CURRENT MARKET PERSPECTIVE | |

|

ENERGY, GOLD, BITCOIN SENDING

A CLEAR MESSAGE

POLITICAL WEAPONIZATION OF THE DOLLAR IS AN INCREASING WORRY!

Click All Charts to Enlarge

| |

SILVER: Is Silver about to follow Gold (and other Inflation hedges) to new highs?? | |

|

1 - SITUATIONAL ANALYSIS

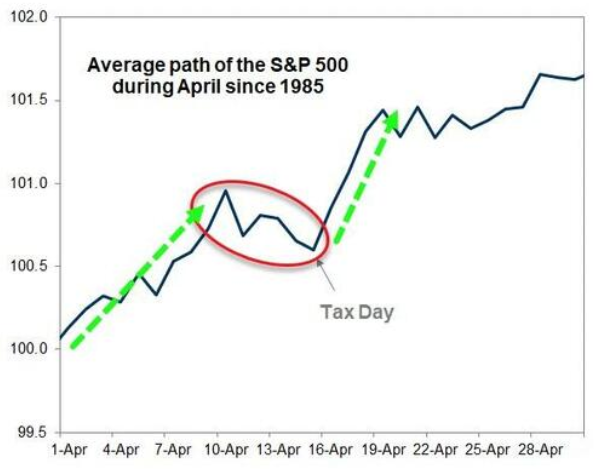

US TAX DAY April 15th: Seasonality will likely come into play here as the retail community tends to sell stocks into 4/15 to raise cash for these payments. Post payments we have historically seen a bullish trend develop.

Seasonality Says:

LONG until April 9th - Then SELL - LONG Again After April 15th

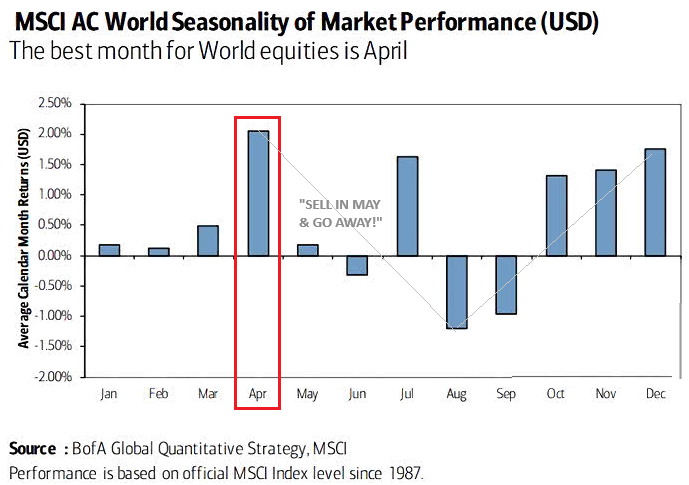

CHART TOP RIGHT: April is normally considered the most favorable month in the world for equities!

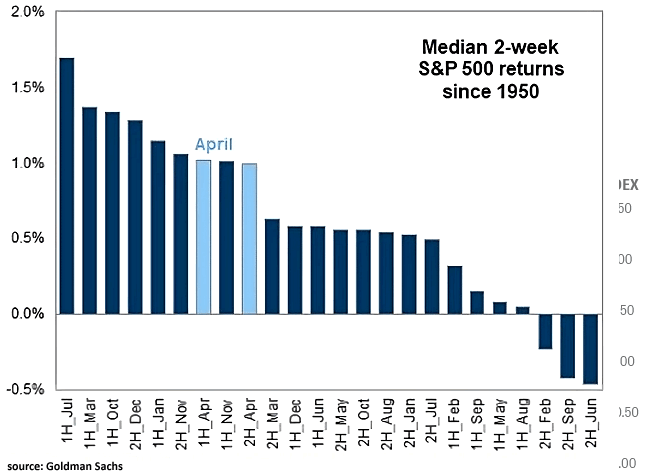

CHART BOTTOM RIGHT: The first two weeks and the last two weeks of April have historically been seasonality quite strong

CHART BELOW: Tax Day could Trigger some tradable volatility? Remember the market moving CPI is Wednesday 04/10 proceeding Tax Day on 04/15.

| |

|

|

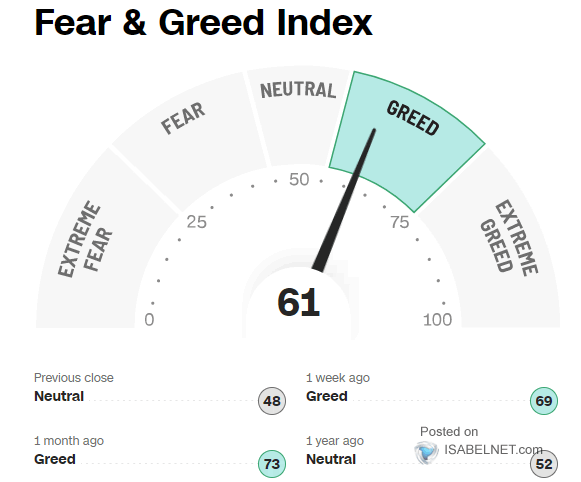

SENTIMENT MAY BE "ADJUSTING"?

We have seen some degree of market weakness over the last week as the S&P 500 tested the 21 DMA for support. It appears that increasing numbers of investors are nervous about some degree of pullback after a historic run-up without any real corrective consolidation.

The Fear & Greed Index reflects this as it has lowered quite noticeably though registering a Greed reading (chart right).

