|

“It’s quite clear the American economy is strong.”

– Jamie Dimon, Chairman and CEO, JP Morgan Chase.

| | |

|  |

|

The New Order: Leverage Finance in an Asset Management World (Last of a Series)

🔔 Subscribe to our YouTube channel: click here

| |

Best Practices in Private Credit (Third of a Series) | |

|

Why is portfolio construction such an important concept for analyzing private credit managers? The answer seems obvious, but it’s more than ensuring defaults and loses are minimized.

As the asset class has grown to dominate the debt capital markets, questions persist around its durability. How will the asset class perform in a real downturn? Will BSL competition compress spreads and raise credit risk in a “race to the bottom”? Are private credit valuations supportable, or will they crash and contaminate the financial system leading to another GFC?

We believe these conclusions are unfounded. The best private credit portfolios act as firewalls when market volatility impacts liquid assets. 2022 was a prime example of that dynamic. By selecting borrowers whose businesses weather rate or economic storms reasonably well, direct lenders can maintain consistent and stable returns for their investors.

What underwriting practices define the best private managers? While industry and macro trends are important, for smaller companies, how diverse are revenue streams and customer base? Do they have diverse groups of suppliers (a critical Covid-era need)? Same for product portfolios and SKUs. How sustainable are cash flows? Can maintenance capex be throttled back to lower levels to generate enough cash to service debt in a downside scenario?

Market leadership is critical. Can the company’s brand and corporate attributes be easily replicated? What are the competitive barriers to entry? If the borrower disappeared tomorrow, would it matter to its clients? Has it been through a variety of business cycles? What was its track record through Covid? Being a market leader is a direct contributor to pricing power. How much leverage does the company have over its customers to cover cost increases or increase margins? This is often a critical sign in assessing the borrower’s “value add”.

Under-appreciated is the role of management. Nothing can support a successful business plan like a top-notch C-suite. Or sink it with the wrong one. Do they have experience with other leveraged borrowers in similar industries? Can they execute on complex growth strategies including integrating numerous acquisitions without losing track of cost controls? How integrated are the company’s IT systems?

Less tangible, but a huge issue today, is employee retention. The cost of acquiring and retraining (and the failure to retain) talent has become a leading concern for private equity sponsors. This results in problems of underutilization and cost absorption, particularly if key revenue producers exit. Note how relevant this has become with so many direct lenders focusing on people businesses in service sectors.

Just as LP’s looking to invest in private credit managers must evaluate retention and incentives for senior management and portfolio managers, lenders themselves need to focus on the corporate cultures of their borrowers. It’s not just having the right team going into an investment that matters. It’s making sure you keep them for the long haul.

| | |

|

|

New: Private Capital Call Podcast

Episode 5: Ron Kahn, Lincoln International,

"You don't have the liquidity issues in the private markets that you do in the public markets, which has a lot of effect on valuations." - Ron Kahn

