CURRENT MARKET PERSPECTIVE | |

|

BEWARE: NOT EVERYTHING WE SEE IS REAL!

"GOOD NEWS IS NOW GOOD NEWS!"

Click All Charts to Enlarge

| |

MONTHLY MATASII CROSS STILL A BUY - The S&P 500 target price of 5540 shown above matches our S&P 500 "Thought Experiment" which we have been showing in our Newsletter for a few months now. The "Thought Experiment" is a shorter Daily view analysis which matches the above Monthly analysis connecting multiple intersection reference points. The reference points are shown by seven non-shaded red circles within a trend channel and rate of change analysis. We have found that a multitude of these connecting factors often "points the way" through more or less long term controlling market "boundary conditions". | |

|

1 - SITUATIONAL ANALYSIS

SOMETHING JUST ISN'T RIGHT??

Wednesday night I pointed out that something wasn't right with the Inverse 10Y Treasury Yield not trading in concert with the Nasdaq (chart below)?

| |

We are also seeing the 10Y Treasury Yield diverging significantly against the e-Mini contract (chart top right)

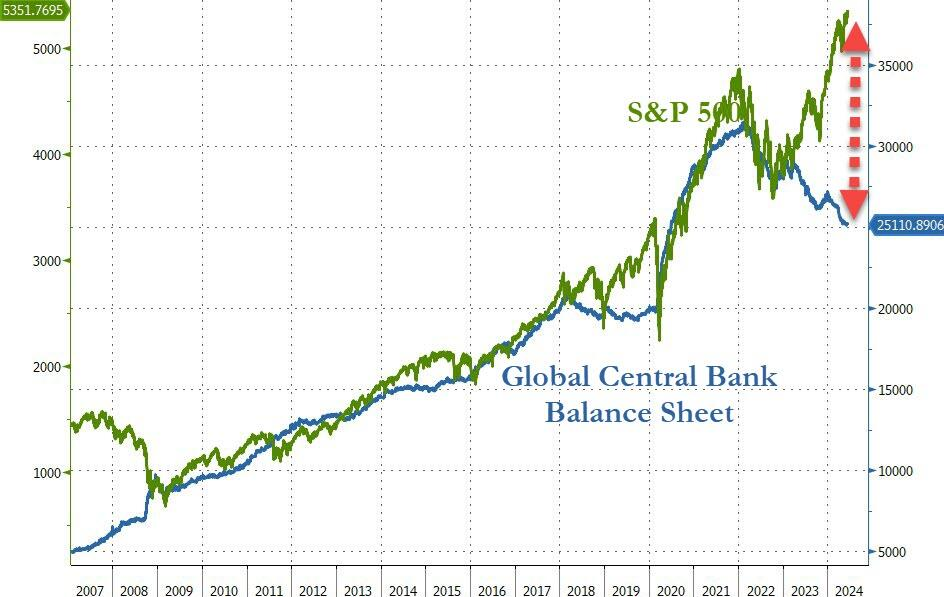

Additionally, we see the S&P 500 diverging significantly from the Global Central Bank Balance Sheet (chart right).

| |  |

| |

|

WHAT EXPLAINS THE DIFFERENCE?

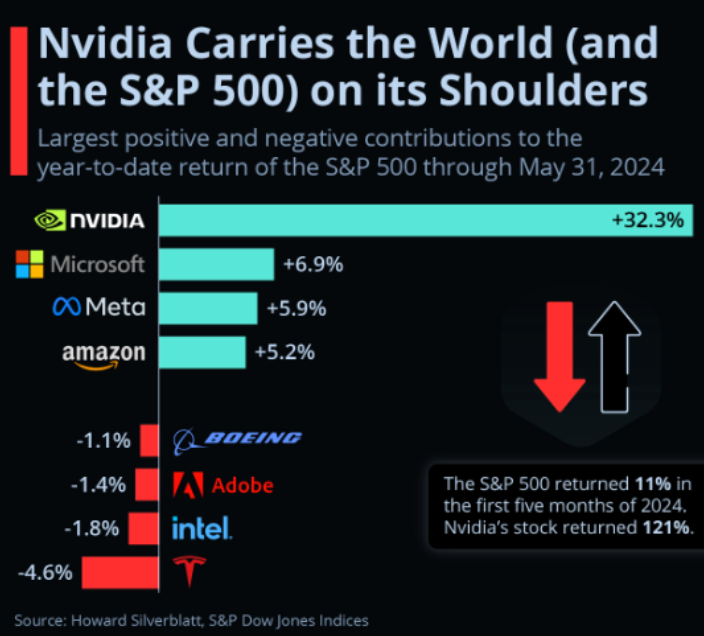

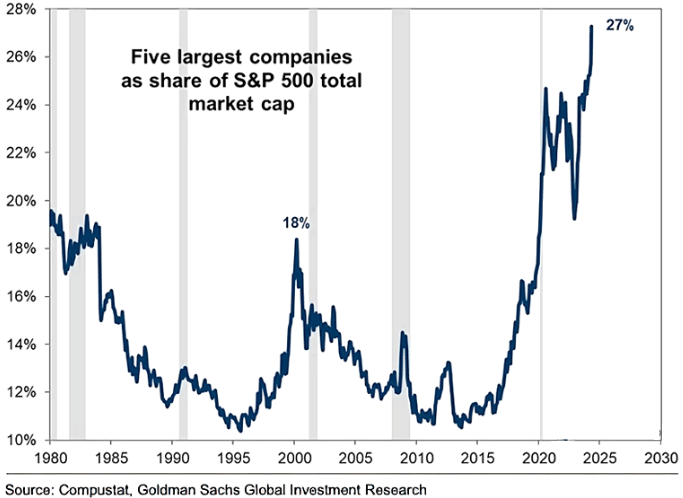

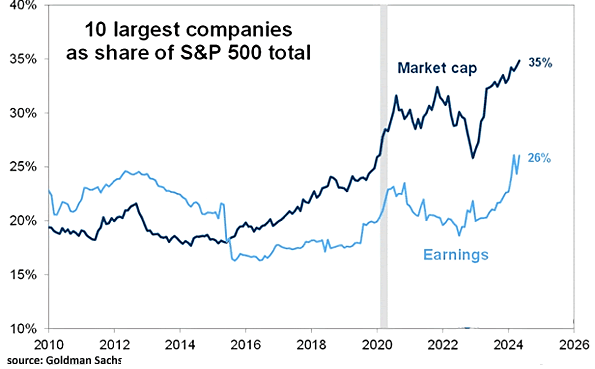

The short answer to explain the divergences above is the extreme and historic narrowness of the Breadth of the US Equity market. The market is now controlled by the Magnificent 7 in a manner never seen before. The Magnificent 7 ascent has been built on effective use and funding of Stock Buybacks. Since January of 2024 the further parabolic explosion of the Magnificent 7 has been further fueled by Nvidia and the current AI Mania.

The long answer involves a full understanding the roll Shadow Banks (specifically Private Equity players) are now playing in global equity markets, corresponding shrinking stock floats & pools and the colossal growth in controlling derivative trading.

That discussion we must leave for a future subscriber video.

| |

27%: Five largest companies as share of S&P 500 total market capitalization. | | |

