|

Last Thursday was opening day for MLB, a hopeful sign of spring. Catching up on some interesting 2023 statistics from our national pastime, we noted that Luis Arráez of the Miami Marlins won the NL batting championship with a .354 average. Astonishingly, this was Arráez’s second consecutive title. He topped the AL in 2022 with the Twins, becoming the first player ever to perform that feat back-to-back in different leagues.

Nicknamed La Regadera (“The Sprinkler”) for his exceptional hitting ability, Arráez struck out fewer than 8% of his plate appearances, compared to 25% for the average ballplayer. His batting average is also 100 points higher than the average. We raise this because it highlights the stark contrast between average and best-in-class performers.

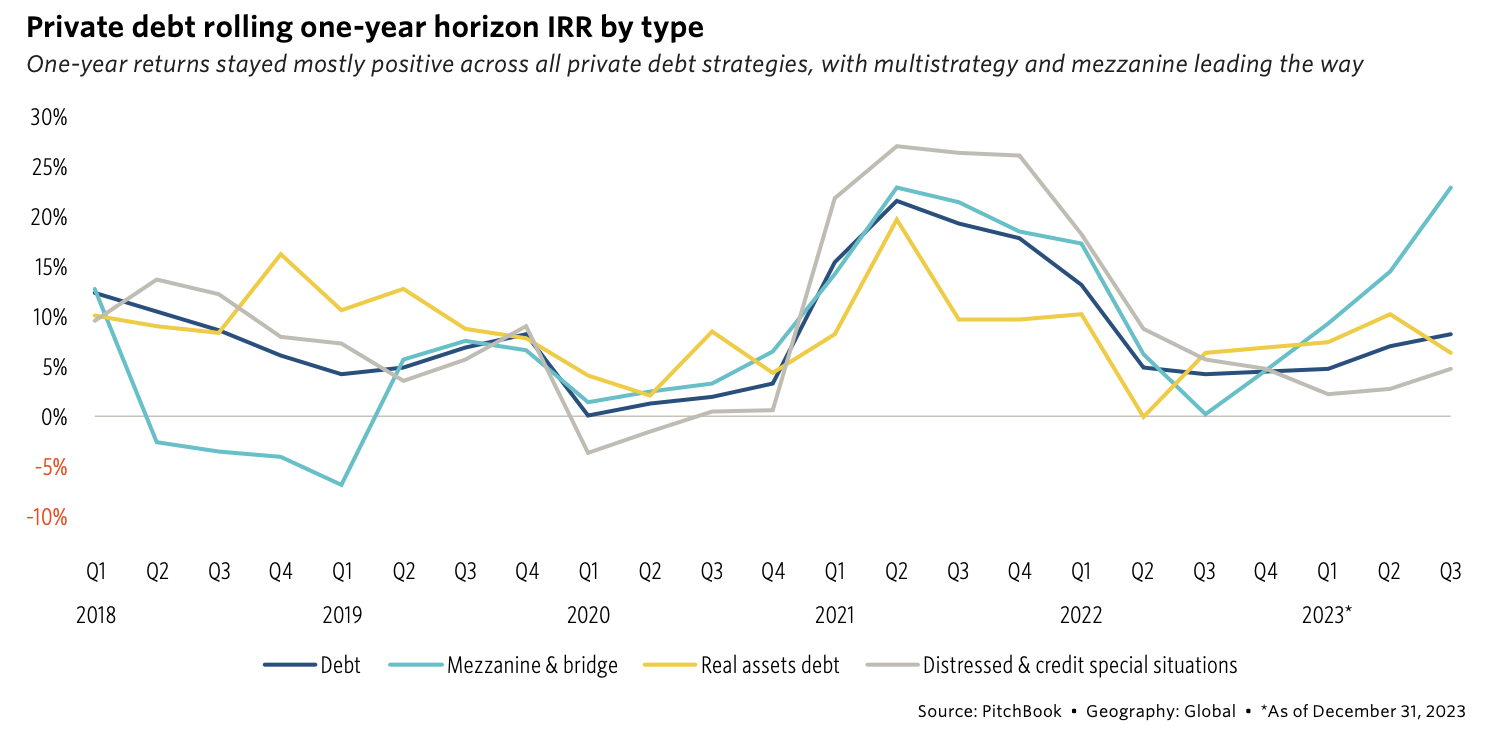

Investors in private credit also focus on managers with low strike-out percentages who can hit to all fields. We’ve highlighted how media and some research outlets address topics such as defaults and recoveries. They cite data compiled from dozens of managers. But this is misleading. Investors don’t invest in all managers. They select the best based on a variety of factors.

What distinguishes a Luis Arráez from, say, a Kyle Schwarber (.197, 29%)? In this special series, we’ll examine what the best private credit managers do in their routine investment processes that make them investor favorites. Discipline and repetition are critical for ballplayers and those providing investors all-weather returns through different economic environments.

Success is a balance of offense and defense. Deploying capital efficiently means sourcing top performing assets – financings to superior corporate borrowers backed by (in sponsor-backed businesses) top-tier private equity firms. Once in the portfolio those companies and their financing structures need to withstand any micro or macro threats.

Let’s break down the steps comprising those processes. First, the origination team matches opportunities with agreed-upon risk parameters to minimize defaults and losses. That means not wasting time on situations that won’t pass the variety of screens established by a team with years of credit experience.

Then underwriters sort through reams of industry and borrower-specific information in due diligence where potential land mines could impact operating results. But when the deal closes, the team’s work is just beginning.

Critical to smart investing is close monitoring and communication on borrower performance, alert to early warning signs of revenue or cash flow shortfalls. Winning teams have great relief pitchers (“stoppers”) who can snuff out problems before the game gets out of control.

Join us over the next several weeks as we walk through these investing steps in more detail.

|