| |

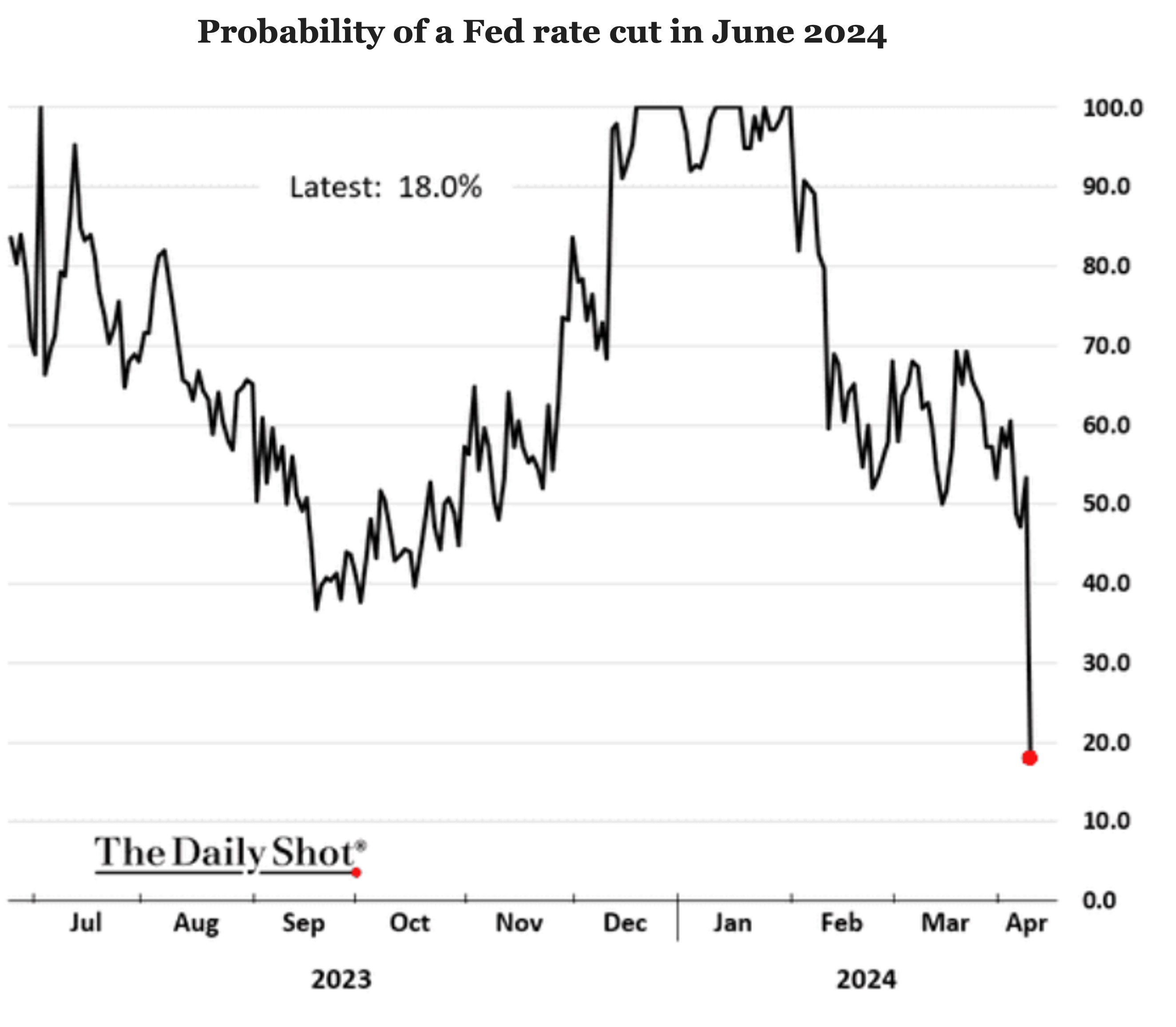

Market observers now think a rate cut at the Fed’s June meeting is unlikely. | |

|

Source: The Daily Shot

(Past performance is no guarantee of future results.)

| |

|

|

30-DAY FREE MEMBERSHIP

Join the leading voice of the middle market. Try us free for 30 days.

| | | |

The investor view from Asia | |

The need for income and the attractive risk/return profile of senior strategies are among the reasons why private debt is popular among LPs based in APAC. | |

|

Private Debt Investor’s recent APAC Forum in Singapore featured many views and insights from leading investors in the region. As our chart shows, appetite for private debt among global LPs remains strong – and in Asia-Pacific it’s no different.

David Chua, chief investment officer at Singapore-based insurance company Income Insurance, spoke on a panel about how and why investors have embraced private debt.

“Since you have the well-known challenges on the banking side, insurers have become more prominent,” he said. “With public markets highly volatile, we want to avoid that noise and friction in our portfolio so we look at what role private debt can play. We find that it’s attractive for its income and price stability and it acts as a diversifier within fixed income. We also think debt will play a more important role relative to equity in this environment.”

“Private debt has been a large and growing part of portfolios,” added Kerrine Koh, a managing director in the client solutions group and head of the Singapore office at Hamilton Lane. She sees allocations going

| |

|

up as part of a search for income, with some of the capital coming from new strategic allocations to private debt while some comes from private markets or fixed income/public credit buckets.

Koh also observed a trend of favouring senior debt where “the returns versus the risk are very attractive”. This approach is seconded by Chua, who said: “When you can obtain low double digits in senior lending, why would you stretch for an additional 200 basis points?”

Lulu Wang, a portfolio strategist in private markets solutions at Abrdn, said her team has backed some pan-Asia special situations strategies in the past but is also now allocating more to senior debt. This conservatism is partly based on caution around the changed backdrop against which managers are operating:

“Many managers haven’t been tested and, in a zero-rate environment, it’s unsurprising that you have low losses and defaults,” she said. “We’re now transitioning to a new environment. Can managers continue to source deals effectively when private equity activity is lower?”