35%: Ten largest companies as share of S&P 500 total. | | |

|

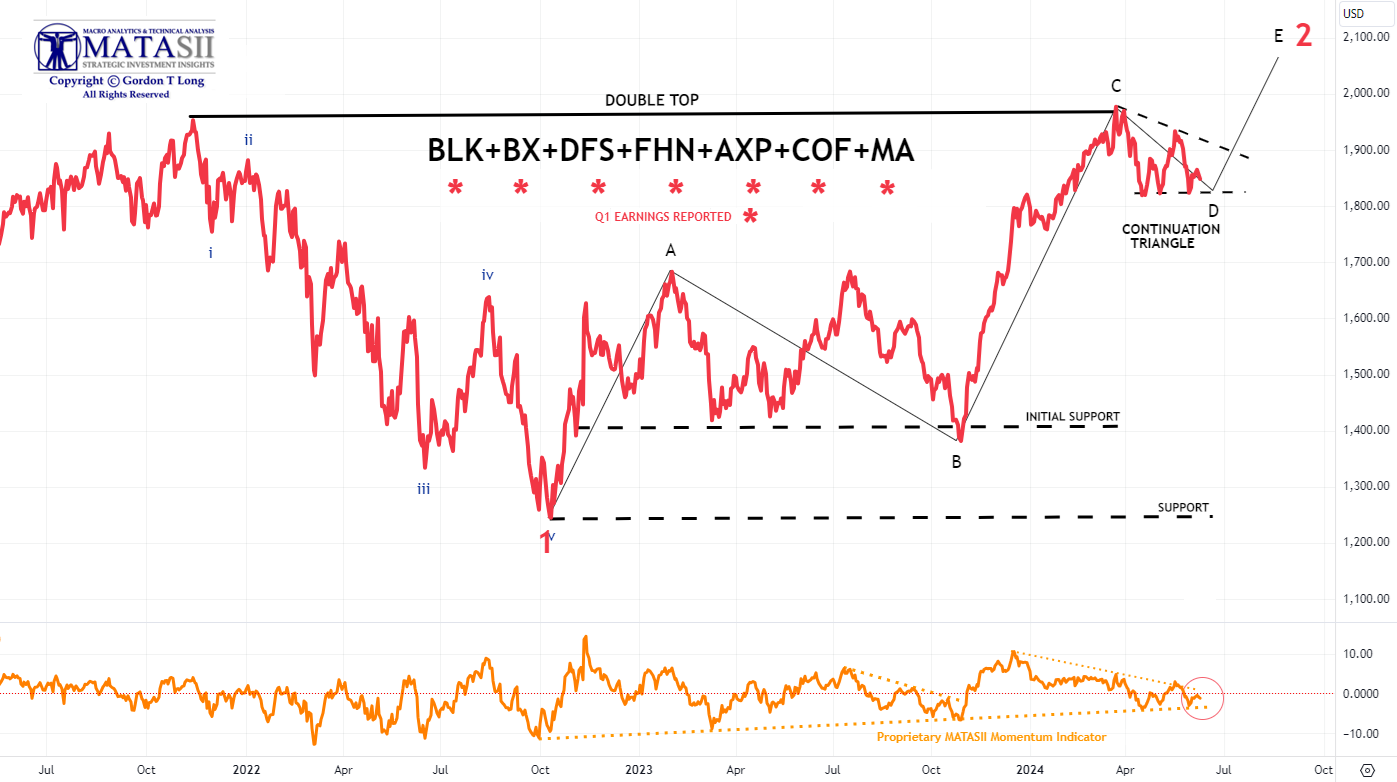

"AS GO THE FINANCIALS, SO GO THE BANKS: AS GO THE BANKS, SO GO THE MARKETS"

MATASII FINANCIAL STOCK INDEX

We continue to keep an eye on both the Bank and Financial stocks to give us an early signal of market direction. We have been showing the banks over the last few weeks but the Financials now appear to be giving a clearer signal.

- The MATASII Financial Index stocks has begun to exhibit a potential continuation triangle pattern.

- The Elliott Wave analysis supports an "E" wave higher as part of an ABCDE pattern.

- Momentum (bottom pane) has found long term support and needs to be watched to see if it breaks shorter term overhead resistance shown by a dotted descending orange momentum trend line.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

2 - FUNDAMENTAL ANALYSIS

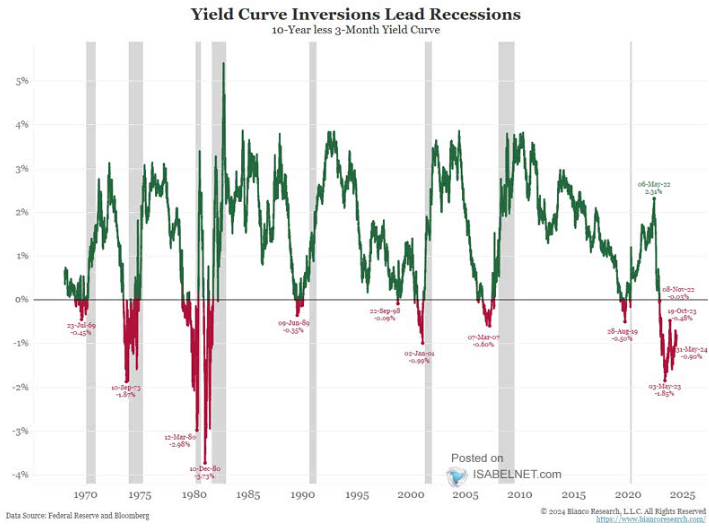

DON'T BELIEVE THE HYPE - A PE KILLING RECESSION IS IN THE WINGS!

Although the 10Y-3Mo Yield Curve is not yet on the verge of inverting, historical data suggests that the "uninversion" is a reliable indictor of an impending recession.

What might trigger that?

We believe it is the breaching of an Unemployment rate of 4.0%. The unemployment rate last month moved up to 3.9%. On Friday it moved to 4.0%.

The JOLTS reports, layoffs and rising jobless claims suggest the Labor situation is weakening significantly. The Friday Labor Report as we will show in tomorrow's Newsletter is highly manipulated.

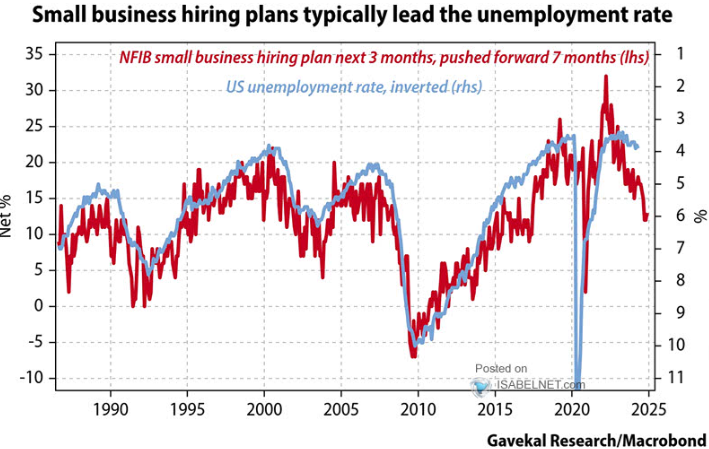

CHART BELOW

Small business hiring plans typically lead the US Unemployment Rate. The NFIB small business hiring plans for the next 3 months, when pushed forward seven months, has proven to be a strong leading indicator. Clearly the signal is for a rising Unemployment Rate to soon occur - maybe Friday?

| |

|

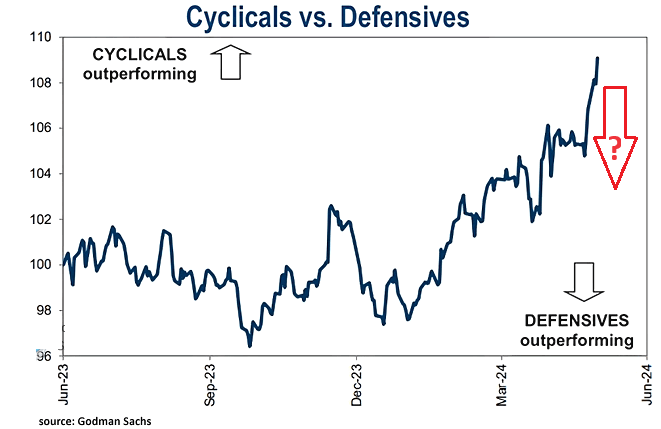

CHART RIGHT:

Investor sentiment is often mirrored in the performance of cyclicals and defensive equities. The anticipation of economic expansion usually prompts a preference for cyclical stocks, causing them to outperform defensive stocks. This is what we have been witnessing with strong earnings outlooks.

However, if the US Unemployment Rate starts to break 4.0% then the worry of a recession will weaken outlooks and a shift to defensives is likely to occur.

EVERYONE EXPECTS NO LANDING WITH A FEW EXPECTING A SOFT LANDING -

ARE THEY RIGHT?

| |

|

MARKET DRIVERS

As goes NVDA, so goes the MAG-7, As Goes Mag-7 so goes The Market.

| |

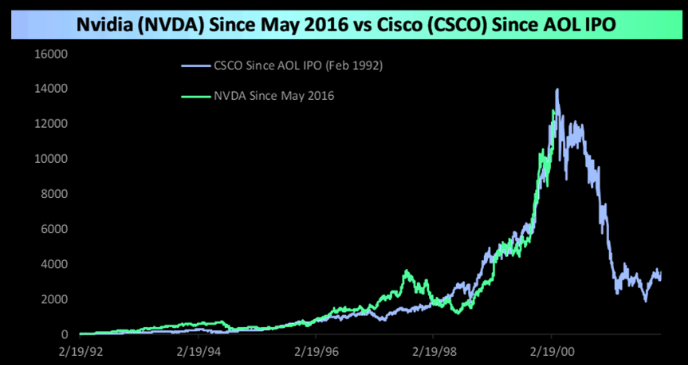

NVDA - Daily

CHART RIGHT: In the chart to the right, we have overlaid the performance of NVDA since May 2016, when Alphabet CEO Sundar Pichai first formally referred to the company as a leader in an “AI first world” to the performance of CSCO starting in February 1992 when America Online had its IPO. As shown, both stocks had insane and strikingly similar runs in the eight years following each of those events. On an ominous note, CSCO’s run at this point was only a month from its ultimate peak before an epic collapse. Then again, though, NVDA CEO Jensen Huang has said that he expects AI to be “bigger than the internet,” so maybe it’s not a fair comparison.