CHART BELOW

Another measure of sentiment shows we are back in neutral territory in measuring extreme Greed versus Extreme Fear. Is a Fear Shock about to kick in, at least temporarily??

| |

|

2 - FUNDAMENTAL ANALYSIS

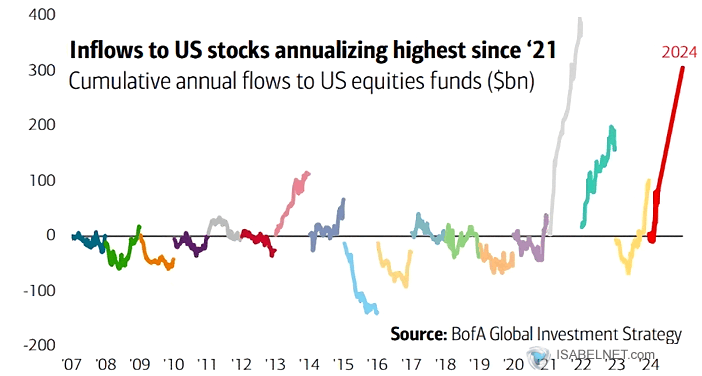

Investor appetite for equities remains strong, driven by confidence in earnings growth matching improving longer term economic growth estimates (chart right).

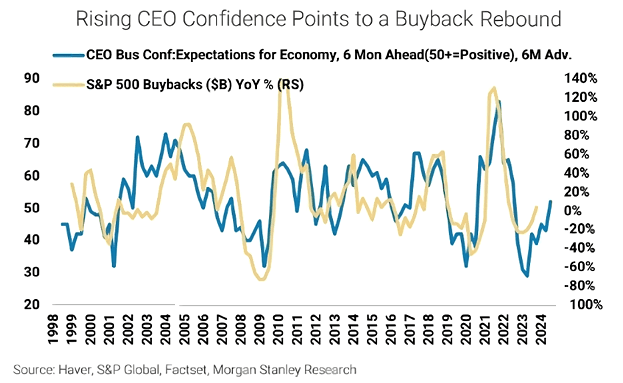

CEO'S INCREASING MORE CONFIDENT!

Any potential corrective / consolidation is to likely be short lived since CEO's are becoming increasingly more confidence with earnings outlooks looking strong. Typically this has lead to increased buyback levels (see chart below).

NOTE: Corporate Buybacks are in a closed window due to pending Q1 earnings releases.

| |

|

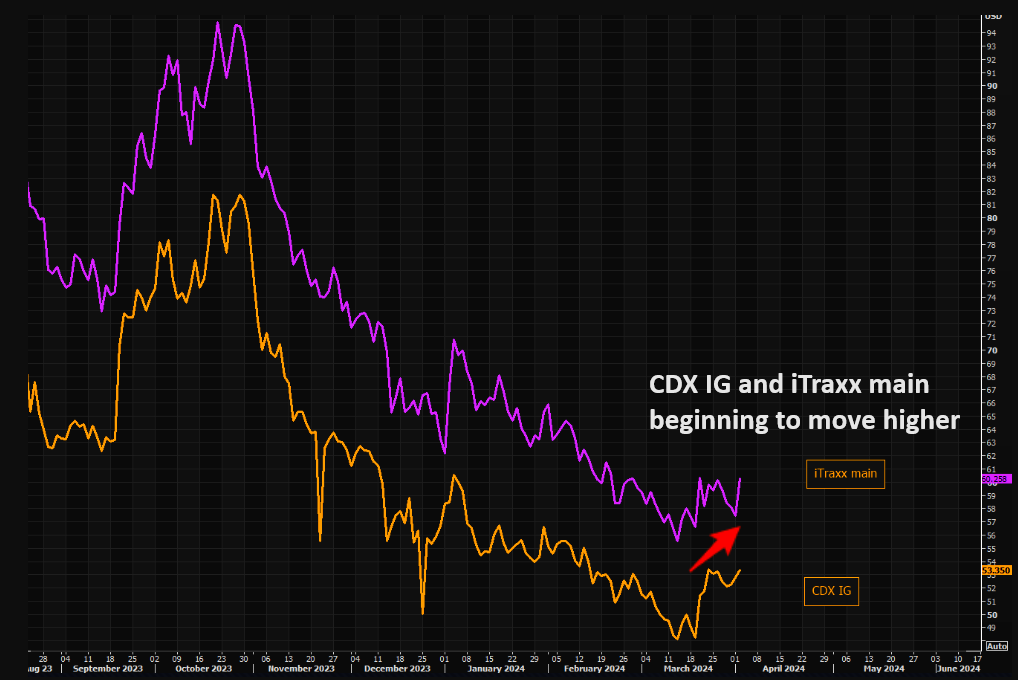

CREDIT MARKETS

Since Credit always leads markets, we are watching it closely. This includes:

- Inverted yield curves

- Negative swap spreads

- Collateral shortages

- Tightening of credit standards by banks and

- Reduced commercial lending

- The High Yield Corporate "JNK" Market. (BELOW)

CREDIT RISK PROTECTION IS GETTING MORE EXPENSIVE

As the chart to the right indicates, CDX IG and iTraax are to have bottomed and have turned up.

| |

THE HIGH YIELD CORPORATE "JNK" MARKET

There is a strong technical patterns on 2-year, 10-year, and 30-year US Treasuries showing an Ascending Triangle, all suggesting yields are heading higher (chart right).

This appears to match the HY Credit Markets which show a possible approaching conclusion to their major corrective consolidation. The technical Ascending Triangle (ABCDE) in the JNK suggests this may be completed over the next 90 days (chart below)

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

3 - TECHNICAL ANALYSIS

THE HEADLINE MARKET: MAGNIFICENT 7

- We are reaching the vertical lift part of the parabolic (geometric) lift shown by the dashed red line.