| |

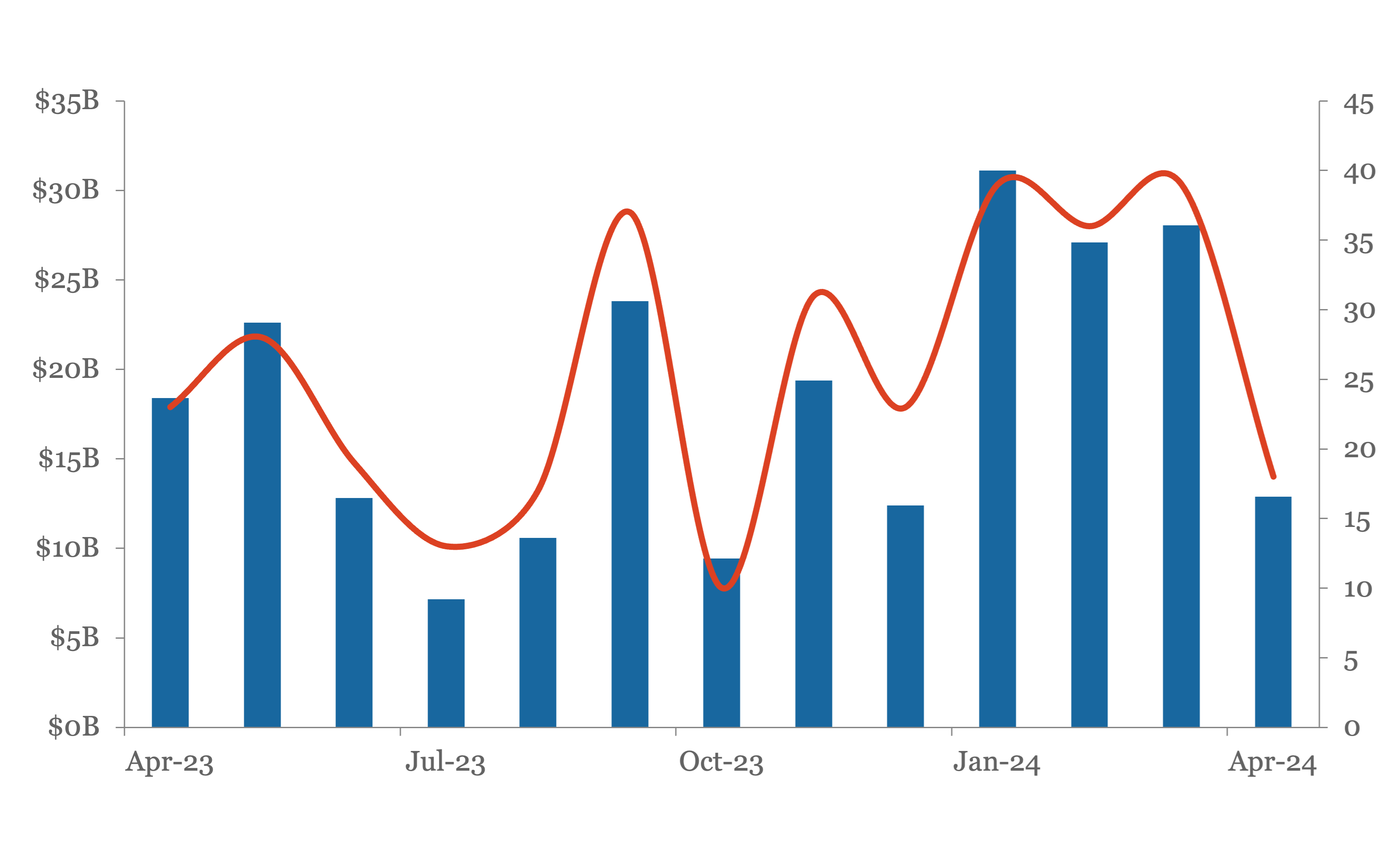

Leveraged Loan Insight & Analysis | |

|

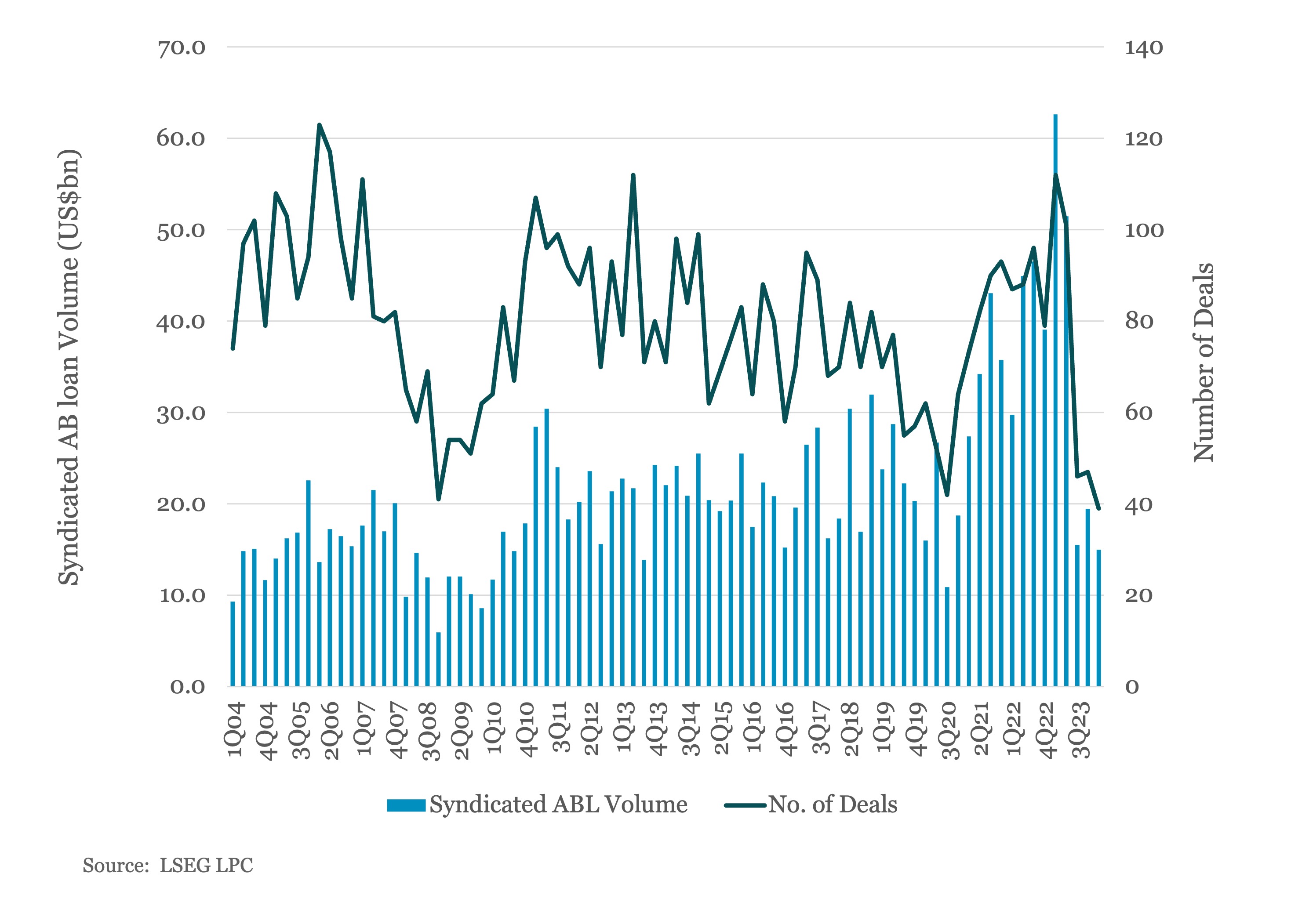

1Q24 ABL loan volume down 76% year over year

at US$15bn

| |

US lenders completed US$15bn of asset based loan volume in 1Q24, marking the lowest quarterly total since 3Q20 during the height of the Covid pandemic and a 76% drop in issuance year over year. Part of the steep decline in lending can be traced back to the fact that a substantial amount of ABL refinancing activity was | |

pulled forward in 1H23 as the market moved away from Libor based pricing. Ultimately 39 syndicated deals worked their way through the market during the quarter, down from 112 at the same time last year, to mark the lowest quarterly results on record. | |