DOES THE MARKET NOW FINALLY BELIEVE NVIDIA HAS GONE TOO FAR, TOO FAST???

- 5 years ago, Nvidia had a market cap of just $100 billion. It is now the 3rd largest public company in the world and 17% away from being larger than Apple.

- Nvidia is now larger than Tesla and Amazon combined.

- Nvidia is now larger than the entire German stock market.

- At $2.6 trillion, Nvidia's market cap is now $890 billion higher than all of the companies in the S&P 500 Energy sector combined. The total net income of the Energy sector is $128 billion vs. $43 billion for Nvidia.

- Nvidia's share of the Data Center Compute market has grown from ~15% five years ago to ~80% today.

- NVDA opened another Unfilled Gap this week as it reached for new highs yet again before pulling back slightly on Thursday & Friday.

- NVDA's lift this week pushed through the upper channel boundary trend line.

- The MATASII Proprietary Momentum Indicator (lower pane) appears to be attempting to roll over.

-

The Dotted Black Trend line in the MATASII Proprietary Momentum Indicator pane is suggesting a potential Divergence has been set up. This is normally seen as a warning to the downside that is ahead if the Divergence isn't removed by a movement higher in Momentum.

- At some point the major unfilled gaps (at much lower levels) must be filled. NVDA therefore may becoming no longer a Short to Intermediate Long Term hold, but rather a position trading stock as others entering the space and force margins to contract.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

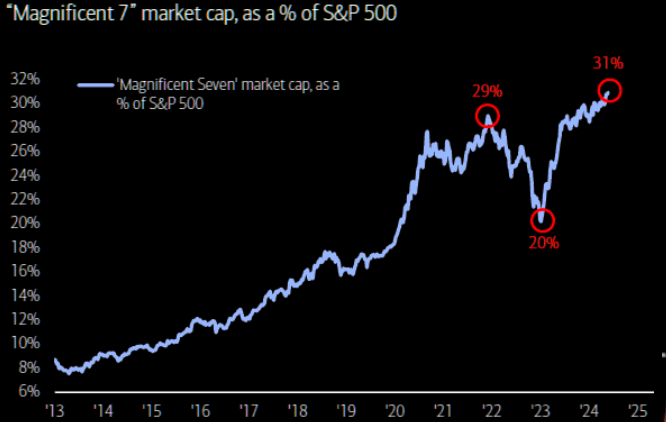

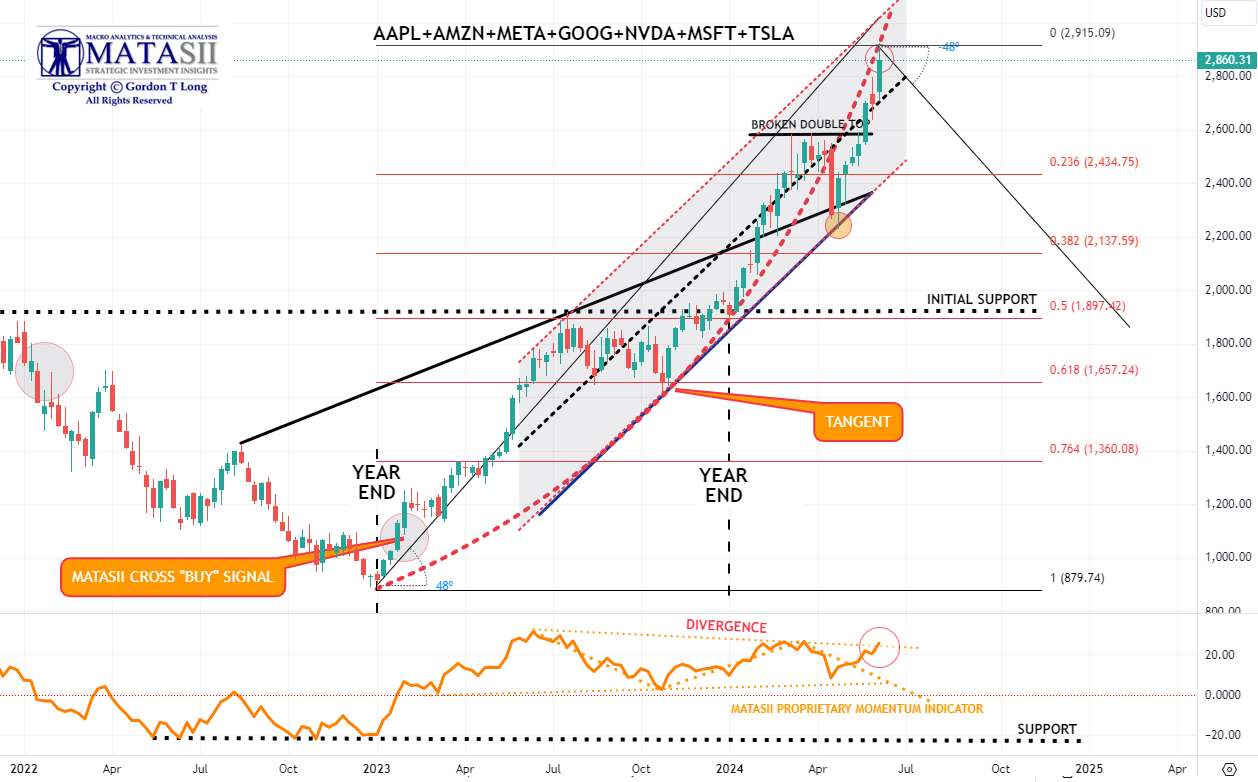

MAGNIFICENT 7

Magnificent 7 is up a magnificent 24% YTD (chart right), contributing >50% of SPX return (NVDA alone = 25%) as monopolistic mega tech monopolizes performance..

Total CAPEX + R&D for the Magnificent Seven this year is expected to total $348bn. (Think about that for a second).

Here’s another way to frame it - the Magnificent 7 is reinvesting 61% of their operating free cash flow back into

CAPEX + R&D!

-

The basket of 'Magnificent 7' stocks soared for the 6th week in the last 7 (and the best week in the last 7) before pulling back at the end of the week.

- The Magnificent 7 reached its rising parabolic trend (dashed red line).

- We continued to be concerned about the momentum Divergence signal that has been occurring for some time (bottom pane). NVDA has obviously extended the duration of the signal which we have tested again this week. When this occurs often there a is normally a significant drop that occurs. Caution advised.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

"CURRENCY" MARKET (Currency, Gold, Black Gold (Oil) & Bitcoin) | |

|

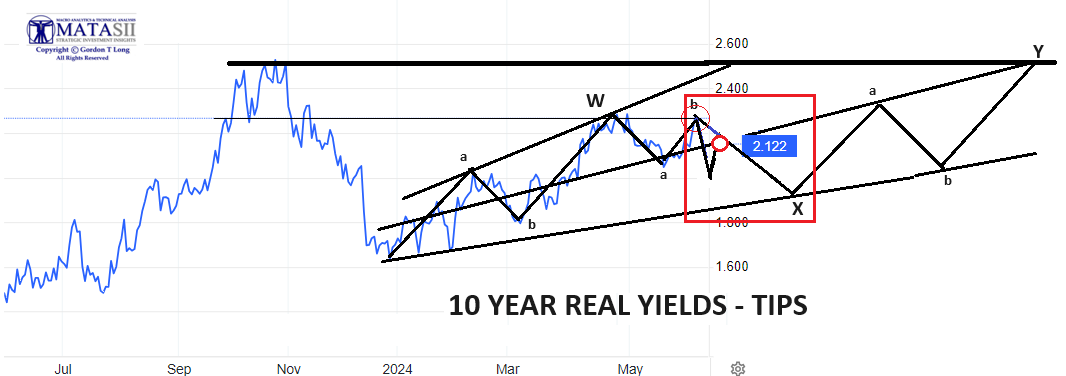

10Y REAL YIELD RATE (TIPS)

Real Rates reached our initial overhead resistance level of 2.25% before falling off hard as part of our expected "X" leg lower (chart right). On Friday the Biden Admin's apparent strong Labor Report pushed yields higher taking needed pressure off the Fed to reduce rates.

| |

CONTROL PACKAGE

There are TEN charts we have outlined in prior chart packages, which we will continue to watch closely as a CURRENT Control Set:

-

US DOLLAR -DXY - MONTHLY (CHART LINK)

-

US DOLLAR - DXY - DAILY (CHART LINK)

-

GOLD - DAILY (CHART LINK)

-

GOLD cfd's - DAILY (CHART LINK)

-

GOLD - Integrated - Barrick Gold (CHART LINK)

-

SILVER - DAILY (CHART LINK)

-

OIL - XLE - MONTHLY (CHART LINK)

-

OIL - WTIC - MONTHLY - (CHART LINK)

-

BITCOIN - BTCUSD - WEEKLY (CHART LINK)

-

10y TIPS - Real Rates - Daily (CHART LINK)

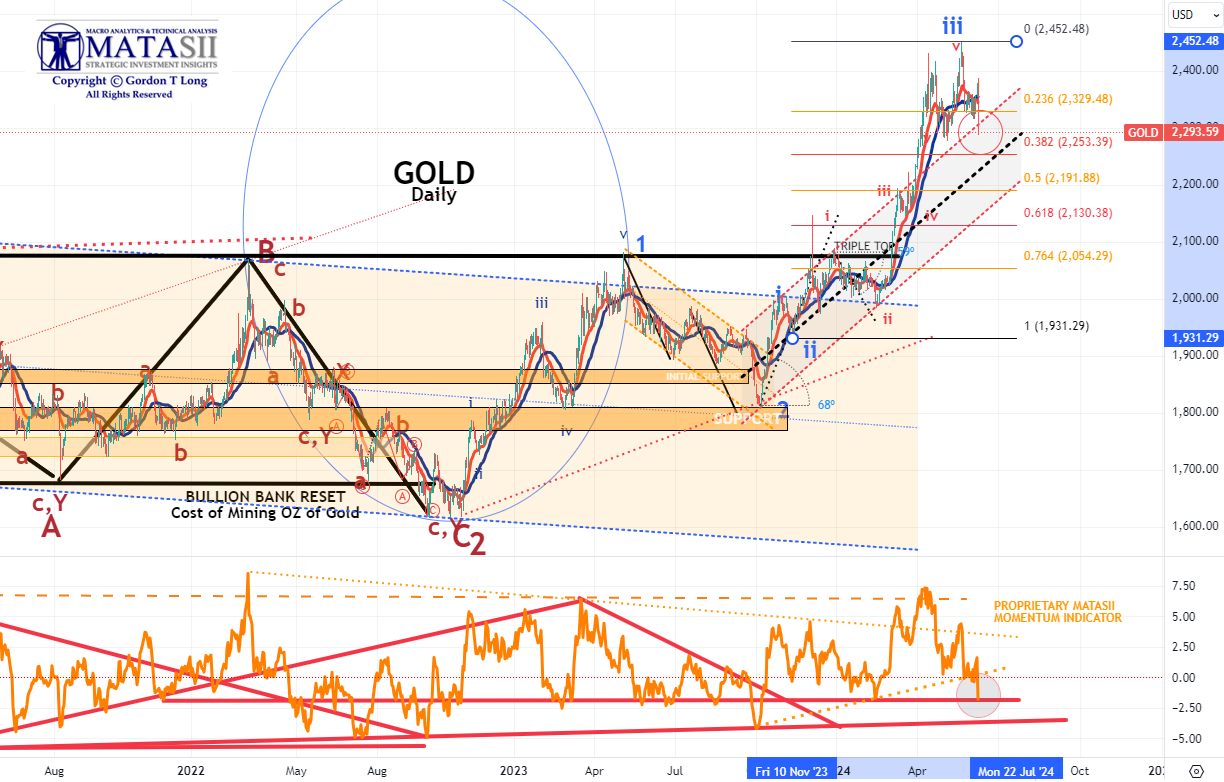

GOLD - DAILY

- Gold started to move again this week after the recent profit taking, and was up a solid $27 Wednesday and putting in an all-time high. Friday's strong Labor report ruined the party and gold sold off substantially to 2293/Oz.

- The Elliott Wave count still suggests a strong likelihood of a minimum retracement of 38.2% and likely in the area of 50% of this last "iii" leg.

- Momentum support (lower pane) shows gold has found an important support line. it should be noted there is another one even longer, slightly lower.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

CHART RIGHT: We have seen bears throw in the towel lately, but what if this is just another overshoot? We have seen similar setups play out before. Believe it or not, but this is the biggest down candle for the SPX since April 30th.

CONTROL PACKAGE

There are FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set":

-

The S&P 500 (CHART LINK)

-

The DJIA (CHART LINK)

-

The Russell 2000 through the IWM ETF (CHART LINK),

-

The MAGNIFICENT SEVEN (CHART ABOVE WITH MATASII CROSS - LINK)

-

Nvidia (NVDA) (CHART LINK)

| |

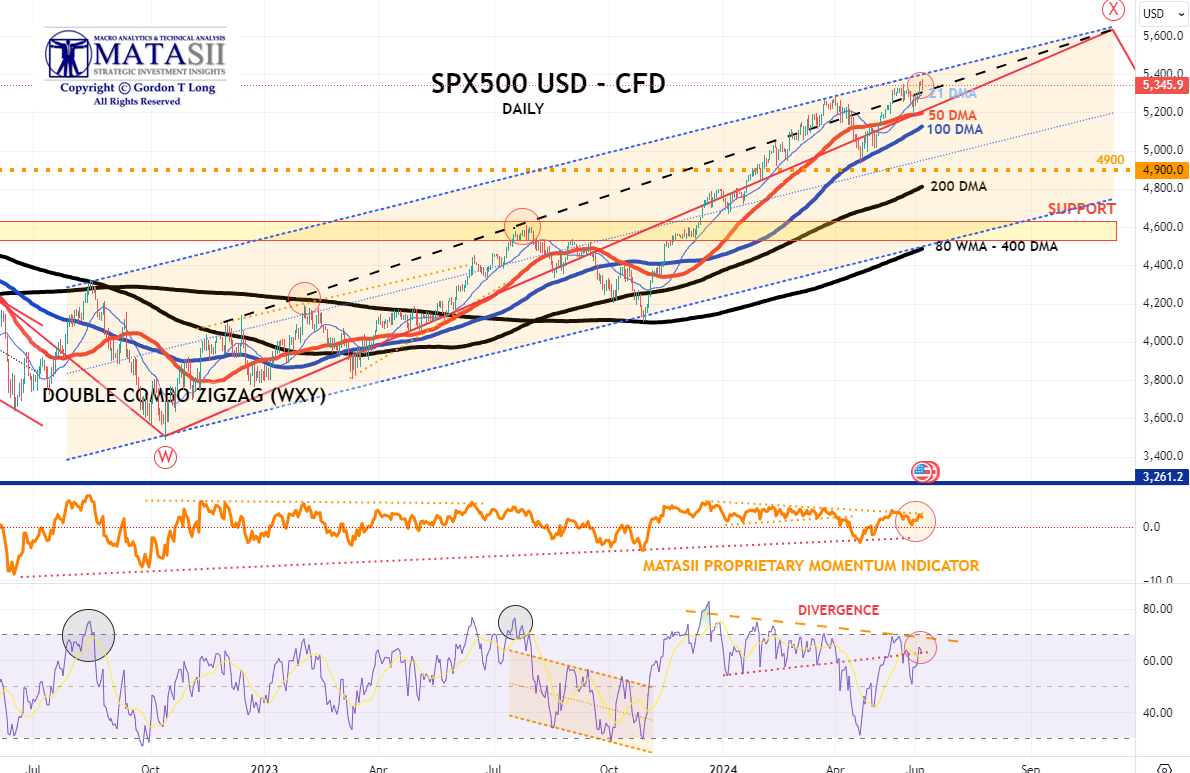

CHART RIGHT: We are stuck and need new narratives. The range that has been in place for months continues to hold. SPX is trading at the same levels we traded at in mid March. Note the 50 day coming in.

S&P 500 CFD

- The S&P 500 cfd rose aggressively this week towards its upper trend channel boundary line (NOTE: see Thought Experiment note below).