- We have intermediate term Divergence with momentum (bottom pane).

- In the short term Momentum appears to be rolling over (bottom pane).

MATASII CROSS: WEEKLY - CONTINUES TO SIGNAL A MAG-7 BUY

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

"CURRENCY" MARKET (Currency, Gold, Black Gold (Oil) & Bitcoin)

CONTROL PACKAGE

There are EIGHT charts we have outlined in prior chart packages which we will continue to watch closely as a CURRENT "control set".

-

US DOLLAR -DXY - MONTHLY (CHART LINK)

-

US DOLLAR - DXY - DAILY (CHART LINK)

-

GOLD - DAILY (CHART LINK)

-

GOLD cfd's - DAILY (CHART LINK)

-

GOLD - Integrated - Barrick Gold (CHART LINK)

-

OIL - XLE - MONTHLY (CHART LINK)

-

OIL - WTIC - MONTHLY - (CHART LINK)

-

BITCOIN - BTCUSD -WEEKLY (CHART LINK)

CHART ABOVE RIGHT

As gold pushes to higher & higher record highs (in USD terms), Real yields refuse to play along?? I side with BoAML's Michael Hartnett and believe that what we are seeing is Gold aggressively discounting a coming collapse in Real Rates.

GOLD cfd's - DAILY

The 3 Std Deviation band for Gold has gone almost vertical with Gold prices tracking it!! Frankly, in over 40 years I don't believe I have seen this technically occur with a 3 Std Dev in Gold? Something is either broken, panic has set in somewhere or there is an "elephant(s)" now playing the market?

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

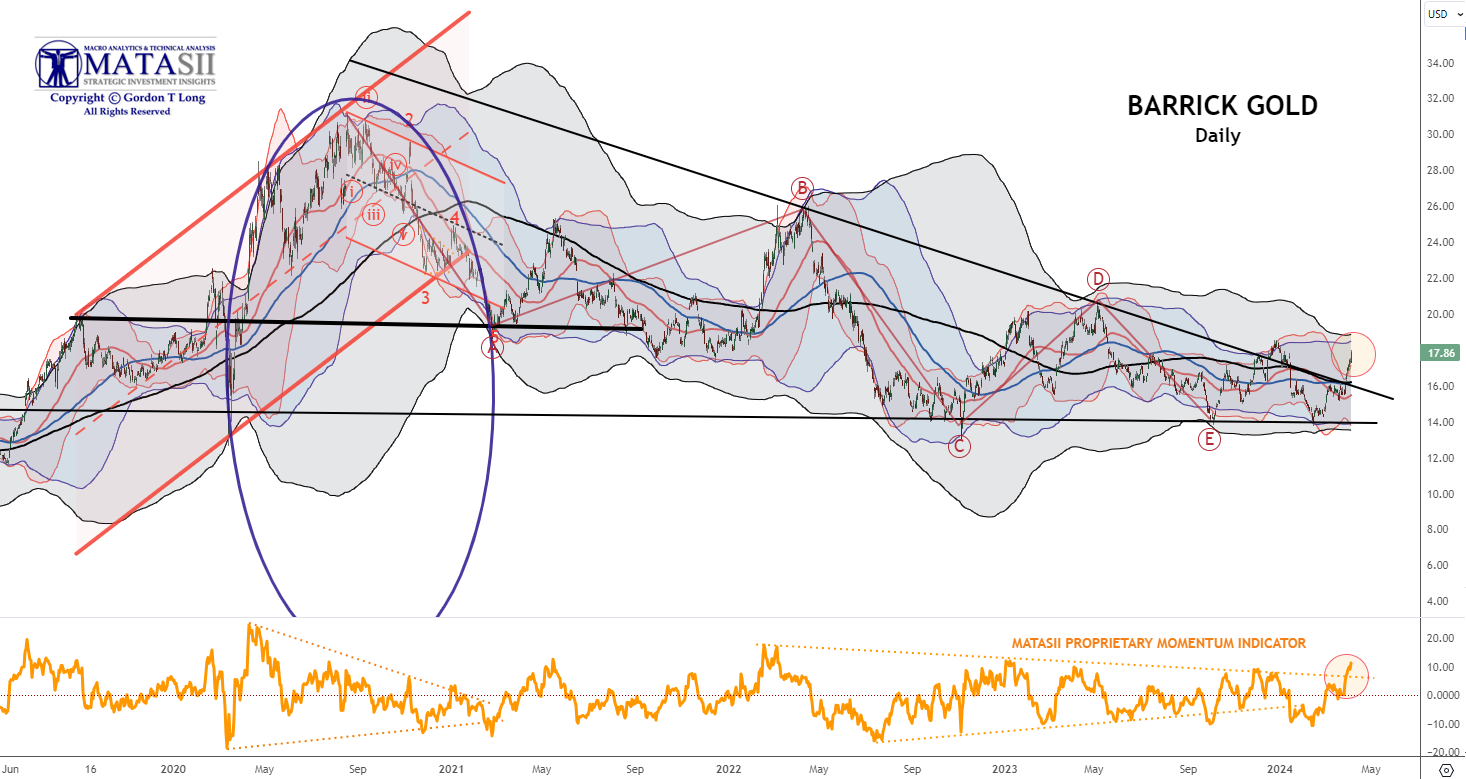

INTEGRATED GOLD MINERS

We have a close eye on Gold and the INTEGRATED GOLD MINERS as represented by Barrick Gold. Barrick which broken out of its long term declining overhead resistance trend. It is likely time to be adding to your Gold and Silver positions on pullback opportunities.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

US EQUITY MARKETS

CONTROL PACKAGE

There have FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set".