The Pulse of Private Equity | |

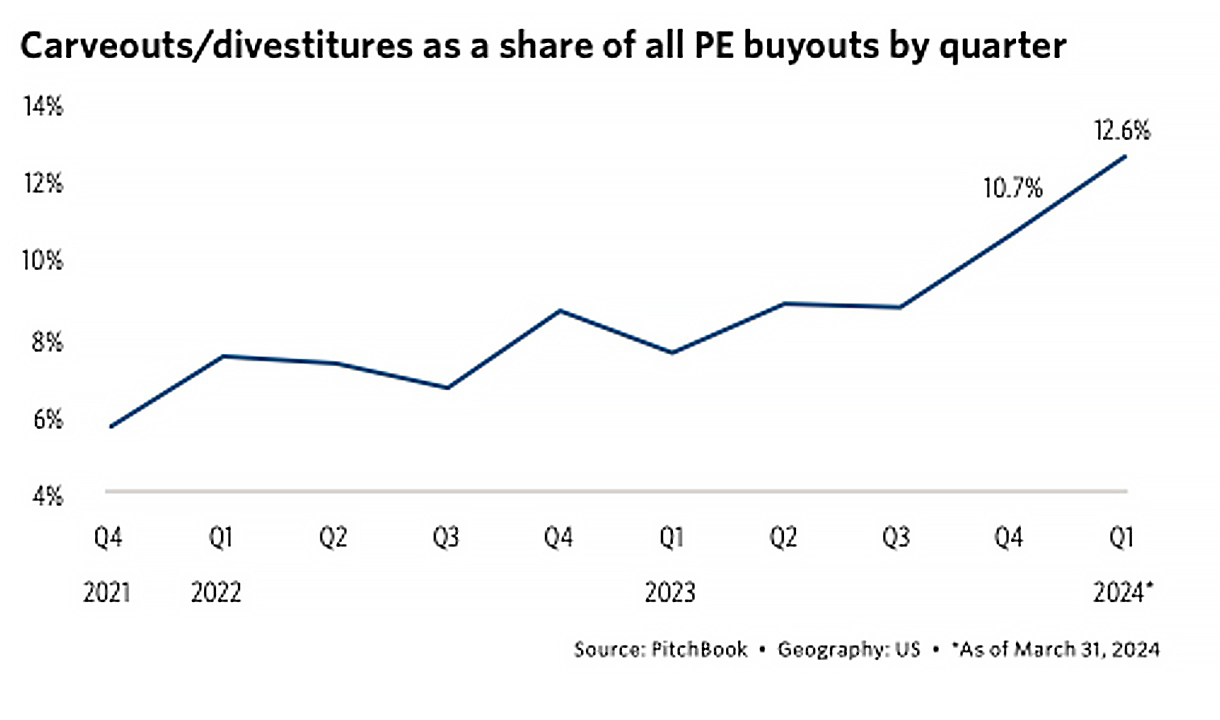

Carveout activity rebounds: Why corporate owners are selling | |

At the same time interest rates inflected upward for PE borrowers, earnings growth inflected downward for business owners and corporations. Earnings per share growth on S&P 500 companies has stagnated over the past two years, including three straight quarters of decline between Q4 2022 and Q2 2023 and three quarters of low-single-digit growth since then. For large companies tasked with achieving faster growth than the overall economy or peers, divestitures have always been a constant companion to the corporate strategist. When needing to kick growth into a higher gear, boardrooms can decide to either acquire what they do not own or divest what they do own. With growth rates as anemic as they have been over the past two years, this has caused more large companies to contemplate the latter, especially given the high cost of capital to fund a new purchase and the perceived likelihood of a recession. Large corporate owners were thus motivated to conserve cash and review what they own; at the same time, PE firms were more amenable to buying divested assets. With a more motivated universe of potential sellers, the bid-ask spread has been less disrupted than other areas of the M&A deal market. | |