- However, the MATASII Proprietary Momentum Indicator (middle pane) appears to be showing signs of weakening within a Divergence pattern with price.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

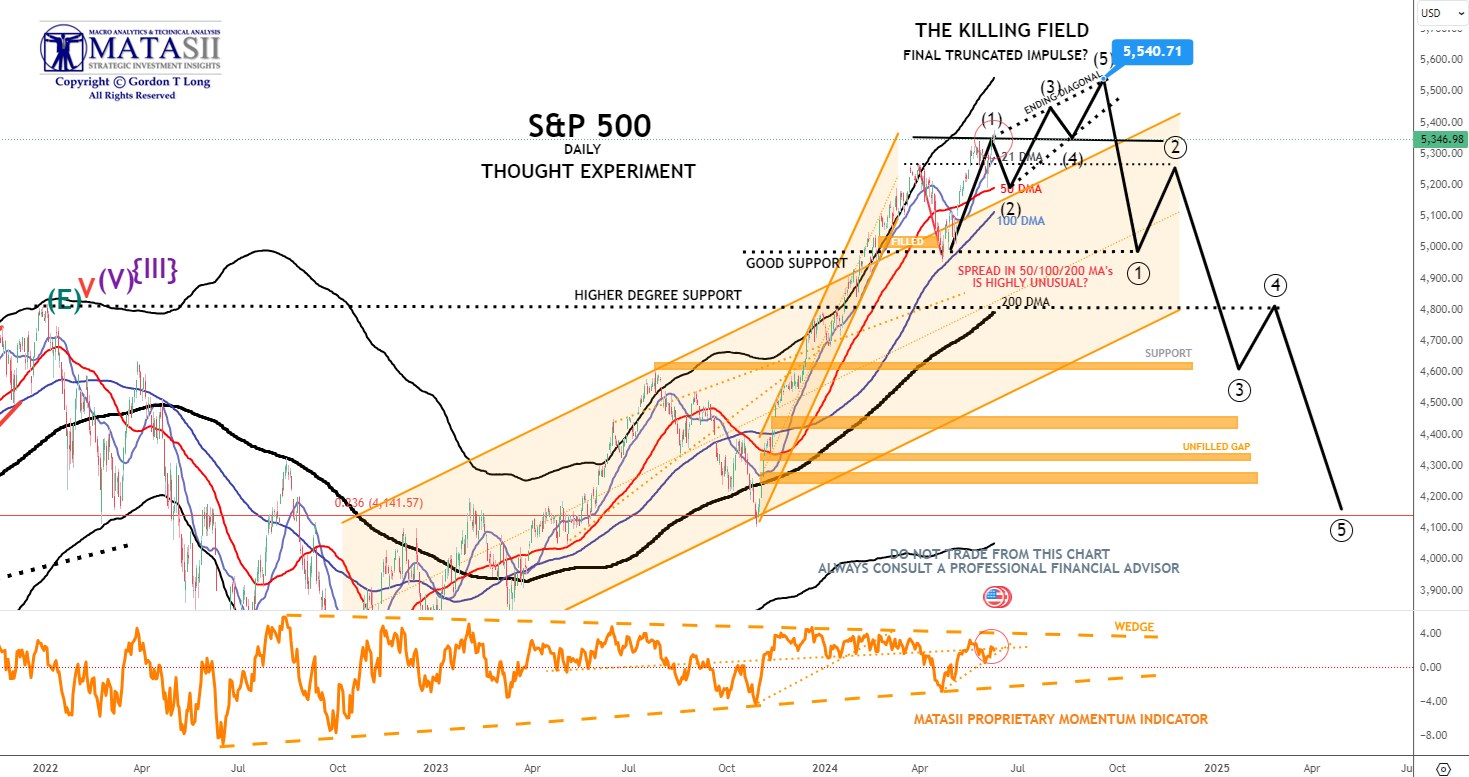

S&P 500 - Daily - Our Thought Experiment

Our Thought Experiment, which we have discussed many times previously in the way of a projection, suggests we have put in a near term top and will now consolidate before possibly completing one final small impulse higher OR put in a final Wave 5 of a higher degree.

NOTE: To reiterate what I previously wrote - "the black labeled activity shown below, between now and July, looks like a "Killing Field" where the algos take Day Traders, "Dip Buyers", the "Gamma Guys" and FOMO's all out on stretchers!"

- With an expected tidal wave of easing about to be unleashed by all central banks (Canada lowered rates Wednesday and the ECB lowered rates Thursday), it is no surprise that the S&P just hit a new all time high this week, up a whopping 30% from the October lows.

- However, the MATASII Proprietary Momentum Indicator appears to be showing signs of weakening (lower pane) with support quite a bit lower.

- The Divergence in Momentum (lower pane) needs to be noted along with a clear long term ending wedge.

OUR CURRENT ASSESSMENT IS THAT THE INTERMEDIATE TERM IS LIKELY TO LOOK LIKE THE FOLLOWING:

(NOTE - The black projection has not been changed since prior posts so as to serve as a reference.)

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

STOCK MONITOR: What We Spotted

MONDAY

- Stocks ultimately finished the Monday session mixed.

- Growth fears initially weighed on sentiment after the US Manufacturing ISM headline fell by more than expected. Within the data the Prices Paid component slipped beneath all analyst expectations.

- The data supported Treasuries across the curve but the downside in yields and softer prices data was not enough to provide a convincing tailwind to stocks.

- Stocks did close off the lows with outperformance in NVDA shares which helped the Nasdaq outperform after its slew of AI/Chip updates over the weekend.

- The fall in yields gave a helping hand to traditional havens with the Yen and Franc outperforming in FX while gold also saw decent upside.

- Crude prices slumped in the aftermath of the OPEC+ decision, which ultimately extended the official crude output cuts in 2025, while Saudi Arabia and Russia would also extend their voluntary production until the end of Q3 24, before being restored gradually until the end of September 2025.

- There will also be increased supply from the UAE by 300k BPD from Jan-Sept 2025.

INFLATION BREAKEVENS: 5yr BEI -3.0bps at 2.331%, 10yr BEI -2.3bps at 2.338%, 30yr BEI -2.1bps at 2.335%..

REAL RATES: 10Y -- 2.082%

STOCK SPECIFIC

- Nvidia (NVDA): Announced its next-gen of AI chips while the CEO pledged to release new AI chip technology on a one-year basis, faster than its prior two-year timeline, reports CNBC. The new architecture is called "Rubin" and follows the announcement of its upcoming "Blackwell" model.

- AMD (AMD): Announced a series of next-gen architecture and products aimed at ushering in a new era of AI experiences. Unveiled the Ryzen AI 300 and Ryzen 9000 series processors.

- Edwards Lifesciences (EW): To sell its Critical Care product group to Becton Dickinson (BDX) for USD 4.2bln in an all-cash deal.

- Autodesk (ADSK): Announced the results of its audit investigation and named Betsy Rafael as interim CFO. It also gave guidance above expectations.

- Spotify (SPOT): Raised its price for Premium in the US.

- Paramount (PARA): The latest Skydance deal values the co. at USD 15/shr, a 26% premium to Friday's close, via WSJ. CNBC says the deal should be announced very soon. Bloomberg reports that Skydance will offer USD 23/shr for voting shares.

- BestBuy (BBY): Double upgraded at Citi.

- GameStop (GME): “Roaring kitty” (Keith Gill) shows in a Reddit post his USD 116mln bet on GME.

- GlaxoSmithKline (GSK): Delaware judge allows over 70k Zantac lawsuits to go forward.

- Waste Management (WM: Confirmed reports that it is to acquire Stericycle (SRCL) +15% for USD 62.00/shr in cash

- Honeywell (HON): Completed acquisition of Carrier’s Global Access solution Business and raised its FY outlook.

- United Airlines (UAL): CEO says that demand is steady at the moment but industry seat growth is expected to moderate in H2, noting that some low-cost carriers will struggle to survive.

- Delta Airlines (DAL): Announced it is running its largest-ever transatlantic schedule this year as it sees healthy travel demand, especially on international routes.

- Boston Beer (SAM): Said it is aware of the WSJ article on Friday re. the sale of its company to Suntory but that it does not comment on market rumors. Adding, "We are fully focused on our business as an independent company and our return to growth."

- Toyota Motor (TM): Reported vehicle sales +15.7% Y/Y at 216,611 for May 2024

- Indie Semiconductor (INDI): To explore options including sale, according to Bloomberg

- Boeing (BA): Jet deliveries to China remain halted as regulators in China criticize the design of the new, 25-hour cockpit voice recorder used in the 737 max, and 787 Dreamliner, according to Bloomberg.

TUESDAY

- The risk tone was cautious, with equity futures trading negative in pre-markets, before paring losses as US traders arrived.

- Cash equities opened with a soft bias, and after some fleeting choppiness after the JOLTs jobs data, resumed to the downside as growth concerns continue to weigh in traders' minds.

- The JOLTs data saw a cooling of headline job openings, an unchanged quits rate, while the vacancy rate fell.

- That gave a bid to Treasuries, with the rally being led by the belly as the curve bull flattened.

- The dollar softened, and safe-haven FX came into demand, although EMFX was unable to take advantage of the USD's weakness, both due to risk-off sentiment as well as some idiosyncratic factors (see FX wrap, below).