-

The S&P 500 (CHART LINK)

-

The DJIA (CHART LINK)

-

The Russell 2000 through the IWM ETF (CHART LINK),

-

The MAGNIFICENT SEVEN (CHART ABOVE WITH MATASII CROSS - LINK)

-

Nvidia (NVDA) (CHART LINK)

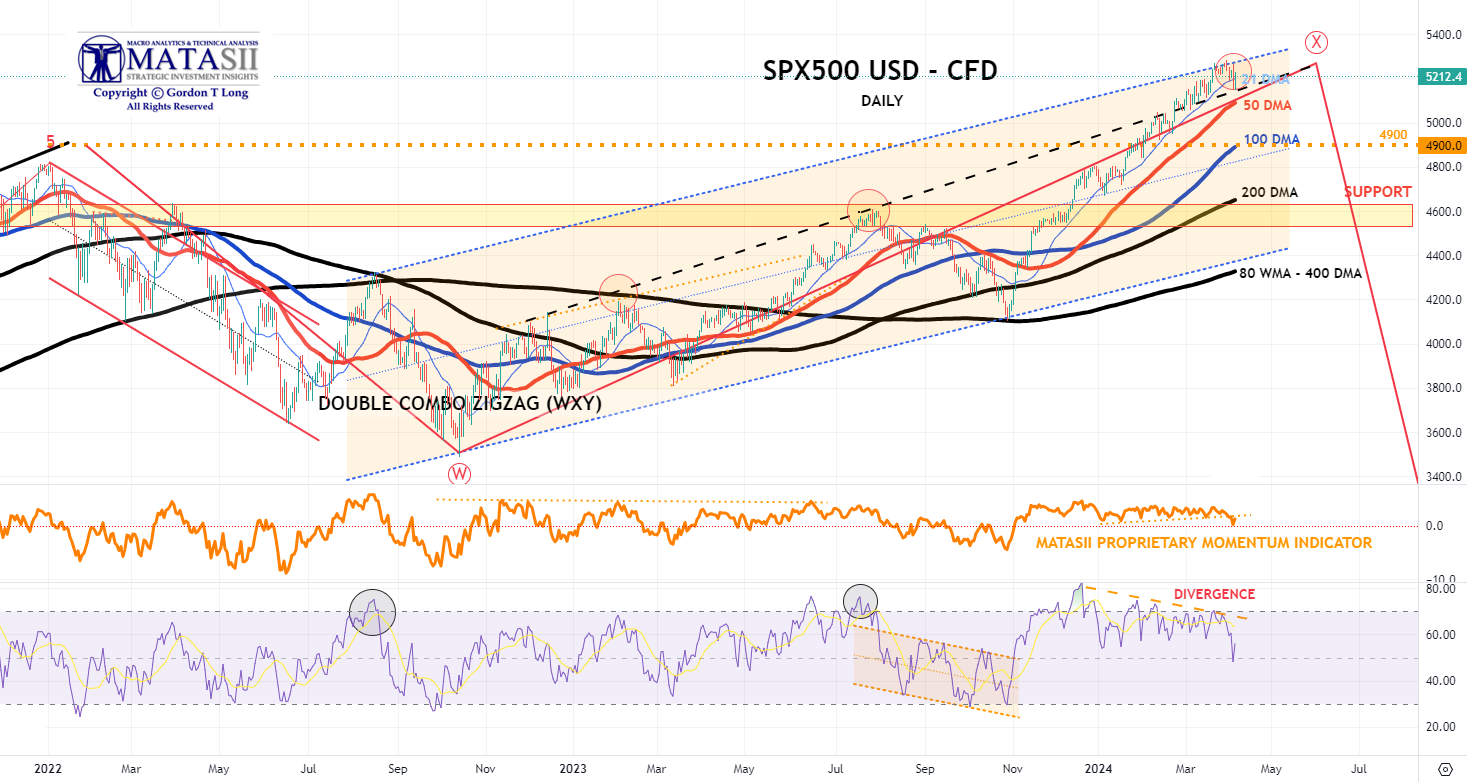

S&P 500 CFD DAILY

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

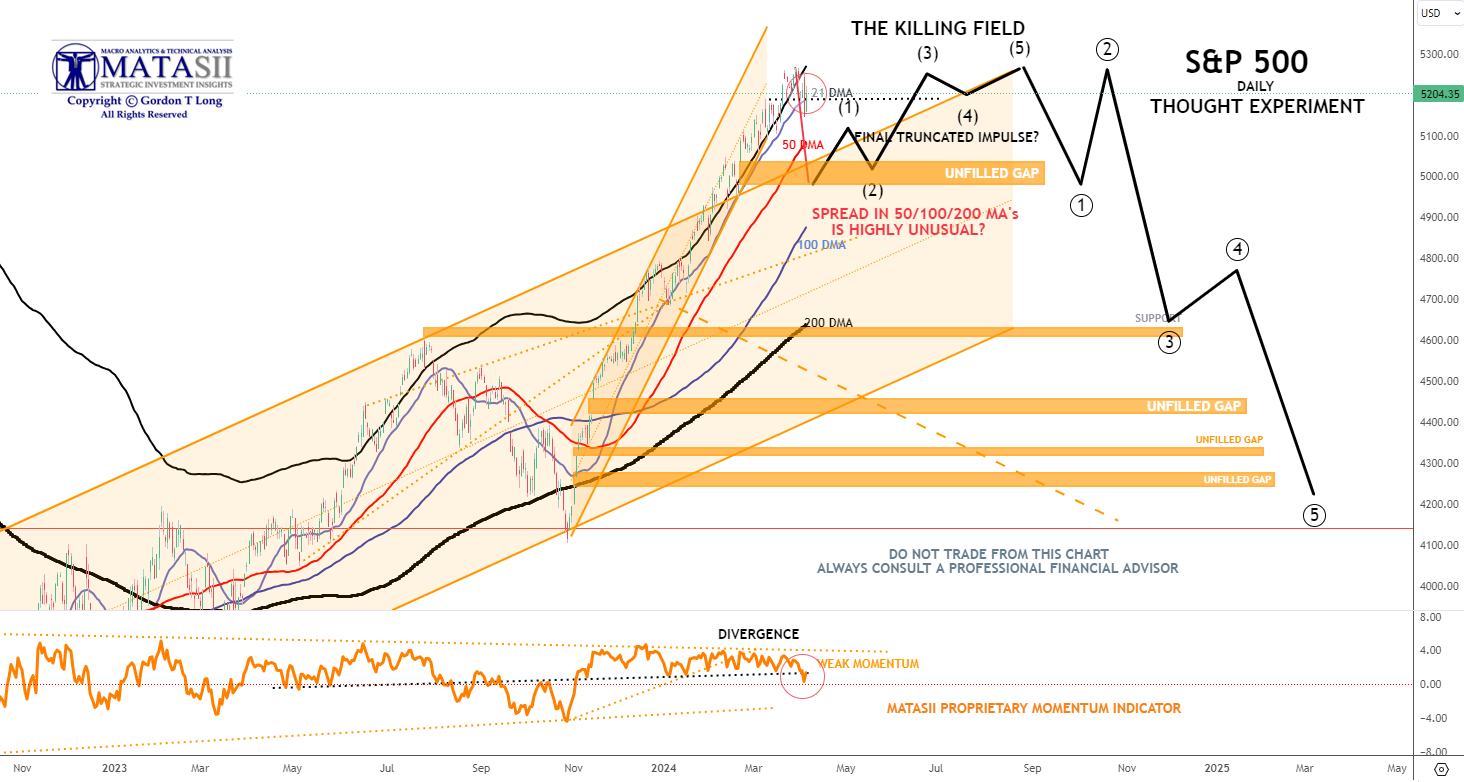

S&P 500 - Daily - Our Though Experiment

Our Though Experiment, which we have discussed previously, suggests we have put in a near term top (or very close to it) and will now consolidate before possibly completing one final small impulse higher or put in a 1-2 Wave of a much higher degree.

NOTE: To reiterate what I previously wrote - "the black labeled activity shown below, between now and July, looks like a "Killing Field" where the algos take Day Traders, "Dip Buyers", "Gamma Guys" and FOMO's all out on stretchers!"

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

STOCK MONITOR: What We Spotted

MONDAY

- Stocks were largely sold on Monday with the rate-sensitive sectors of the market underperforming after the hot ISM manufacturing survey unwound Fed cut expectations.

- The market is now priced for c. 65bps of Fed cuts this year vs 70bp+ before the data, while the first fully priced cut has been pushed back to September from July.

- Treasuries saw heavy selling (2s +9bps at 4.71%, 10s +13bps at 4.33%) amid the hot ISM data and the passing of month-end buying, with a healthy slew of corporate debt deals adding additional selling pressure.

- The Dollar saw a strong bid amid the hot US data with Euro on watch ahead of the region's return on Tuesday, with German inflation figures due.

- Oil prices continued their breakout to the upside with the hot US and China PMI data providing tailwinds. China stocks surged, with the Yuan flat against the strong Dollar.