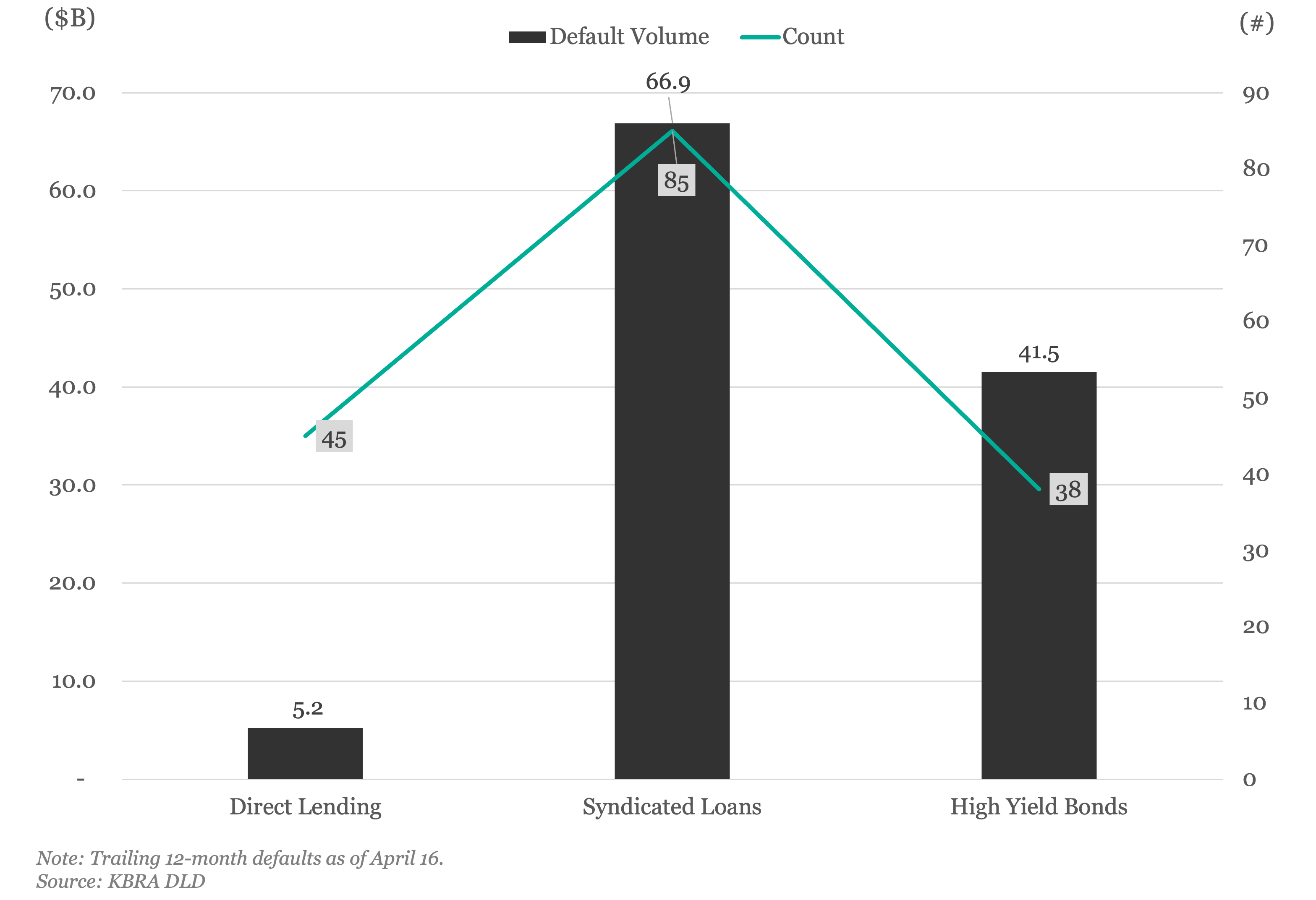

KBRA Direct Lending Deals: News & Analysis | |

TTM Default Volume, Count | |

Middle Market & Private Credit | |

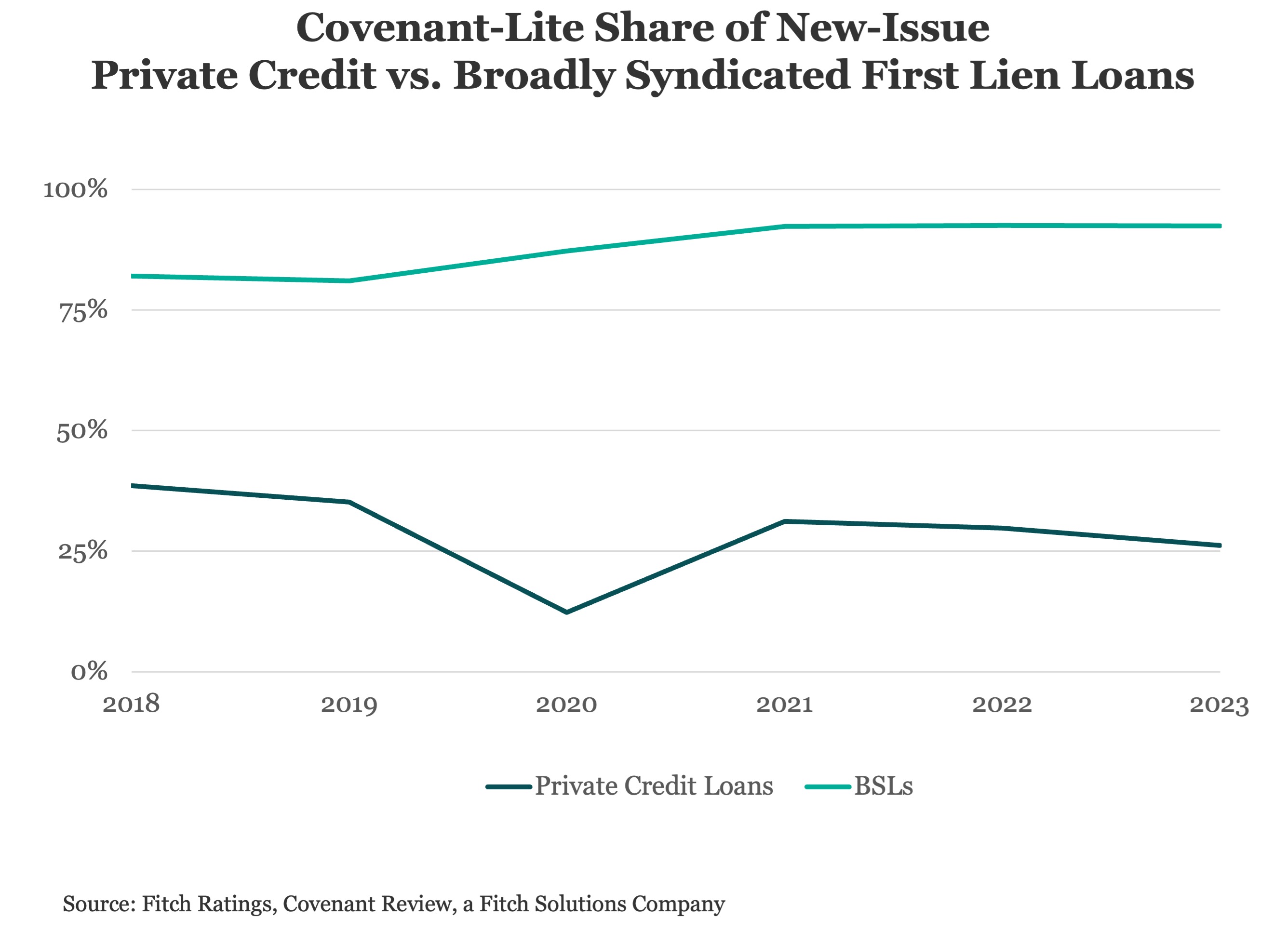

How Do Covenants for Private Credit Loans Compare to Broadly Syndicated Loans? | |

|

While liability management exercises (LMEs) are not necessarily prohibited in direct lending documents, they are considerably less common than in the BSL market. We have yet to observe LMEs in the private credit portfolio rated for asset managers.

| |

|

Fitch believes that the lack of LMEs within private credit indicates sponsors’ preference to avoid the reputational risk inherent in mistreating their lender-partners more than any concerted effort on the lenders’ side to avoid covenant weaknesses, such as those exposed in BSL LMEs including J. Crew and Serta.

