Welcome to Michelle's 12 Days of Tax Tips!

|

|

Tip 2:

New 20% Qualified Business Income "QBI" Deduction available for Self-Employed Individuals

|

|

Greetings!

If you have self-employed income for 2018, this edition of my 12 Days of Tax Tips is for you!

Last week, I issued my digest about deferral and exclusion of certain capital gains tax via a qualified opportunity fund. I'm linking it

here for your reference.

Today, I am breaking down the Qualified Business Income Deduction: What is it? How does it work? And how can you benefit from it?

|

|

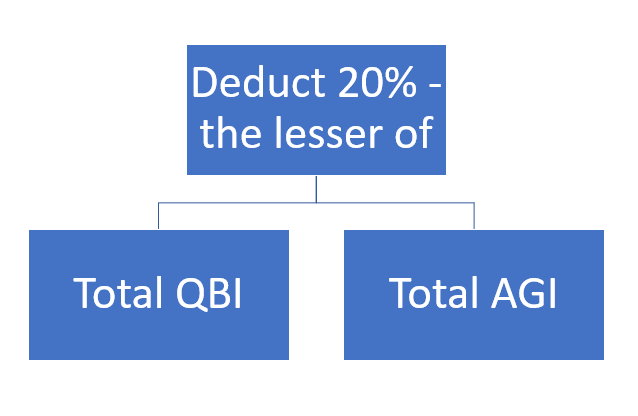

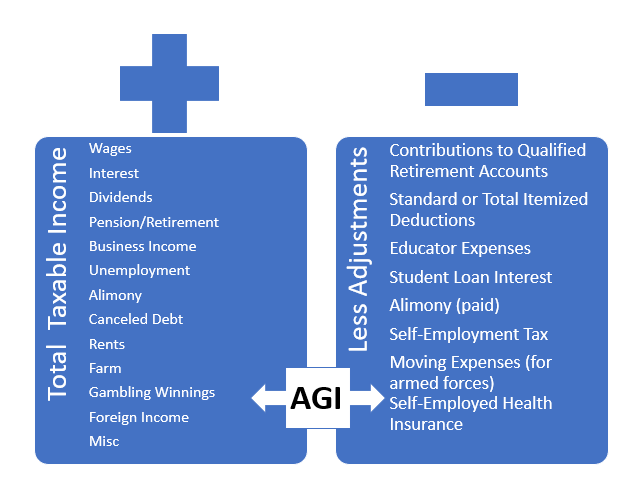

Under the new tax law, a deduction is provided for taxpayers who have self-employed income. The deduction is calculated as 20% of your net income from business activity, or your total adjusted gross income, whichever is less.

|

|

QBI is your gross earnings less expenses - AGI is the total of all income less adjustments, including your QBI

|

|

|

|

Deferring and accelerating expenses based on the AGI parameters can optimize your QBI deduction

|

|

|

|

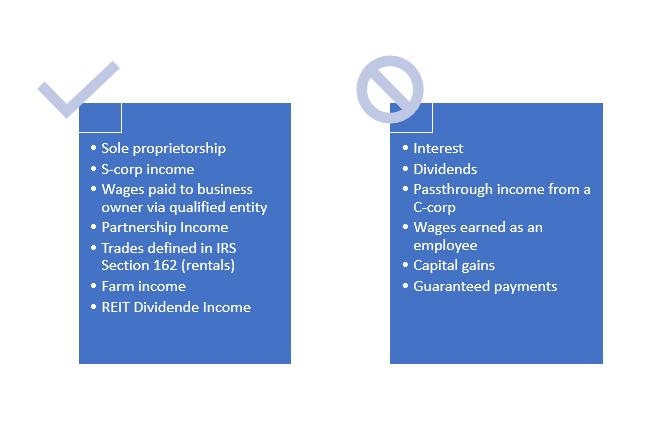

Character of income determines if it is QBI eligible and any applicable limitations.

|

|

|

|

|

Deduction Phaseouts Based on Income and Filing Status: Limitations are based on total income, as the deduction begins to phase out after certain income thresholds are met: The phase in for single taxpayers is $157,500 and $315,000 for married filing jointly taxpayers.

This phase out works as a double edged sword, depending if one spouse is making a lot more money for the household than the other, and is right in the goldilocks zone not making more than $315k combined, or if they well surpass it, they may want to consider filing separate from their spouse to not lose the deduction completely.

|

|

Miscellaneous factors effecting QBI Deduction

|

|

Word to the wise...

I mentioned earlier in this letter that other factors involved in reporting your income and deductions will effect optimization of this exclusive deduction which will sunset in 2025.

|

|

- The factors involved in reporting your total income, and adjustments to income can effect the 20% basis of the QBI deduction.

- Sole shareholders of an S-corporation should be aware that the QBI deduction is limited to 20% of their officer compensation, and 2.5% of unadjusted basis in business property.

- Businesses operating at a loss cannot take the QBI deduction, and recognize tax if deduction is taken in a subsequent year.

|

|

- Special advantages and suspension of limitations may differ for taxpayers not considered a Specified Service Trade or Business "SSTB" by the IRS.

|

|

- Dividends coming from a qualified Real Estate Investment Trust "REIT" are the only dividends specified that qualify for the QBI deduction.

|

|

|

- The new tax law may allow capitalized assets to be fully depreciated for tax purposes to lower your taxable net profit. However, keep in mind that take this bonus depreciation can lower your QBI deduction.

|

|

- Though ordinarily considered for purposes of calculating AGI, for considering whether the deduction is based off of AGI or QBI, the lesser of, current capital gains and losses are taken out of the equation

|

|

|

|

|

If you asked Santa for an amazing tax adviser to save you money this year, lucky for you, your wish has been granted early!

With my resources, I can help you execute tax deferring strategies and investments that will save you money!

|

|

Further, my additional gift to you this holiday season is my $50 rebate program* on your first tax service, and per each referral to your friends and family :)

Lastly, s

tay tuned for 10 more days of tax tips; and I w

ish you health, wealth and prosperity this holiday season.

|

|

Happy Holidays & Many Happy Returns,

|

Bringing Tax Saving Joy and Cheer this Holiday Season to Individuals and Businesses

|

|

“Fearlessness is like a muscle. I know from my own life that the more I exercise it the more natural it becomes to not let my fears run me.”

– Arianna Huffington, president and editor in chief The Huffington Post Media Group

|

|

*Special offer details* Offer available until 2/15/18 unless otherwise stated and is subject to change at anytime based on facts and circumstances. Recipients must submit valid W9 to redeem. Referred must complete paid services. Fees are open to be paid via choice of Amazon gift card, check, Venmo transfer, more.

Contact me

for details*

The content of this email is confidential and intended for the recipient specified in message only. It is strictly forbidden to share any part of this message with any third party, without a written consent of the sender. If you received this message by mistake, please reply to this message and follow with its deletion, so that we can ensure such a mistake does not occur in the future. Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties. If desired, I would be pleased to perform the requisite research and provide you with a detailed written analysis. Such an engagement may be the subject of a separate engagement letter that would define the scope and limits of the desired consultation services.

|

|

|

|

|

|

|