INFLATION BREAKEVENS: 5yr BEI +1.4bps at 2.380%, 10yr BEI +2.4bps at 2.356%, 30yr BEI +2.4bps at 2.301%

REAL RATES: 10Y -- 1.9691%

STOCK SPECIFIC

- Micron (MU) +5.5%: DRAM spot prices are now reversing their steady upward trend that was seen since H2 2023, according DigiTimes citing sources. In other news, BofA increased its PT forecasting high-bandwidth memory technology demand will grow to more than USD 20bln by 2027.

- Liberty Media (FWONA) -0.2%: Announced an agreement to acquire commercial rights of MotoGP, for a EUR 4.2bln enterprise value (equity value of EUR 3.5bln). In fitting with FT reports last Wednesday.

- AT&T (T) -0.6%: Investigating a data leak that resulted in excess of 7mln customers’ information being published on the dark web.

- Tesla (TSLA) -0.3%: Raised prices for all Model Y cars in the US by USD 1k.

- UPS (UPS) -0.7%, FedEx (FDX) -3.3%: UPS has replaced FedEx to become the USPS’s primary air cargo provider.

- Disney (DIS) -0.7%: Pension Fund CalPERS (0.36% owner, 28th largest) votes to elect Trian Fund Management's candidates Nelson Peltz and Jay Rasulo to Walt Disney's board, believing fresh perspectives will benefit the Co.

- Meta Platforms (META) +1.2%: Cannot delay the FTC from reopening a probe into alleged privacy failures at Facebook while it pursues a lawsuit challenging the agency's authority.

- Microsoft (MSFT) +0.9%: Will now sell its Teams chat and video app separately from its Office product worldwide.

- 3M (MMM) +6%: Completed its spinoff of health-care company Solventum and announced a USD 10bln settlement with public water suppliers in a chemicals lawsuit had received final approval.

- US Steel (X) +2.5%: Nippon Steel (5401 JT) reportedly makes formal pledge to union in push for US Steel.