Download Report

| |

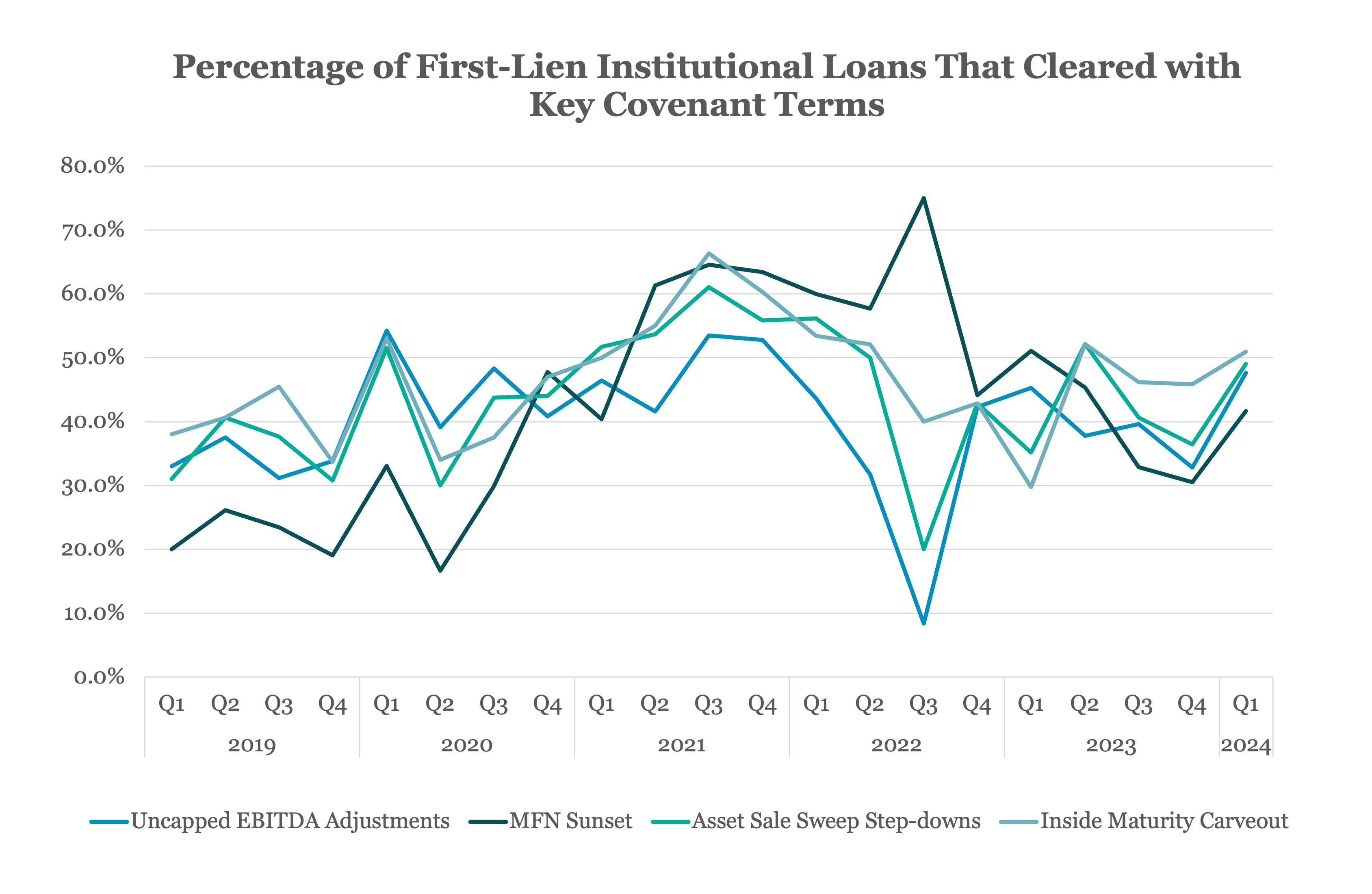

Percentage of First-Lien Loans Clearing with Key Covenant Terms by Quarter | |

High-Yield Bond Statistics | |

Weekly fund flows source: Lipper | |

|

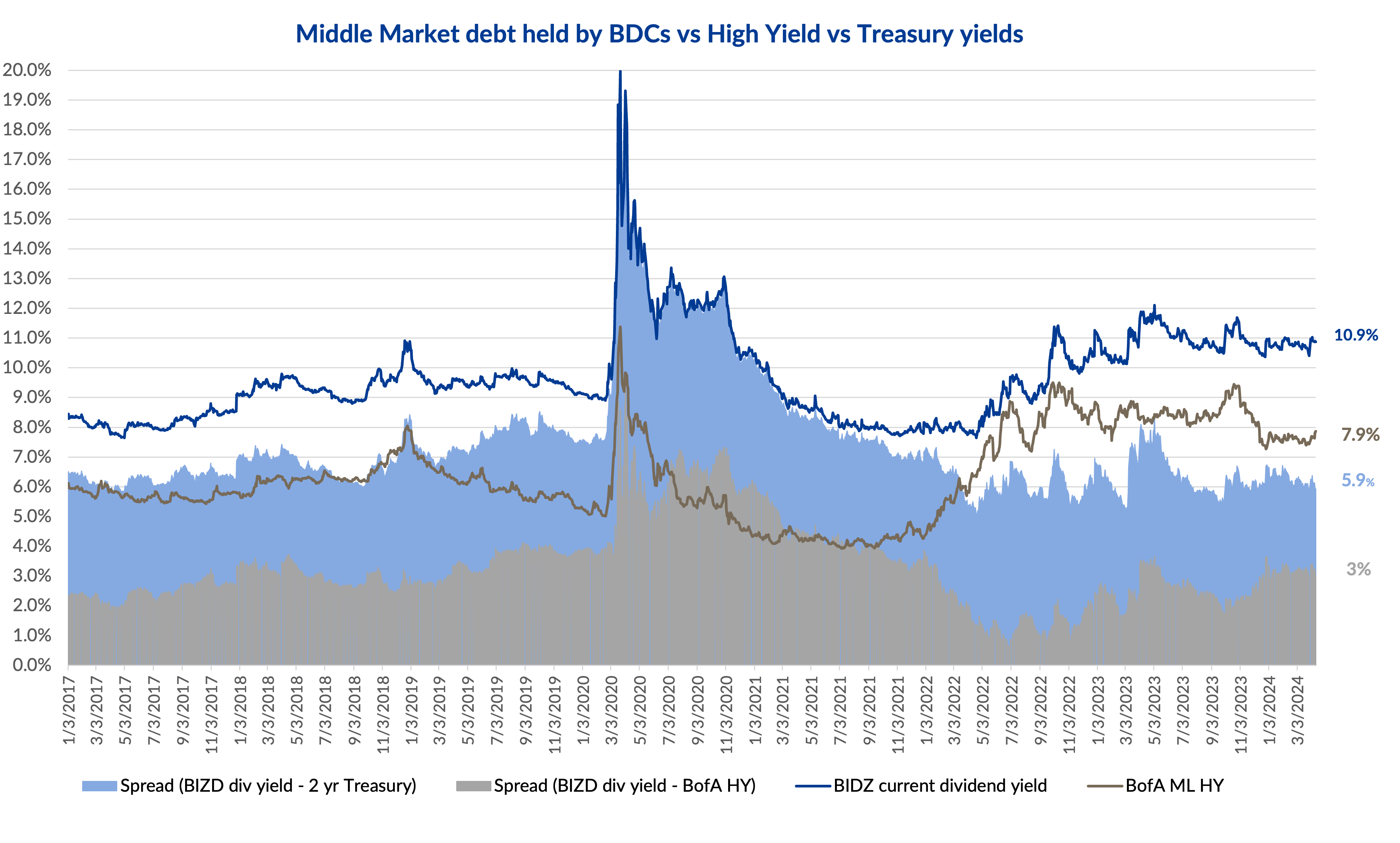

The blue line in the chart is the current dividend yield of the *VanEck BDC Income ETF (currently at 10.9% as of 11 April, down from the highest level in last 12 months of 12.1% in May 2023) that tracks the overall performance of publicly traded business development companies (BDCs, lenders to privately held middle-market businesses that tend to be below investment grade or not rated, with most lending comprising of senior secured loans). The brown line displays the BofA Merrill Lynch US High Yield (US HY index - currently at 7.9% as of 11 April, decline from the highest level in last 12 months of 9.5% in October 2023), which tracks the performance of USD denominated below investment grade corporate debt publicly issued in the US.

In March, CPI increased for the third consecutive month to 3.5%, from 3.2% in February and 3.1% in January. Despite sticky inflation, FED had indicated three rate cuts in 2024 on 20 March, while keeping interest rates unchanged (5.25%-5.5% since July 2023) for now. Given the rise in inflation which is still above the FED’s targeted inflation of 2%, rate cuts on 30 April – 1 May meeting seems to be unlikely. The spread of BIZD dividend yield minus the US High Yield (shaded area in gray) shows the premium/discount of middle-market loans over traditional high yield. As of 11 April, BIZD dividend yield was at a premium of 300bps to the US High Yield Index, 24bps above the 1-year average of 276bps. The premium for middle market, to some extent, depicts illiquidity for private loans and the credit risk associated with middle market companies. The spread of BIZD dividend yield minus the 2-year treasury (shaded area in light blue) stood at 594bps as of 11 April, below the 1-year average of 633bps.