- Equity futures went flat in later trading after Tesla (TSLA) CEO Musk detailed purchases of Nvidia (NVDA) chips, which saw the semiconductor company rally, lifting indices with it. But that foray into positive territory proved fleeting, and equities went back to flat levels shortly after.

- Meanwhile, Crude futures continued to fall on Tuesday, with traders continuing to cite the OPEC+ policy announcement from the weekend, along with demand concerns due to softening US economic momentum (JOLTs today, ISM on Monday, lower GDP trackers).

- Ahead, there are plenty of macro catalysts for traders to sink their teeth into; Wednesday sees the release of ADP jobs data, ISM Services data, as well as a BoC rate decision;

- Thursday sees an ECB rate decision, and on Friday, the nonfarm payrolls data is due.

INFLATION BREAKEVENS: 5yr BEI -3.5bps at 2.304%, 10yr BEI -2.5bps at 2.319%, 30yr BEI -1.9bps at 2.325%.

REAL RATES: 10Y -- 2.0312%

STOCK SPECIFIC

- TSMC (TSM): Chairman is reportedly considering raising production fees for Nvidia (NVDA), according to Nikkei.

- Nvidia (NVDA): CEO says his interest remains in using Intel (INTC) fabs for the Co.'s chips.

- Intel (INTC): Launched its next-gen Xeon server processors in a bid to regain data centre market share, and revealed that its Gaudi 3 AI accelerator chips would be priced much lower than its rivals' products, via Reuters.

- Social Media (META, SNAP): New York is reportedly planning to ban social media firms from using algorithms to steer content to children without parental consent under a tentative agreement reached by state lawmakers, WSJ sources said. Separately, Meta's (META) Instagram is reportedly testing ad breaks, according to The Verge.

- Alphabet (GOOG): Reportedly laying off employees from several teams in Google’s cloud unit, one of its fastest-growing businesses, CNBC sources reported.

- Tesla's (TSLA): China-made EV sales declined in May by 6.6% Y/Y to 72,573 units, amid output cuts of China-made electric vehicles. Separately, Elon Musk ordered Nvidia (NVDA) to ship thousands of AI chips reserved for Tesla (TSLA) to X and xAI, according to CNBC.

- Illumina (ILMN): Announced that its Board of Directors has approved the spin-off of GRAIL.

- HubSpot (HUBS): Reportedly rumoured to attract interest from another tech giant other than Google (GOOGL), according to Betaville.

- Viking Therapeutics (VKTX): Announced its VK2809 Phase 2b NASH study achieved its primary endpoint with patients experiencing statistically significant reductions in liver fat vs a placebo.

- Axos Financial (AX): Named a new short at Hindenburg Research.

- Bath & Body Works (BBWI): EPS and revenue beat but guidance was soft.

- Ford (F): Started mass production of its new EV Ford explorer at its first EV facility in Europe. EV sales increase +64.7% Y/Y to 8,966 units for May, while total vehicle sales units for May were reported at 190,014.

- Nvidia (NVDA): To sell approx. USD 3-4bln of chips this year to Tesla (TSLA), says TSLA CEO Musk.

- Core Scientific (CORZ): Offered to be bought out at c. USD1bln by Coreweave valuing CORZ at 5.75/shr, according to Bloomberg,

- Apple (AAPL): Reportedly held discussions with China Mobile to bring Appl TV+ to China, according to The Information.

- Cisco (CSCO): Launched a USD 1bln global AI investment fund; also announced new AI-powered innovations and investments to help customers unlock a more connected and secure future.

WEDNESDAY

- Stocks were bid on Wednesday as markets digested a soft ADP, a BoC rate cut and hot US ISM Services PMI.

- Stocks were trending higher as US players arrived and extended to record high territory throughout the rest of the session as it reacted to the mixed data.

- There was a brief knock in reaction to the Services PMI data, but ultimately it was deemed a positive for stocks on encouraging growth prospects (note the weakness seen after a soft Chicago PMI last Friday and Manufacturing PMI on Monday).

- At the same time, although the ADP data was soft, it is usually an unreliable indicator for the NFP on Friday, which participants are looking to for a more up-to-date assessment of the labor market.

- Aside from the data, there was also a dovish BoC rate decision, which saw a rate cut of 25bps as expected, while Governor Macklem signaled more cuts are coming.

- Despite the strong PMI data, T-notes were bid in reaction to the ADP data despite a brief knock on the PMI data with yields lower by c. 4-5bps across the curve.

- Attention now turns to the ECB rate decision on Thursday and the NFP on Friday previews for both are available below.

INFLATION BREAKEVENS: 5yr BEI -0.1bps at 2.299%, 10yr BEI -0.7bps at 2.309%, 30yr BEI -0.9bps at 2.315%.

REAL RATES: 10Y -- 2.002%

STOCK SPECIFIC

- Intel (INTC) and Apollo (APO): Announced an agreement where APO will lead an investment of USD 11bln to acquire from INTC a 49% equity interest in a JV entity related to Intel's Fab 34. Separately, the INTC CEO expects the co. to regain some market share, according to Bloomberg.

- NXP (NXPI) and TSMC (TSM): Plans to build a USD 7.8bln Singapore chip plant, according to Bloomberg. Plans to repurchase 3.2mln shares between 6th June and 5th August; approved capital boost for TSMC Global for up to USD 5bln.

- Disney (DIS), Comcast (CMCSA), Amazon (AMZN): NBA reportedly closing on a USD 76bln TV deal; is in advanced talks with NBC (CMCSA), Amazon (AMZN) and ESPN (DIS), according to WSJ.

- PVH Corp (PVH): Beat on EPS and revenue although guidance was soft. It also announced a leadership update where the CEO of Tommy Hilfiger and PVH Europe is set to leave the co.

- UnitedHealth (UNH): Board authorized a cash dividend of USD 2.10/shr (prev. 1.88).

- Eli Lilly (LLY): Announced the departure of its CFO, Anat Ashkenazi. Anat Ashkenazi to join as CFO of Google and Alphabet (GOOGL).

- Campbell Soup Co (CPB): Beat on revenue and earnings as well as reporting strong guidance.

- American Express (AXP): eBay (EBAY) will reportedly drop American Express Co. cards as a payment option on the online marketplace because of “unacceptably high fees,” according to an email reviewed by Bloomberg.

- Psychedelics (MNMD, CMPS, ATAI): The US FDA advisers did not approve the use of the drug MDMA to treat a form of mental illness, according to Bloomberg. The advisers voted 9-2 that Lykos Therapeutics data failed to show the drug is effective in patients with PTSD.

- SAP (SAP GY): Agreed to acquire Walkme (WKME) driving business transformation by enhancing the customer experience and enriching SAP business AI offerings; offer price represents a 45% premium to last close (USD 9.64/shr).

- Amazon (AMZN): Labor union has formally affiliated with the Brotherhood of Teamsters; members will vote to consent to the affiliation in the coming weeks.

- Boeing (BA): A further two whistleblowers go public over plane safety, reigniting safety and quality concerns. In addition, Starliner spacecraft launched successfully; BA and NASA will continue to work together to certify the Starliner for long-duration operational missions to the ISS. CEO to testify before US Senate committee on June 18th.

- Toyota (TM): Says it is to nearly double its output capacity of the Sorocaba plant in Brazil by 2026, according to the local head.

- Walmart (WMT): CEO said there is no impact from the war in Gaza, just a minor supply chain issue.

- Mercadolibre (MELI): Executive says the company is open to extra distribution centres in Brazil this year and investments in Brazil in 2024 are to surpass the initial plan of BRL 23bln.

EARNINGS

- CrowdStrike Holdings Inc (CRWD): Beat on EPS, and revenue while guidance was also above expectations.

- Hewlett Packard Enterprise Co (HPE): Beat on top and bottom line, with guidance above expectations for the FY.

- Dollar Tree Inc (DLTR): Beat on EPS, missed on revenue and announced a review of strategic alternatives for Family Dollar. Comp sales missed while it cut FY EPS guidance.

- Brown-Forman Corp (BF.B): Beat on EPS, revenue missed, and gave a positive FY25 organic net sales growth.

- Campbell Soup Co (CPB): Beat on revenue and earnings as well as reporting strong guidance.

THURSDAY

- Stocks and bonds chopped to the ECB rate decision and US data while Euro upside weighed on the Dollar but the Swissy, Yen and Aussie outperformed.

- Crude prices were bid.

- The ECB cut rates as was widely expected, although it did not give clear future guidance on future rate cuts while Lagarde noted the decision was not unanimous with reports stating that Holzmann wanted to keep rates unchanged.

- Sources later revealed that a few hawks may have preferred to keep rates unchanged today had there not been a pre-meeting commitment.