- Nuvei (NVEI) +2.5%: Enters into agreement to be taken private by Advent International for USD 34/shr.

TUESDAY

- Stocks saw notable selling on Tuesday, extending the April rot, amid various micro factors in the backdrop of an aggressive Treasury bear-steepener.

- Treasuries saw large bear-steepening on Europe's return, despite soft German inflation figures, as oil prices ripped and Europeans reacted to the long weekend's events.

- However, Fed expectations were little changed for the year-end, with Fed's Daly and Mester both noting today that three rate cuts looks like a good baseline (same as the Fed median SEP view).

- In stocks, Tesla (TSLA) added particular pressure on the Nasdaq after very poor Q1 delivery figures, while semiconductors were another pocket of weakness.

- Elsewhere, there was pressure in the apparel space after PVH's (PVH) awful guidance, citing weakening consumer trends in Europe, especially Germany and the UK.

- Health insurance names were slammed after the final Medicare Advantage rate has ignited margin concerns.

- In FX, the Dollar was lower with some profit taking in Euro shorts after the soft German regional inflation figures, while commodity currencies prospered amid the further rip in oil and metals, including gold. Bitcoin extended its selloff, and is flirting either side of USD 65k.

INFLATION BREAKEVENS:5yr BEI +3.3bps at 2.412%, 10yr BEI +2bps at 2.375%, 30yr BEI +1.9bps at 2.321%.

REAL RATES: 10Y -- 1.9792%

STOCK SPECIFIC

- Tesla (TSLA) -5%: Q1 deliveries way short of expectations (386.8k, exp. 449k), and said decline in volumes during Q1 was partially due to early phase of production ramp of updated Model 3 at the Fremont factory and shutdowns.

- Alphabet (GOOG) -0.5%: Google will destroy billions of data records to settle a lawsuit claiming it secretly tracked the internet use of people who thought they were browsing privately.

- Disney (DIS) +1%: Said to be winning a proxy battle against activist investor Peltz.

- PVH (PVH) -22%: Next quarter and FY guidance very light warning of a tougher macroeconomic setup and particular weakness in Europe.

- Verve Therapeutics (VERV) -35%: Pauses enrollment in Heart-1 trial of VERVE-101.

- SLB (SLB) -1% ChampionX (CHX) +10.5%: SLB to acquire CHX in a USD 7.7bln all-stock transaction.

- Health insurance names (HUM, UNH, ELV, CI) were lower after CMS announced rates for the 2025 calendar year will increase 3.7%, as previously proposed. Some investors had anticipated a larger hike.

- Estee Lauder (EL) +0.5%: Upgraded at Citi.

- Rivian (RIVN) -5%: Missed Q1 production estimates.

- Endeavor (EDR) +2%: Silver Lake is to take Endeavor private for USD 27.50/shr in cash; TKO (TKO) is not party to this transaction and will remain a publicly traded company.

WEDNESDAY

- Stocks and bonds were choppy while the Dollar took a hit on the soft ISM services PMI.

- Stocks started the session on the front foot in wake of the ISM data while T-Notes pared the earlier ADP-induced weakness.

- Fed Chair Powell largely stuck to the script which only pushed stocks and bonds higher and the DXY lower as the hot data seen recently appears to not have phased the Fed Chair.

- Although stocks had jumped throughout the majority of the session, gains pared in the last hour of trade as traders unwound positions.

- Crude prices were bid throughout the morning, albeit settled off best levels, after continued geopolitics, OPEC JMMC and the weekly EIA data.

- The DXY tumbled throughout the session, particularly on the soft ISM Services print which also saw prices paid ease, at odds with the strong/hot manufacturing PMI seen earlier in the week.

- The data and reiterations from Fed Chair Powell saw traders ultimately price in more rate cuts throughout the year.

- The ADP data initially saw traders pare rate cut bets but the soft ISM data and Powell commentary saw money markets lean dovish again with 72bps of easing priced throughout year-end vs. 66bps in wake of the ADP.

- Semiconductors tumbled pre-market after Taiwan's strongest earthquake in 25 years which saw TSMC (TSM) halt some of its operations.

- Nonetheless, the equity upside saw the chip weakness pare with the Semi ETF (SOXX) closing flat.

INFLATION BREAKEVENS:5yr BEI -1.2bps at 2.399%, 10yr BEI -0.9bps at 2.364%, 30yr BEI -0.5bps at 2.313%.

REAL RATES: 10Y -- 1.99%

STOCK SPECIFIC

- Intel (INTC) -8%: Foundry losses have widened, and the unit may not reach a break-even point for several years. Said its foundry business had USD 7bln in operating losses for 2023 vs. USD 5.2bln the year before.

- Paramount Global (PARA) +17%: Co. and Skydance are in advanced discussions for a potential deal, NYT reports. WSJ reported the board has agreed to enter exclusive discussions, and they favour it over a recent USD 26bln all-cash offer from a PE firm.

- Dave & Buster (PLAY) +10.5%: Board increased share repurchase authorization by USD 100mln, bringing the total to 200mln.

- Tesla (TSLA) +1%: In wake of its dismal Q1 delivery numbers, TSLA saw its PT cut at numerous brokerages accompanied by bearish commentary.

- Signet Jewelers (SIG) +10%: Raised 2025 EPS guidance.

- Spotify (SPOT) +8%: To raise prices by USD 1-2 for individual and family plans.

- Retailers (FIVE, COST, DLTR, LOW) are lower after Gordon Haskett downgraded the four names after the recent rally.

- Disney (DIS) -3%: CEO Iger wins proxy vote over Peltz with board’s election; all 12 nominees re-elected to board.