*As of 31 March 2024, BIZD’s weighted average market cap stands at USD 5bn, with PE ratio of 8.22 and PB of 1.01, with the entire portfolio holdings in publicly traded BDCs. Click here for top holdings.

| |

Private Debt Intelligence | |

Family offices warm to Infrastructure, private debt, and hedge funds | |

|

Private equity is the main alternative asset class for family offices, with 58% of those tracked by Preqin active in the strategy, ahead of real estate (46%). However, while just 21% of family offices are active in hedge funds and private debt and 20% in infrastructure and natural resources, analysis of near-term commitment plans show shifting preferences.

Infrastructure, private debt, and hedge funds are set to play a greater role, with investors attracted to the lower volatility and hedging benefits. Half of all family offices active in infrastructure plan a commitment in the next 12 months, compared to 29% in hedge funds, and 19% in private debt. By contrast, just 9% of active family office investors in private equity intend to make an investment in the next 12 months.

For more, read Preqin’s Report: Family Offices in 2024: Lessons on Investing in Alternatives: A Preqin Primer

| |

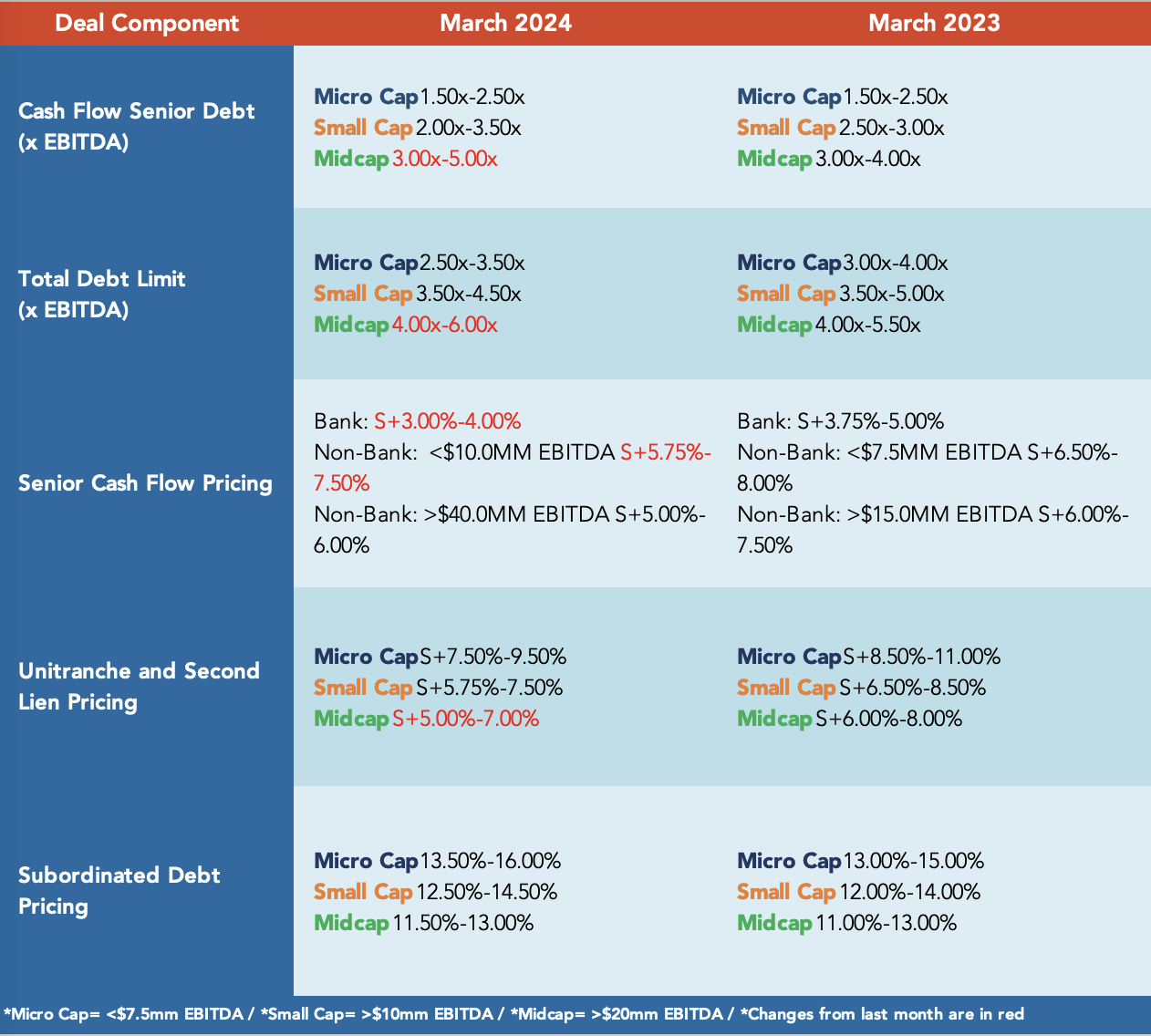

Middle Market Deal Terms at a Glance | |

This publication is a service to our clients and friends. It is designed only to give general information on the market developments actually covered. It is not intended to be a comprehensive summary of recent developments or to suggest parameters for any prospective financing opportunity. | | | | |