- The hawkish ECB cut did support the Euro while Bunds were hit; T-notes were also briefly dragged lower.

- Nonetheless, above-expected jobless claims and a larger downward revision to the Q1 Unit Labor Costs data from the US helped support T-notes with attention turning to the US NFP on Friday.

- Crude prices were bid after both Saudi and Russia questioned the recent downside in oil prices after OPEC+, while the US had also warned Israel about expanding the war into Lebanon on account that Iran may intervene and thus expanding the war in the Middle East.

- Note, elsewhere Nvidia (NVDA) weakness weighed on semis after reports suggested the US FTC and DoJ are to proceed with antitrust investigations into both NVDA's and Microsoft's (MSFT) AI dominance.

- Meanwhile, Meme stocks (GME, AMC) surged after RoaringKitty scheduled a live stream on YouTube for Friday.

INFLATION BREAKEVENS: 5yr BEI -1.3bps at 2.280%, 10yr BEI -1.7bps at 2.290%, 30yr BEI -1.2bps at 2.298%.

REAL RATES: 10Y -- 2.0065%

EARNINGS

- Lululemon Athletica Inc. (LULU) beat on EPS and revenue as well as reporting strong guidance, and raising its buyback program.

- Five Below (FIVE) missed on top and bottom line and gave poor guidance.

- JM Smucker (SJM) beat on adjusted EPS and gross margin but missed on revenue and EPS guidance.

STOCK SPECIFICS

- Lululemon Athletica Inc. (LULU) beat on EPS and revenue as well as reporting strong guidance, and raising its buyback program.

- Five Below (FIVE) missed on top and bottom line and gave poor guidance.

- JM Smucker (SJM) beat on adjusted EPS and gross margin but missed on revenue and EPS guidance.

- AI Dominance (MSFT, NVDA, OpenAI): US DoJ and FTC reached a deal that allows them to proceed with antitrust investigations into the dominant roles that Microsoft (MSFT), OpenAI and Nvidia (NVDA) play in the AI industry, according to NYT citing sources. DoJ will take the lead in investigating whether NVDA violated antitrust laws, while the FTC will examine the conduct of OpenAI and MSFT, the report added.

- Nvidia (NVDA) and Oracle (ORCL): The two companies have had their top-quality chips rented by some large Chinese firms for AI computing, according to The Information.

- TSMC (TSM) China competitors are reportedly developing less powerful processors to keep access to TSM production in fear of US sanctions, according to Reuters.

- ASML Holding (ASML) will ship its new chipmaking machine to TSMC (TSM) and Intel Corporation (INTC) by the end of the year, according to Bloomberg.

- Hertz (HTZ) considers selling at least USD 700mln of debt and convertibles, according to Bloomberg.

- Gamestop (GME) strength attributed to “RoaringKitty” scheduling a YouTube stream on Friday at 17:00 BST / 12:00 EDT.

- Salesforce (CRM) Director Morfit purchases USD 100mln of Salesforce (CRM) stock.

- Warner Bros. Discovery (WBD) and TNT are reportedly in talks for a possible fourth NBA rights package, according to Front Office Sports.

- NIO (NIO) missed on Q1 24 vehicle deliveries at 30,053 (exp. 31.33k, prev. 50,045 in Q4).

- Moderna (MRNA): Announced that the FDA has selected mRNA-3705 for the START pilot program.

- Old Dominion (ODFL) sees its Q2 revenue per day up 5.6% from last year, driven by an increase in less-than-truckload shipments per day. The CEO commented on their position, saying they are in a "strong position to win market share and increase shareholder value over the long term.". Nonetheless, Bank of America cut their PT on the name to USD 192/shr from USD 205/shr.

- Monster Beverage (MNST) Announced prelim results of its modified "Dutch auction" tender offer. A total of 77.4mln shares of MNST were validly tendered and not validly withdrawn at a purchase price of USD 53.00/shr. Additionally, 41.6mln shares were tendered through notice of guaranteed delivery at such purchase price or as purchase price tenders.

- Newmont Corp (NEM) CEO stated the industry is ripe for further consolidation driven by demand for metals like copper that are needed in the energy transition and challenges accessing capital.

- Meta (META) reportedly plans to use new artificial intelligence features to amplify its efforts to generate revenue in messaging services, according to WSJ.

- Robinhood (HOOD) to buy global cryptocurrency exchange Bitstamp, with the deal valued at approx. USD 200mln in cash.

- Eli Lilly (LLY) donanemab-treated participants were reviewed by the FA with reviewers saying the higher number of deaths in these patients vs a placebo cannot be completely explained by deaths due to aria or cerebral hemorrhage.

- Chipotle (CMG) shareholders approved a 50-1 stock split; record date is June 18th and stock will begin trading on a post-split basis on June 26th.

- Blackstone (BX) said it has no plans to change its BREIT repurchase program.

- Altria (MO): US FDA reportedly to rescind the ban on Juul e-cigarettes, via WSJ.

FRIDAY

- Stocks were ultimately flat aside from the Russell with the major indices seeing weakness in response to the hot NFP report, which also heavily weighed on bonds and gave a rally to the Dollar.

- Stocks had clawed back losses on the economic growth prospects in response to the solid labor market report (note both Atlanta Fed and NY Fed raised their GDP tracking estimates), offsetting some fears of a softening labor market.

- The hot report however does give the Fed more time to be patient before lowering rates, which saw T-notes tumble across the curve with the front-end and belly underperforming.

- Money markets now only fully price just one rate cut by year-end, vs 2 rate cuts priced pre-data; there is still around 50% probability of two cuts in 2024.

- The hot jobs report set the tone of trade for the day while crude prices ultimately settled flat to slightly lower with some remarks regarding the increased supply from Russian deputy PM Novak and comments on Ukraine Peace talks from President Putin kept the crude complex offered, as did the surging buck.

- Antipodes were the FX laggards although metal prices also took a beating in response to the higher yields in the US.

- Attention now turns to the US CPI and FOMC with accompanying dot plots on Wednesday.

INFLATION BREAKEVENS: 5yr BEI +1.4bps at 2.292%, 10yr BEI +1.9bps at 2.307%, 30yr BEI +1.7bps at 2.316%.REAL RATES: 10Y -- 2.122%

STOCK SPECIFIC

- Samsara Inc. (IOT) earnings missed profit expectations.

- DocuSign (DOCU) FY25 revenue guidance disappointed but it did boost its buyback program by USD 1bln.

- Microsoft (MSFT): The FTC has sent civil subpoenas to MSFT as it opens an antitrust probe of MSFT’s Inflection AI deal, with the FTC wanting to know about the purpose of their partnership and how it came to fruition, according to WSJ.

- Nvidia (NVDA) outstanding short bets stand at c. USD 34bln, nearly twice as much as what has been bet against Apple (AAPL) and Tesla (TSLA), according to S3 Partners cited by Reuters.

- GameStop (GME) announced plans to sell up to USD 75mln shares after the rally on Thursday, as well as reporting a Q1 earnings and revenue miss. RoaringKitty live stream added little new.

- Regional Banks (FRME, FNB, FULT, ONB, PGC, WAFD) - Moody's placed ratings of these six U.S regional banks on review for downgrade on Thursday due to their substantial exposure to commercial real estate (CRE) loans.

- Lockheed Martin (LMT): Germany is looking into buying eight additional F-35 jets, according to Reuters sources.

- Lyft (LYFT): CEO said Lyft has more drivers on the platform now than at any other time in the company’s history in an interview on CNBC. Stock received upgrades from Morgan Stanley and BofA.

- Google (GOOGL): Persuaded a federal judge in San Francisco on Thursday to dismiss a proposed class action over its alleged misuse of personal and copyrighted data to train AI systems including its chatbot Bard.

- Walgreens (WBA): Reportedly shelves plans for a Boots IPO as sale talks continue, according to Bloomberg.

- PowerSchool (PWSC): To be acquired by Bain Capital in a USD 5.6bln transaction, or USD 22.80/shr in cash.

- Autos (GM, F, TSLA): US is finalizing vehicle fuel economy rules through 2031 that are less stringent than what the Biden Administration originally proposed, via NHTSA. General Motors (GM) faces USD 906mln in forecasted US Fuel Economy civil penalties through 2031, down from USD 6.5bln under the 2023 proposal.

- Kroger (KR) Health's The Little Clinic is announces that patients will be able to explore medical treatment, including GLP-1s such as Wegovy, Zepbound and others as part of their weight loss journey.

| |

CONTROL PACKAGE

Remember when "developed world" central banks pretended their inflation target was 2%? Well, that lie died a miserable death today - and will do so again for good measure tomorrow - after the BOC cut rates for the first time in 4 years, and less than a year after its last rate hike, from 5.0% to 4.75% even as Canada's inflation remains a very sticky 2.7%.