- Phillips 66 (PSX) +2%: Raised quarterly dividend 10% to USD 1.15/shr.

- Ulta (ULTA) -15%: Sees Q1 comp 'on lower end' of H1 guide of low single digits and is forecasting a slowdown in total category in Q1.

- Boeing (BA) -1.7%: 737 MAX production has fallen sharply in recent weeks as FAA steps up factory audits, according to Reuters sources; rate fell as low as a single-digit number of jets per month in late March.

THURSDAY

- Stocks saw heavy selling in late US trade Thursday as part of a broader haven influx amid uncertainty over an Iran response.

- Oil, gold, USTs, the Dollar, Franc, and Yen all saw a bid as stocks tumbled despite an obvious piece of news flow to explain the move.

- Although desks point to various signs of unease reported over the past day or so such as embassies being put on high alert and unconfirmed reports that the CIA had warned of an imminent attack on Israel.

- Note that defense contractors were an outperforming sector amid the broader stock sell off.

- Until then, broader indices had been firmer in what had been a recovery attempt of the April-to-date selling.

- In data, jobless claims rose to 221k, a bit above expectations and the highest since late Jan, albeit still low in the broader scheme of things, while Challenger layoffs rose to the highest since January 2023.

- Fed Speak lent on the hawkish side with Goolsbee and Kashkari both warning that there may be no cuts this year if inflation progress stalls, while Barkin warned of differing views amongst officials.

- Attention is now on Friday's NFP with sell-side estimates skewing higher after the ADP beat Wednesday, albeit it appears to be a consensus now that a hot print won't derail Fed easing plans, although that will be tested if AHE sees a meaningful spike.

- The latest geopolitical concerns will also muddy the picture for traders, although it is worth noting that Gold has struggled to hold on to its gains.

INFLATION BREAKEVENS:5yr BEI -0.1bps at 2.395%, 10yr BEI -0.2bps at 2.357%, 30yr BEI -0.5bps at 2.304%.

REAL RATES: 10Y -- 1.976%

STOCK SPECIFIC

- Alphabet (GOOG) -3%: Google mulls adding "premium" features to its search engine using generative AI and charging for the service, FT reports.

- HubSpot (HUBS) +5%: Alphabet (GOOG) is in talks with advisers about a potential offer for HubSpot, according to Reuters sources.

- Levi’s (LEVI) +12.5%: EPS and revenue surpassed Wall St. expectations alongside raising FY EPS outlook.

- Etsy (ETSY) +0.5%: Positive mention at the Sohn Conference; Elliott Investment Management said there is the potential for multi-year upside in Etsy's share price.

- Conagra Brands (CAG) +5.5: Profit beat and raised FY24 adj. operating margin guidance.

- Bumble (BMBL) -3.5%: Downgraded at Raymond James on near-term headwinds.

- Block (SQ) -6%: Downgraded at Morgan Stanley citing “high market penetration and limited additional opportunity”.

- Lamb Weston (LW) -19.5%: Top and bottom line missed accompanied by weak FY guidance.

- Tesla (TSLA) +1.5%: Started producing right-hand drive cars in Germany for exports to India, according to Reuters sources.

- Paramount (PARA) -8.5%: Ellison-led bid would require Paramount to raise new equity, according to CNBC citing sources.

- Boeing (BA), Spirit AeroSystems (SPR): BA and Airbus (EADSY) are reportedly exploring a framework deal to divide operations of SPR, according to Reuters citing sources.

FRIDAY

- Stocks rallied Friday after shaking off a knee-jerk sell-off to the hot US jobs report.

- The 303k jobs added (exp. +200k; prev. +270k), just in line AHE (+0.347% M/M), and fall in U rate 3.8% (exp. unch. at +3.9%) saw big selling in Treasuries as part of the broader hawkish reaction, with money markets now pricing in 65bps of cuts this year vs 70bps+ right before the data.

- A June rate cut is now just over a 50% probability vs 70% before the data, with all attention now on next Wednesday's CPI.

- Note that the front end remained pressured with Fed hawks Logan (non-voter) and Bowman (voter) the latest officials to push back on rate cut expectations.

- Oil and Gold extended their bid with geopolitical uncertainty remaining high into the weekend with reports in CBS today (citing US officials) suggesting Iran could retaliate by the end of Ramadan next week in a drone attack.

- In FX, the Dollar initially caught a bid, but faded into the close with the broader risk rally.

INFLATION BREAKEVENS:5yr BEI +1.5bps at 2.428%, 10yr BEI +1.1bps at 2.382%, 30yr BEI +0.9bps at 2.324%.

REAL RATES: 10Y -- 1.976%

STOCK SPECIFIC

- EUROPEAN CLOSES: DAX: -1.30% at 18,164, FTSE 100: -0.81% at 7,911, CAC 40: -1.11% at 8,061, Euro Stoxx 50: +0.05% at 5,013, IBEX 35: -1.58% at 10,916, FTSE MIB: -1.29% at 34,011, SMI: -1.72% at 11,490.

- Samsung Electronics: The world’s largest maker of DRAM memory chips expects to report Q1 prelim operating profit +931% Y/Y as chip prices rebound.

- BlackRock (BLK) +0.8%: Bluebell Capital Partners seeks to remove BlackRock founder Larry Fink as chairman, proposing a resolution requiring an independent director

- Shockwave Medical (SWAV) +1.9%: To be acquired by Johnson & Johnson (JNJ) for USD 335/shr in cash or USD 13.1bln. Note, SWAV closed Thursday at USD 319.99/shr.

