-in-banks-trending-in-the-right-direction-new-survey-finds

| | | | |