And just to underscore the death of the 2% inflation target, tomorrow the ECB will also cut rates for the first time since March 2016 (and 8 months after the last rate hike), even though core Eurozone CPI remains 3%.

Of course, despite all the posturing, the Fed won't be far behind especially once it becomes clear that the myth of strong US job growth was just a mirage, and either in July or September, the Fed will join the party despite core US inflation stuck at a blistering 2.8%.

It was this long overdue realization that the G7 central banks have officially raised their inflation target by about 1% that helped pushed bond yields to fresh two month lows, and down more some 35bps in just the past week, down for a 5th straight day as financial conditions have eased dramatically (see chart of Goldman Financial Conditions Index above), undoing any jawboned tightening the Fed tried to inject into the market in recent months: indeed, the latest rate pricing shows a sharp dovish shift in the Fed cut narrative for Sept, rising to 80% vs 45% just one week ago. As Goldman's trader notes, CTAs will become a focus if yields keep moving lower. -- Tyler Durden

There are FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set":

- The 10Y TREASURY NOTE YIELD - TNX - HOURLY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - DAILY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - WEEKLY (CHART LINK)

- The 30Y TREASURY BOND YIELD - TNX - WEEKLY (CHART LINK)

- REAL RATES (CHART LINK)

FISHER'S EQUATION = 10Y Yield = 10Y INFLATION BE% +REAL % = 2.307% + 2.122% = 4.429%

| |

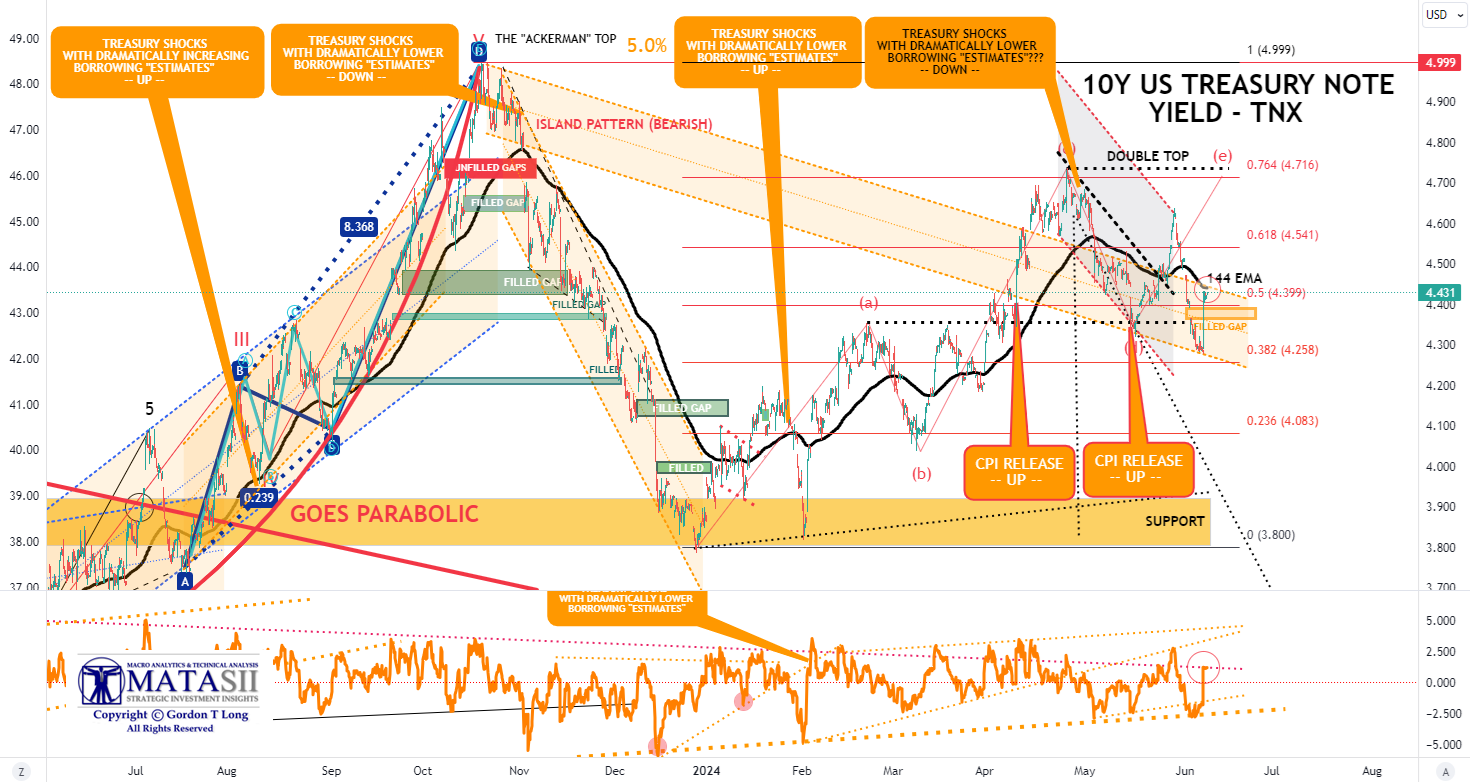

10Y UST - TNX - Hourly

- The TNX had continued to plunge since the release of the PCE until Friday's Labor Report which pushed yields up dramatically to 144 EMA overhead resistance.

- Momentum (lower pane) appears to have reached a longer term support line.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

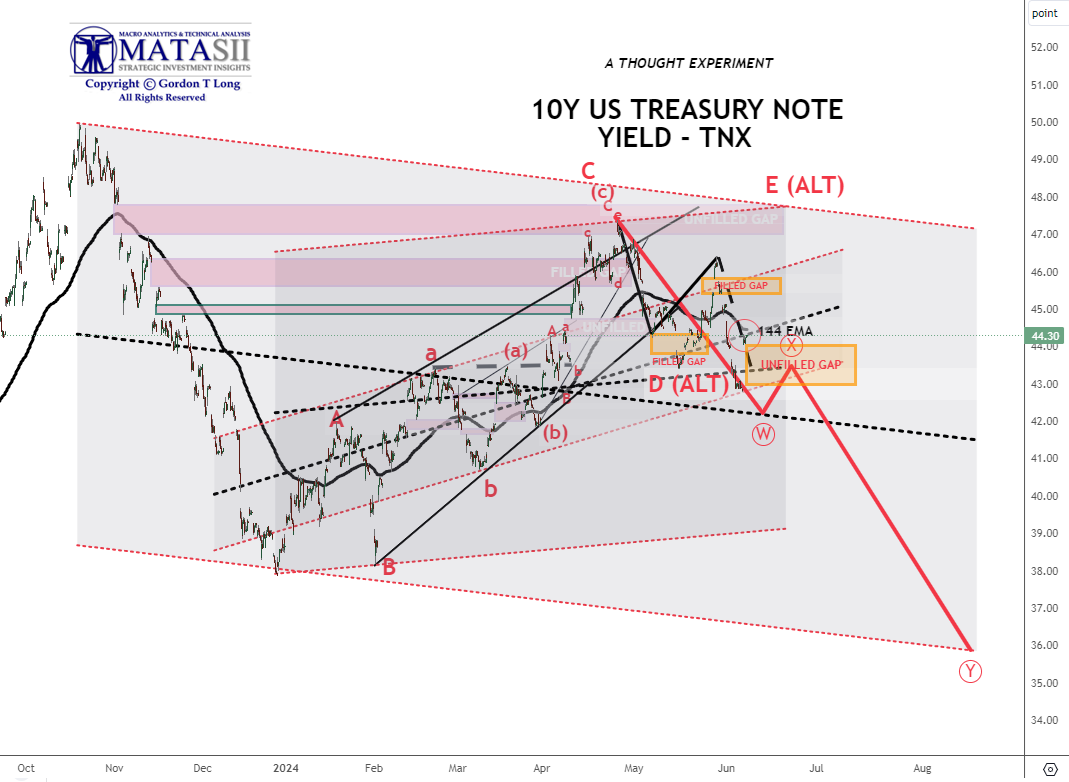

10Y UST - TNX - NASDAQ - Hourly

- The TNX (NASDAQ) continued to plunge since the release of the PCE until Friday's Labor Report.

- The "ALT E" count is back in play but a low probability.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.

========

| |

IDENTIFICATION OF HIGH PROBABILITY TARGET ZONES | |

Learn the HPTZ Methodology!

Identify areas of High Probability for market movements

Set up your charts with accurate Market Road Maps

Available at Amazon.com

| |

The Most Insightful Macro Analytics On The Web | | | | |