- Becton Dickinson (BDX) +1.3%: Citi opens a 90-day positive catalyst watch. Said that the headwinds (FX and inflation), that impacted Q1 margins should begin to abate.

- Snowflake (SNOW) +1.75%: Upgraded at Rosenblatt citing healthy customer interest in the platform.

- Western Digital (WDC) +4%: Upgraded at Rosenblatt saying it should benefit from a broad rise in prices for a key type of memory chip.

- Krispy Kreme (DNUT) +7.5%: Upgraded at Piper Sandler; said Co. is on the verge of a major growth move after a deal with McDonald’s last week.

- Tesla (TSLA) -3.6%: Scraps low cost car plans amid fierce Chinese EV competition, according to Reuters sources. However, CEO Musk later replied saying “Reuters is lying, (again).”

- Sapiens (SPNS) +4.4%: Co. is reportedly exploring a sale, according to Reuters sources.

| |

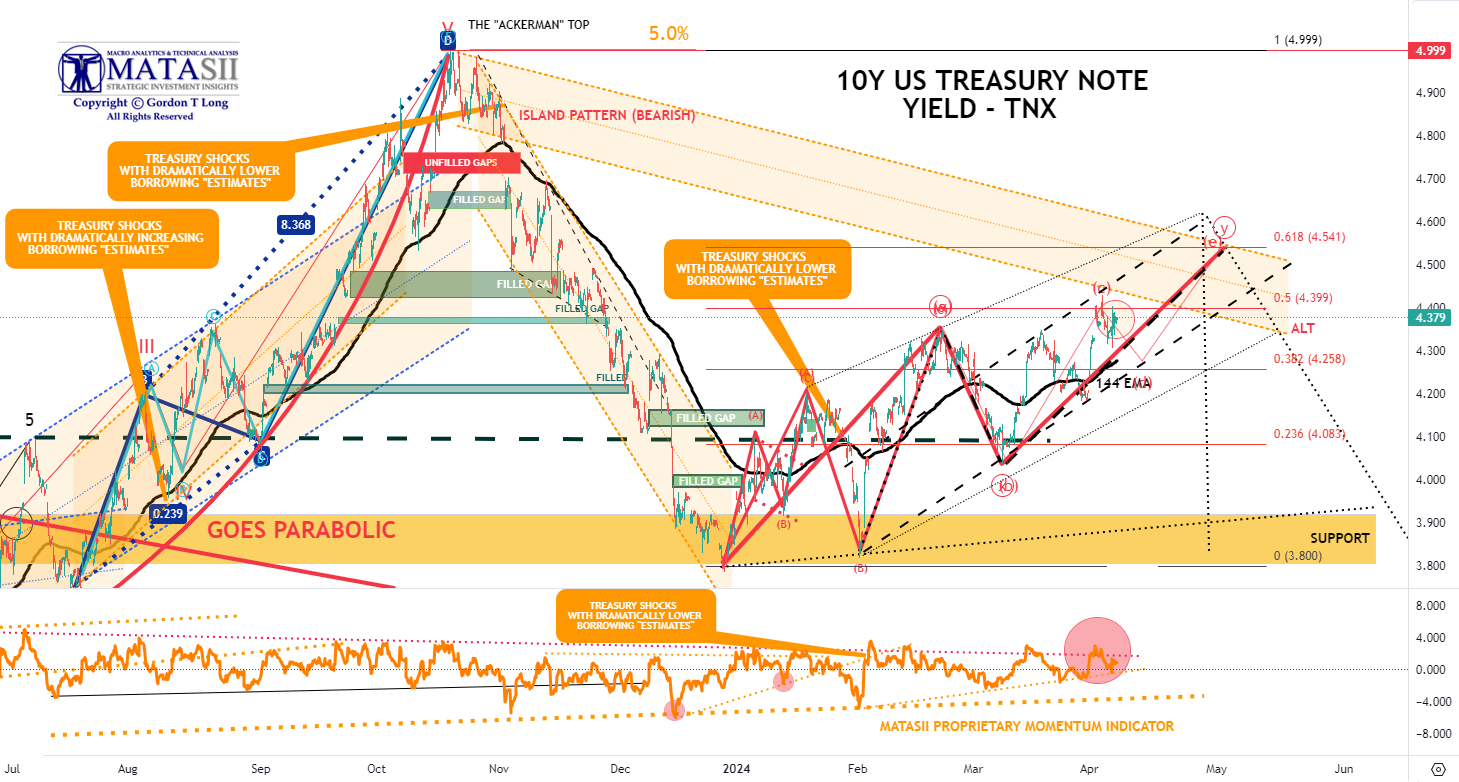

BOND MARKET

CONTROL PACKAGE

There have FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set".

- The 10Y TREASURY NOTE YIELD - TNX - HOURLY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - DAILY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - WEEKLY (CHART LINK)

- The 30Y TREASURY BOND YIELD - TNX - WEEKLY (CHART LINK)

- REAL RATES (CHART LINK)

- FISHER'S EQUATION = 10Y Yield = 10Y INFLATION BE% +REAL % = 2.382% + 1.976% = 4.358%

As rate-cut expectations fell from 6 this year to 3, Treasury yields rose... non-stop... all week with the belly of the curve underperforming (5Y yields up 28bps on the week). Yields all ended back up near their year-to-date highs.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.

========

| |

IDENTIFICATION OF HIGH PROBABILITY TARGET ZONES | |

Learn the HPTZ Methodology!

Identify areas of High Probability for market movements

Set up your charts with accurate Market Road Maps

Available at Amazon.com

| |

The Most Insightful Macro Analytics On The Web | | | | |